So much for Asia’s renewable energy transition

I reported last week how Asia’s addiction to coal is driving the world’s carbon emissions.

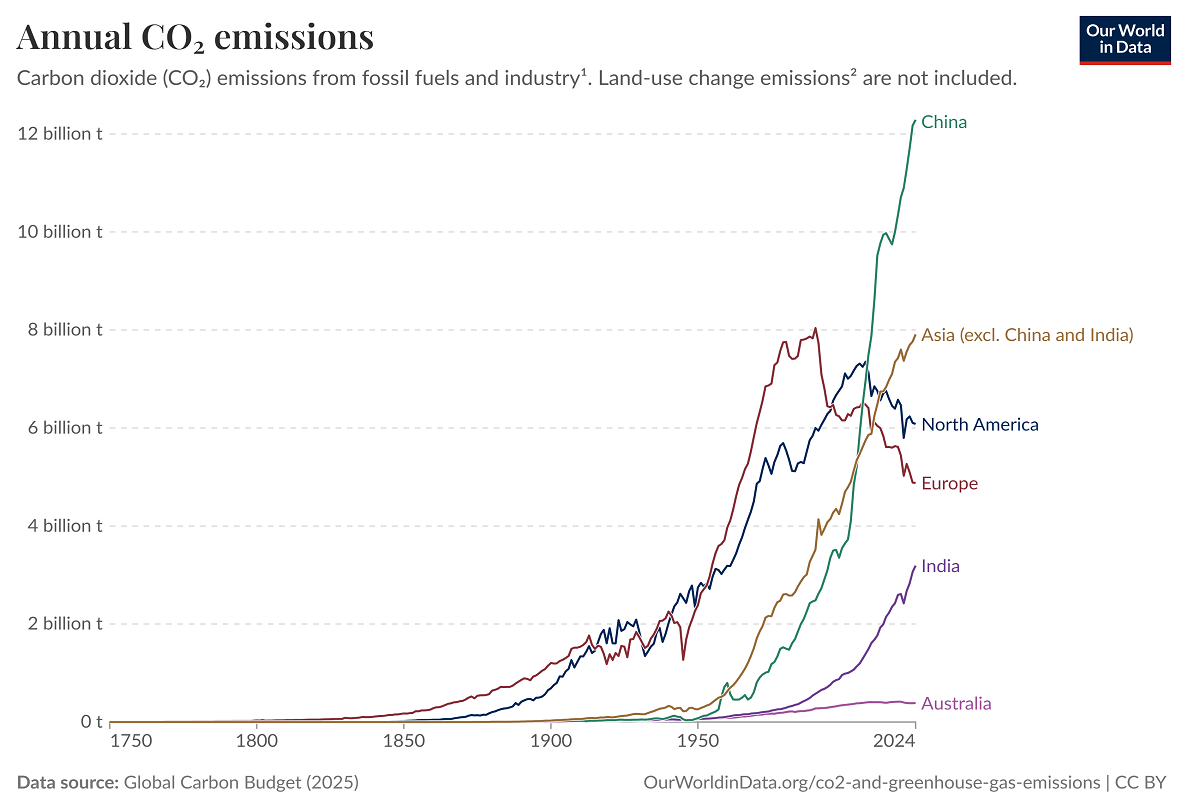

Asian nations combined have accounted for all of the increase in the world’s carbon emissions since the turn of the century and for 60.6% of total global carbon emissions in 2024.

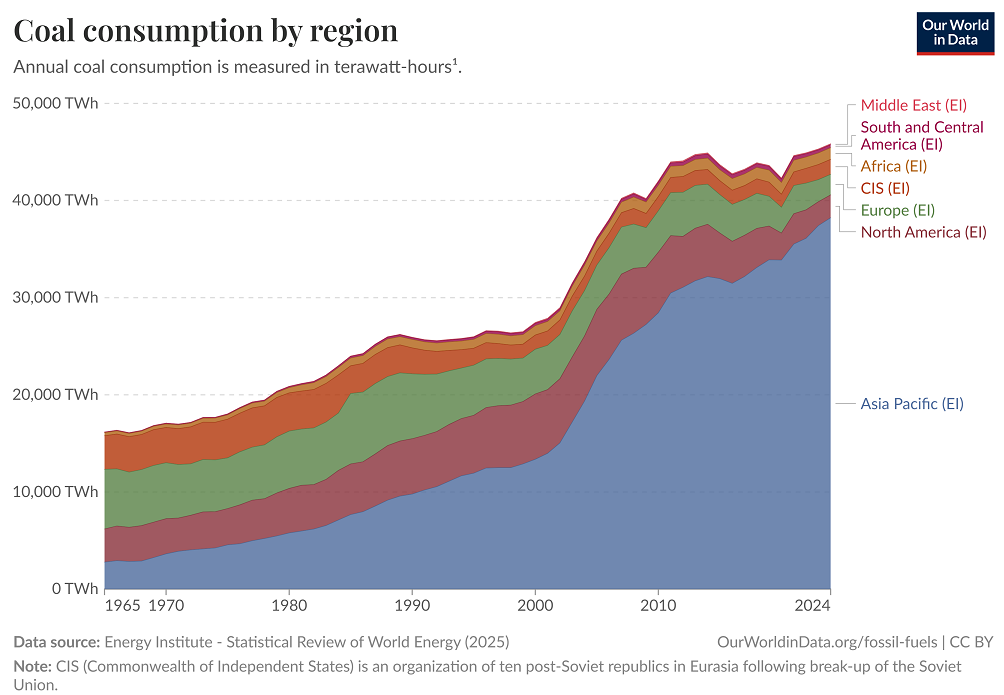

Asia’s consumption of coal has increased from 12.88 TWh at the end of 1999 to 38.23 TWh at the end of 2024, a 197% rise:

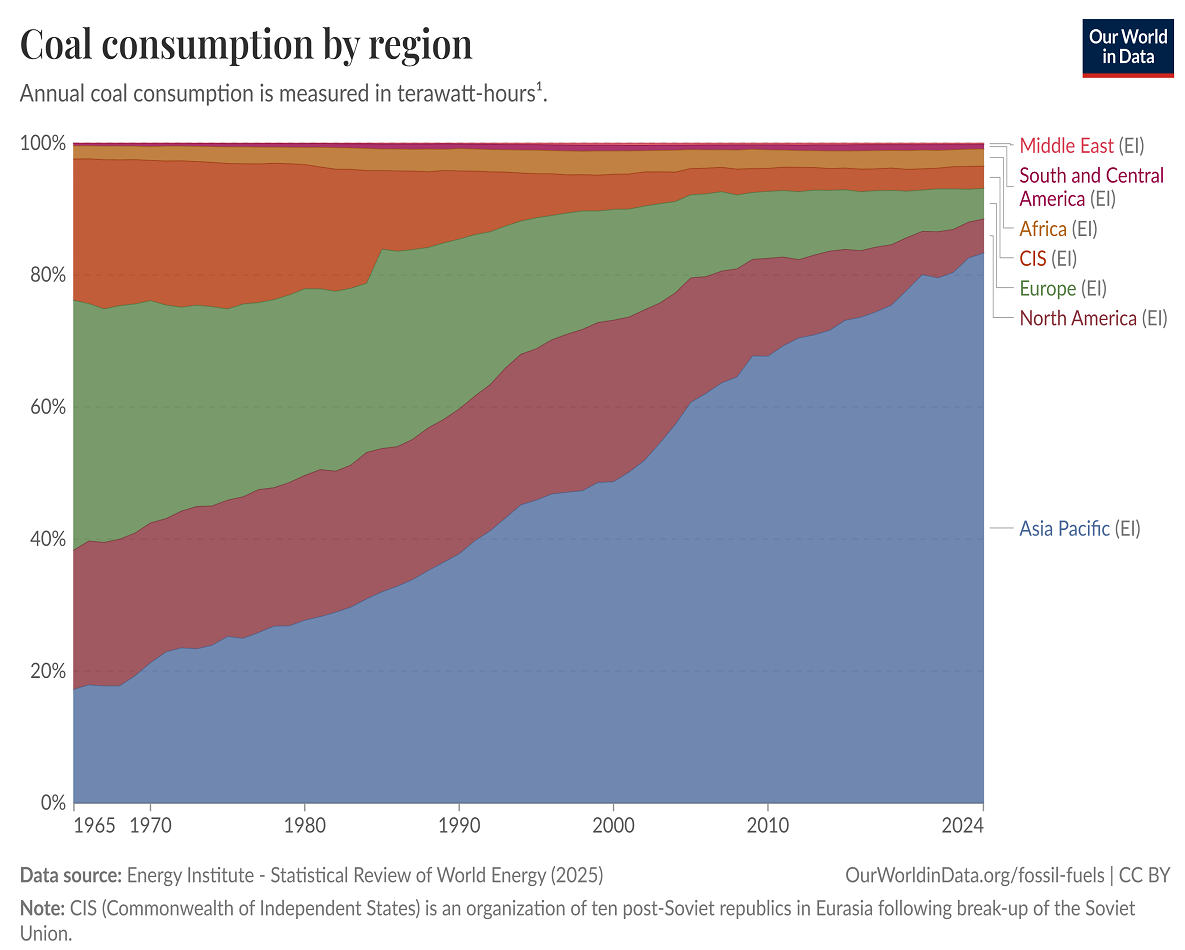

As a result, Asia accounted for 83% of the world’s coal consumption in 2024:

The International Energy Agency (IEA) reported that coal investment is set to rise 4% to $US180 billion ($253 billion) in 2026, the highest level of investment since 2012, driven by China.

Investment in coal production in 2026 is set to increase by 5% for thermal coal and 3% for the steel-making raw material, coking coal.

Rystad Energy forecasts that Asia is set for a major surge in coal use in 2026, driven not by policy reversal but by a severe LNG supply shortfall caused by Middle East conflict damage to Qatar’s Ras Laffan LNG complex.

Damage to Qatar’s Ras Laffan facility has removed 10.2 Mtpa of LNG supply to Asia. This has created a 35 Mt LNG shortfall in 2026 that the region “cannot easily replace”.

The Japan Korea Marker (JKM) LNG price has surged to near three‑year highs, discouraging gas use.

Rystad Energy projects around 70 million tonnes of additional coal demand in 2026 alone and 150 million tonnes of cumulative extra coal consumption through 2030, with half occurring in 2026.

This is not due to new coal plants; rather, existing coal fleets will be run harder.

Northeast Asia is driving the increase, namely:

- Japan: coal generation up 11%, gas output down 13%.

- South Korea: coal imports up 50%+ year‑on‑year.

- Japan: coal imports up 20%+ year‑on‑year.

Regulators in Japan and Korea have lifted caps on coal‑plant utilisation to maintain electricity supply. Utilities are prioritising energy security over emissions targets.

Rystad calls this “not a coal comeback, but a reality check” for Asia’s energy transition. These nations will significantly increase emissions and delay the region’s decarbonisation trajectory.

Australia increasingly isolated on ‘net zero’:

Australia only accounts for around 1% of the world’s carbon emissions. Yet it is busy deindustrialising through expensive energy and green/red tape.

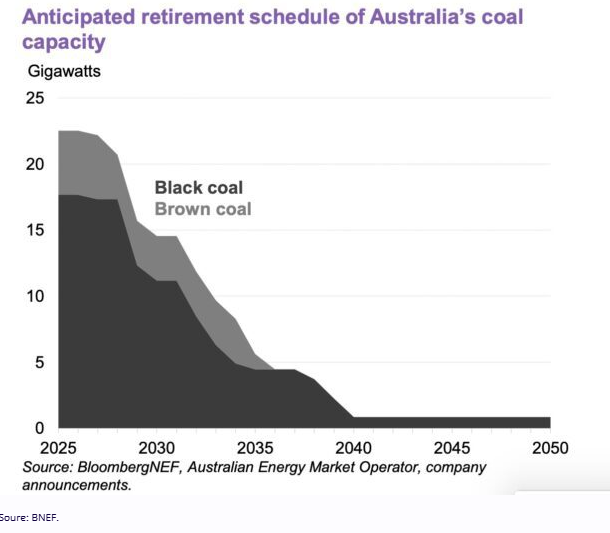

The Australian government plans to shut down baseload coal generation in favour of weather-dependent solar and wind, backed by batteries, pumped hydro, and gas:

The coal closures are expected to coincide with a surge in Australia’s energy demand, driven by the following factors:

- A forecast increase in population of nearly 50% in only 40 years;

- The electrification of the vehicle fleet;

- The mass build-out of energy-hungry data centres, which require stable 24/7 power that only non-weather-dependent sources like coal generation can provide; and

- The build-out of water desalination plants to cater to population growth and data centres.

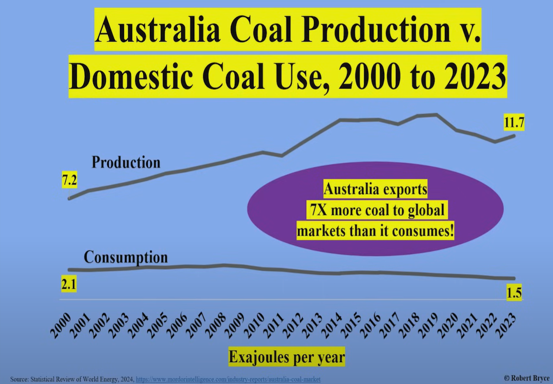

It makes no sense for Australia to be the world’s largest coal exporter to Asia but to refuse to burn it ourselves.

Australia should prioritise energy affordability and security over ‘net zero’ concerns.

Global carbon emissions would be unchanged if Australia used more coal domestically rather than exporting it to Asian nations that are rapidly increasing their consumption.