The fatal flaw in Labor’s capital gains tax reform

Last week’s federal budget announced fundamental changes to Australia’s negative gearing and capital gains tax regimes, summarised below.

Negative Gearing:

From 1 July 2027, negative gearing will only apply to newly built residential properties.

Existing properties purchased before 12 May 2026 are fully grandfathered — no change to current rules.

Policy intent: push investor demand away from established homes and towards new housing supply.

Capital Gains Taxes:

From 1 July 2027, the current 50% CGT discount for individuals, trusts and partnerships will be abolished and replaced with:

- Cost‑base indexation (tax only the real, inflation‑adjusted gain)

- A minimum 30% tax rate on capital gains.

Gains accrued before 1 July 2027 will keep the 50% discount (grandfathered).

New builds retain access to the existing 50% discount or can use indexation (whichever is better), giving them a tax advantage.

Policy intent: tax real gains fairly, reduce investor advantages over wage earners, and redirect capital towards new housing.

The Good:

One of the most positive impacts from the changes is that it will reduce investor demand from the established housing market, thereby putting some downward pressure on home prices and creating a better environment for first home buyers.

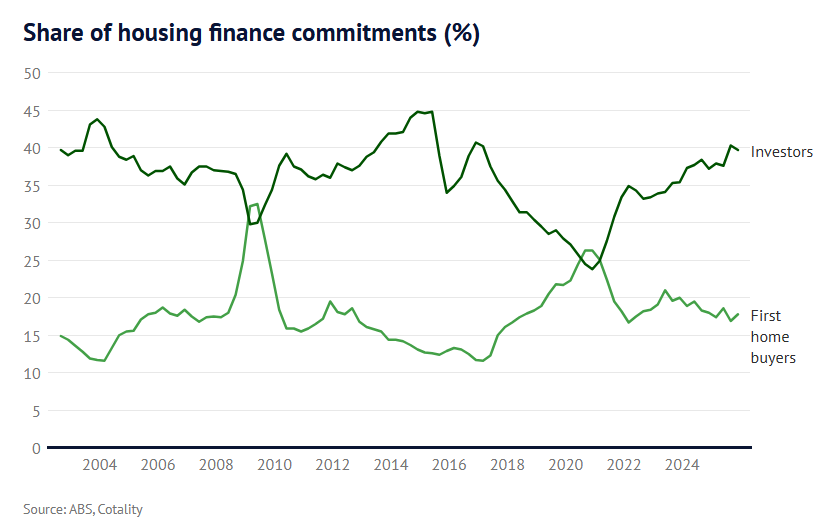

As illustrated below, investors have historically competed directly with first home buyers for housing:

Therefore, by reducing investor participation, the share of first home buyers in the market should increase, alongside the home ownership rate.

The Bad:

The minimum 30% tax rate on real inflation-adjusted capital gains has clearly been targeted to squeeze revenue from self-funded retirees since those receiving government payments (e.g., a partial pension) are exempt.

Targeting those who have accumulated assets through their working lives and then sell them off to fund their retirements with a 30% minimum tax rate seems overly harsh.

Moreover, the changes will adversely impact lower-income earners, such as those buying shares to save up for a housing deposit.

The Ugly:

The CGT changes are slated to apply to all investments, which risks stifling entrepreneurship, investment and productivity at a time when business investment is already near historical lows.

Starting a business is incredibly difficult and risky:

- You take a huge risk, investing a lot, knowing that you have a high chance of failure.

- You work your backside off and usually go through some dark times.

- Your family takes a hit while you put everything into the business.

- You go without a decent salary usually for a few years.

- Family and friends often rely on you as they often invest too (which itself brings lots of stress).

- Then you hope you get a reward at the end (mostly just pay back of everything you’ve invested), which the government now wants to take a bigger chunk of.

Why bother taking a risk, going without a salary for years, etc., only for the government to become a major shareholder on sale (on the slim chance that you succeed)?

Source: SUR Direct

The CGT changes should be carved out for new businesses and venture capital, as they are going to kill entrepreneurship, investment and productivity, which is the last thing that Australia needs.

Thankfully, the budget fact sheet accompanying the changes noted the following:

“Given the unique characteristics of the tech and start up sector the Government will consult on the interaction of the capital gains tax reforms and incentives for investment in early-stage and start-up businesses”.

Let’s hope that the government comes to its senses and carves out start-ups and venture capital from the CGT changes.

Otherwise, the Australian economy will suffer as entrepreneurship dies, investment goes offshore, and productivity and dynamism collapse.