Property investors have been a major driver of the recent boom in Australian home prices.

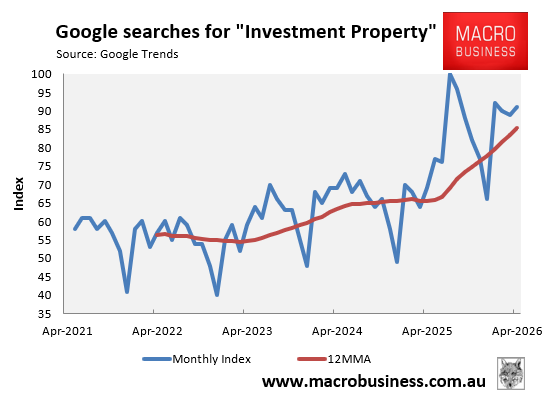

In the second half of 2025, Google searches for “investment property” surged, then slowed in the early months of 2026, though they remained strong.

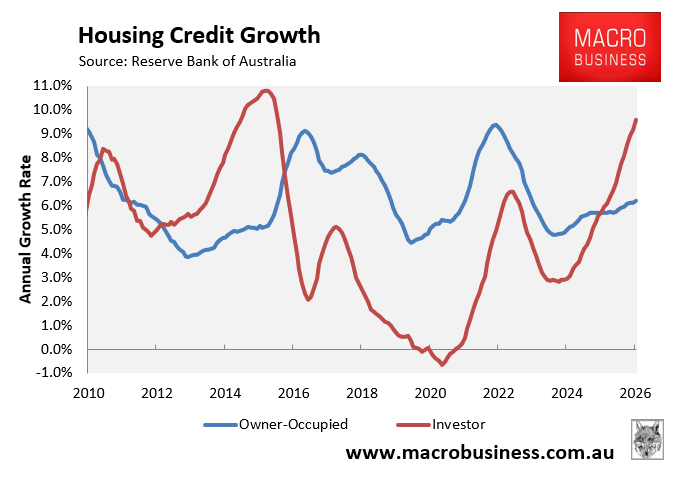

The latest credit aggregates data from the Reserve Bank of Australia (RBA) showed that annual investor mortgage growth reached its highest level since September 2015 at 9.6%, easily exceeding the 6.2% growth in owner-occupier mortgages.

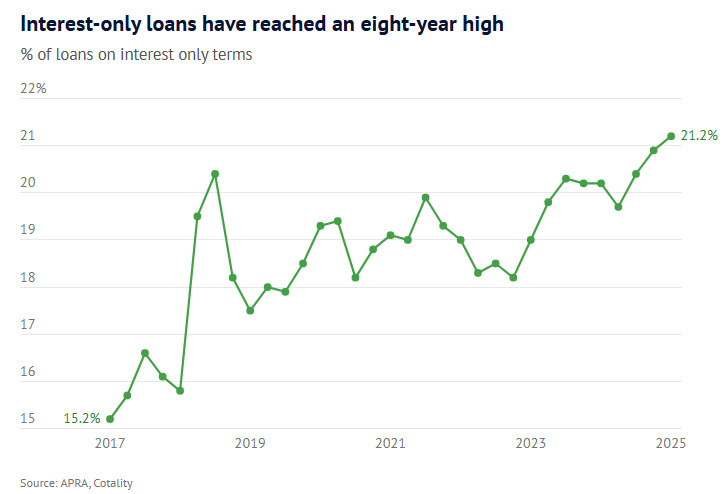

Domain reported this week that interest-only home loans now make up 21.2% of all new lending, the highest share since 2017, driven by investors:

Investors now account for 40.3% of new home lending by value (up from 27.9% six years ago). Because investors could negatively gear, offsetting losses against taxable income, it made financial sense to borrow on an interest-only basis, despite paying higher interest rates.

However, the 2026 federal budget’s changes to negative gearing and capital gains taxes are expected to cool investor demand, likely pulling interest-only lending back down.

“An interest-only loan gives you cash flow while you’re repaying an asset that’s going up in value”, Herron Todd White chief economist Cameron Kusher said.

“They will potentially decrease because there will be less negative gearing”, said Kusher. “We’re likely to see fewer investors as a result of that too”.

Indeed, the combination of higher interest rates, less generous CGT rules, and the ban on negative gearing for established homes is highly likely to lead to significantly lower investor demand in the future and, in turn, lower house price growth.

Australian lenders have already tightened borrowing capacity for investors by changing how they assess after‑tax cash flow and serviceability.

Because losses on established properties purchased after budget night can no longer be deducted against earned income, lenders now model lower after‑tax cash flow for these borrowers.

The change is material because serviceability tests rely heavily on net disposable income.

“With 30% less borrowing power, investors will be removed from (contention) for a lot of properties”, said Refinance.com.au director Aidan Hartley.

A buyer’s agent friend of mine informed me that one of their investor clients had a verbal agreement with a lender to borrow $800,000, which was later reduced to $500,000 following changes to negative gearing in the federal budget.

Leading Sydney auctioneer Tom Panos warned that suburbs “packed with investors” are facing a day of reckoning:

“If investors suddenly think, “Hang on, the tax benefits are changing, borrowing capacity is shrinking, growth may slow, then fewer investors will buy after me’. Then demand is going to dry up quickly”.

“And if existing investors start offloading at the same time that fewer investors enter the market, that’s when you get pressure on prices”.

Thus, higher interest rates and the budget’s taxation are a ‘perfect storm’ for the housing market.

One major positive is that prospective first-home buyers should benefit from lower investor participation and prices.

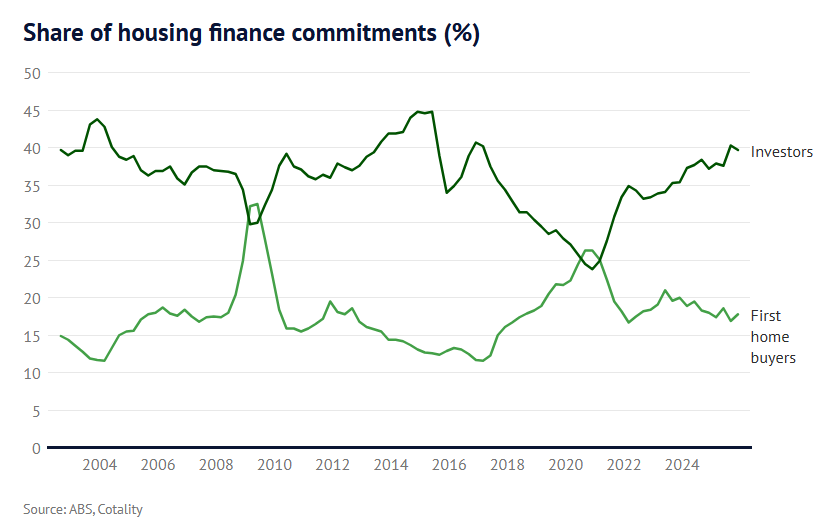

As Domain illustrates below, investor demand has historically correlated inversely with first-home buyer demand:

As a result, the reduction in investor demand arising from the budget’s tax changes should drive increased participation from first-home buyers, raising the homeownership rate.