Will the budget’s tax changes help or hinder housing supply?

The federal budget’s changes to negative gearing and capital gains tax (CGT) were designed to reduce investor demand for established housing, thereby lowering prices, without negatively impacting housing supply.

From 1 July 2027, investors will only be permitted to fully negatively gear newly built dwellings.

From 1 July 2027, the 50% CGT discount is abolished and replaced with cost‑base indexation (taxing only real gains) and a 30% minimum tax rate on capital gains.

However, new builds will retain access to both the old and new CGT systems, giving investors a choice of the more favourable treatment.

These changes create a preferential CGT environment for new housing, making new construction more attractive than buying established dwellings.

The aim is to shift investor demand so that investment adds to housing supply rather than bidding up the price of existing stock.

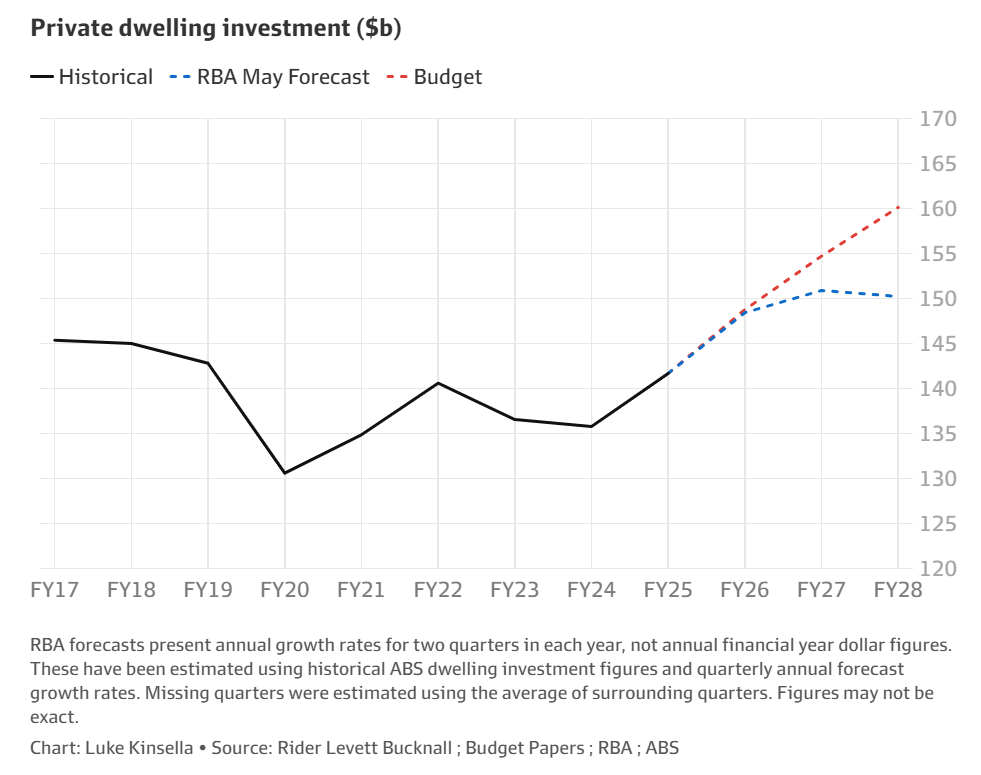

The Australian Treasury believes that the changes will boost supply. The federal budget explicitly forecast $315 billion in new housing investment over 2026‑27 and 2027‑28.

However, the RBA expects dwelling investment to fall from late 2027 because of construction constraints. As a result, its new housing investment forecast is $13.7 billion below the federal budget’s at $301 billion.

The views within the housing industry are mixed.

Harry Triguboff, the founder of Australia’s largest apartment developer, Meriton, reported that investors responded positively to the changes to negative gearing and CGT in the recent federal budget.

Triguboff claimed that the number of investors visiting Meriton displays had increased by 20%, the first such increase since the changes were announced.

He also believed the tax changes would create a boom in demand for new apartments.

Triguboff’s view has been echoed by other property developers, including Ben Stewart, director of SRM Residential, representing multi-billionaire developer Sam Arnaout, as well as several other property moguls.

“I’ve seen a definite increase in interest from investors in one and two-bedroom brand new apartments for negative gearing”, Stewart said.

“There’s a number of parties interested at The Walden by Aland in North Sydney there’s also definitely been an increase in activity with a number of deposits taken”.

By contrast, the Property Council of Australia (PCA) used its submission to a Senate inquiry into the federal government’s budget changes to CGT and negative gearing to oppose the reforms, arguing that independent modelling suggests that they will reduce dwelling starts by nearly 9,000 over four years.

The PCA argues that even with the new-build carve-out, the proposed changes fail to recognise that the established housing market and new housing supply are directly connected.

“If falling sentiment weakens established home prices more significantly than anticipated, the feasibility of new housing projects is undermined, and fewer homes will be built”, it says.

The PCA argues for maintaining the status quo because the overall budget will reduce the number of new homes built.

My view is that construction rates won’t increase unless there is more capacity in the sector and macroeconomic conditions improve.

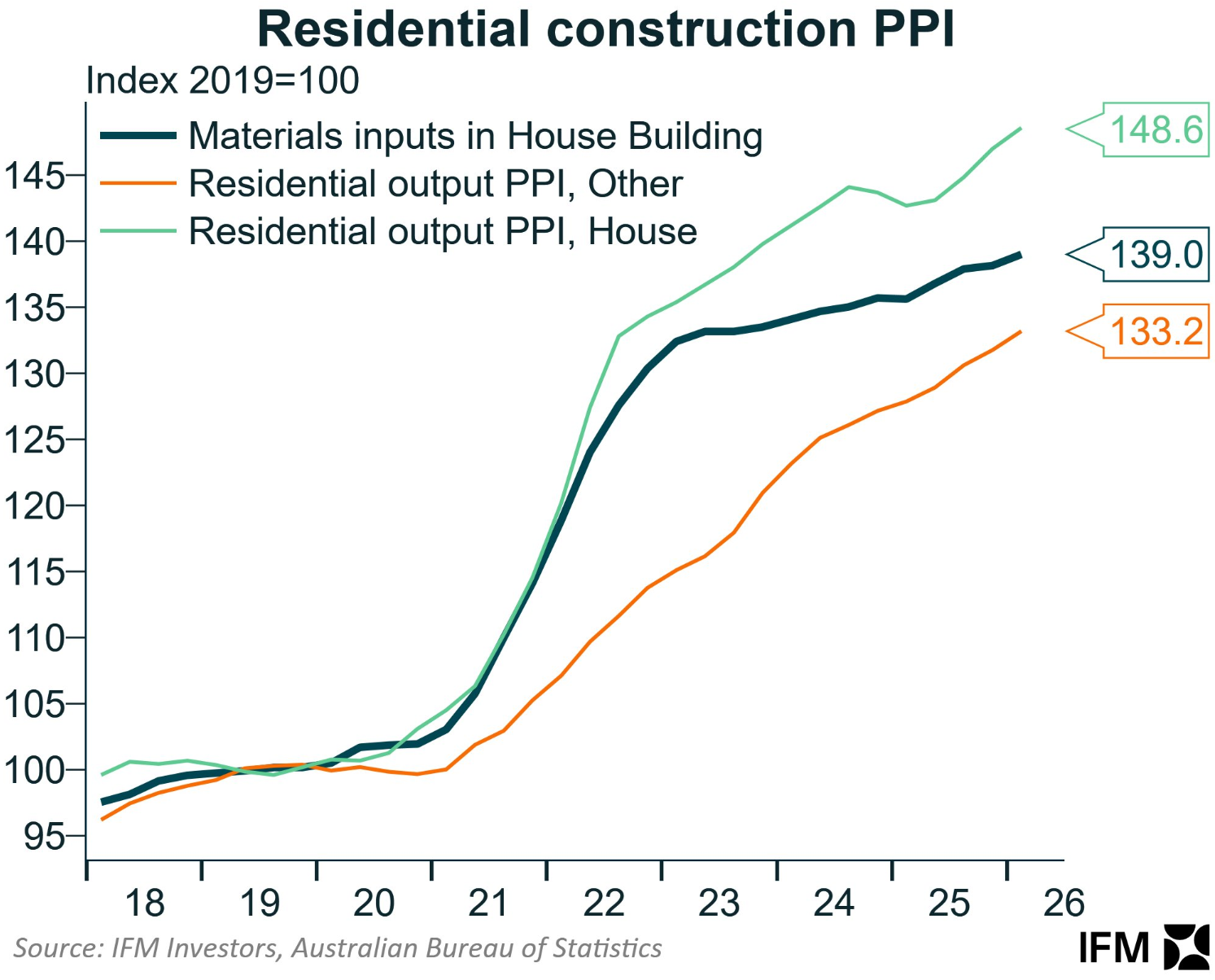

Residential construction costs have surged since the pandemic and are expected to rise further amid the war in the Middle East.

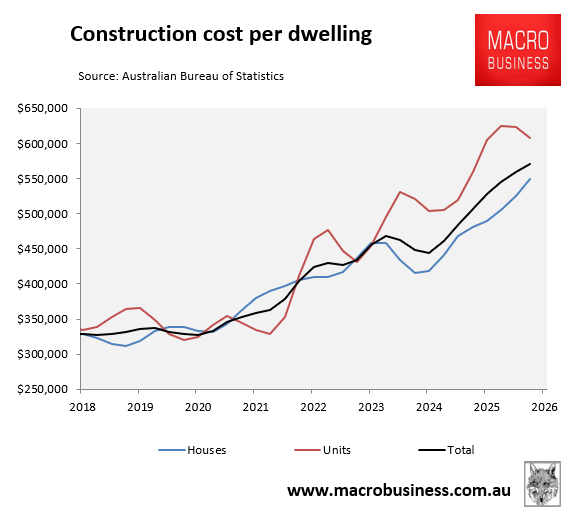

The construction cost per dwelling has shot higher, especially for apartments:

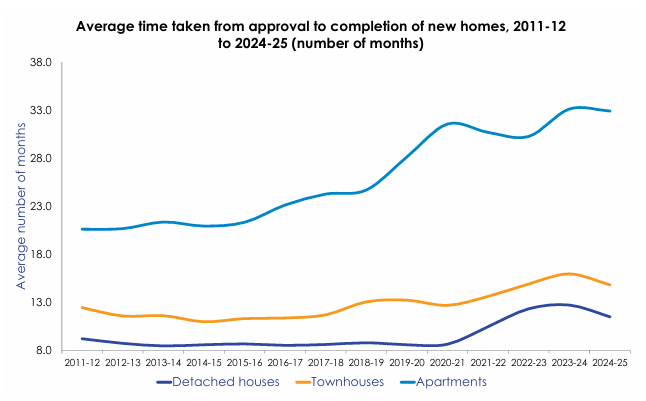

Rising costs, along with labour shortages, have caused a blow-out in the time taken to build housing:

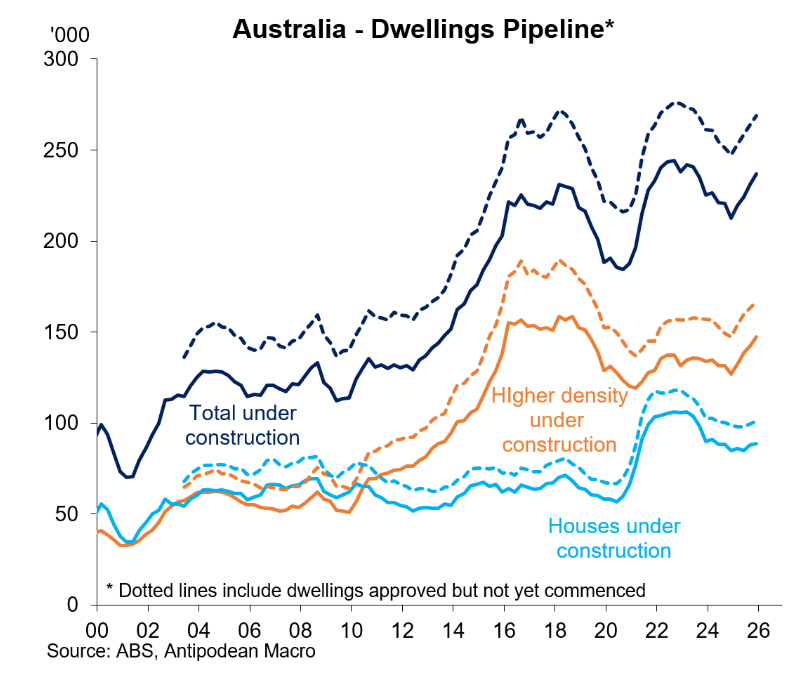

As a result, the pipeline of unfinished homes has swelled:

Finally, rising interest rates and falling dwelling values are acting as additional barriers to new construction.

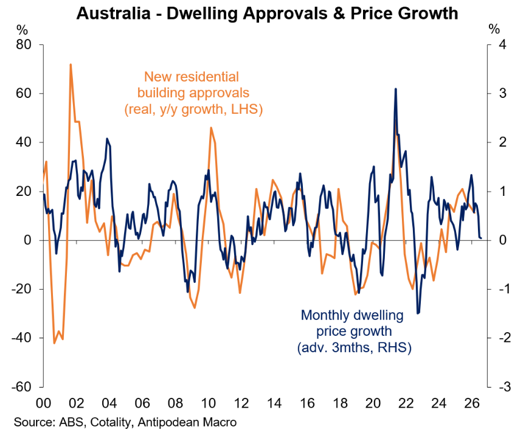

As illustrated below by Justin Fabo from Antipodean Macro, there has historically been a strong correlation between the growth in home prices and dwelling approvals:

The current downturn in dwelling values, therefore, portends lower construction.

The reality is that macroeconomic factors are working against housing construction. And the changes to negative gearing and CGT won’t make much of a difference.