“Booming government spending” will force RBA to hike again

Before the war in the Middle East began in late February 2026, Australia’s underlying inflation was already well above the Reserve Bank of Australia’s (RBA) target band of 2% to 3%.

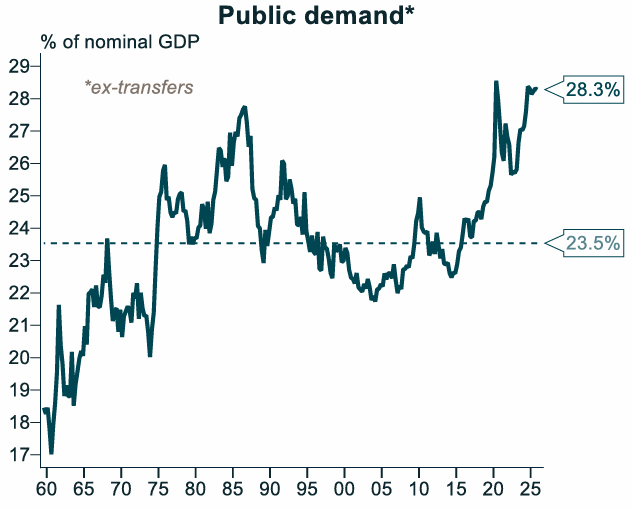

This high inflation prompted the RBA to lift the official cash rate by 0.25% in February, with many blaming record levels of public spending for driving aggregate demand ahead of supply and fueling the inflationary pressures.

Chart by Alex Joiner (IFM Investors)

RBA governor Michele Bullock warned last week that when the economy is already facing capacity pressures, any additional public spending adds to aggregate demand, making the RBA’s job harder.

“When inflation is already too high, and the economy is facing capacity pressures, it doesn’t take much additional spending to make the job of returning inflation to target more challenging”, she said.

This is Bullock’s clearest statement linking government spending to inflation.

In a recent parliamentary hearing, Bullock explicitly agreed that high levels of government spending have contributed to inflation by increasing demand for goods and services:

“Yes, it does… It’s all part of aggregate demand… Total demand is too high, and that’s what’s giving inflationary pressures”.

Bullock has also cautioned that broad-based government cost-of-living support risks adding to inflation. And the RBA will respond with higher interest rates:

“If we need to put up interest rates to slow the growth in demand… then that’s what we will do”, she said.

Bullock’s recent messaging is unambiguous: government spending is contributing to excess demand and therefore to inflation, and additional spending—especially broad cost‑of‑living measures—risks making inflation harder to control.

With this background in mind, UBS chief economist George Tharenou says he expects the RBA to lift interest rates again, most likely in August, resulting in a cash rate of 4.6%. However, he does not rule out an increase in June, following the budget, due to what he contends is “booming government spending”.

“The budget overall remains stimulatory”, said Tharenou.

“The main driver of that is spending growth, which has been booming”.

“Interest rates are likely to stay higher for longer”, he said.

While soaring global energy prices are playing a role, profligate spending by federal and state governments is also driving inflation higher, as are excessive immigration levels.

Government policy is working at cross-purposes to the RBA. As a result, we have what Tarric Brooker has long described as a “burnout economy”.

The RBA has its foot planted on the brake with contractionary monetary policy, while governments have their foot planted on the accelerator with expansionary fiscal policy.