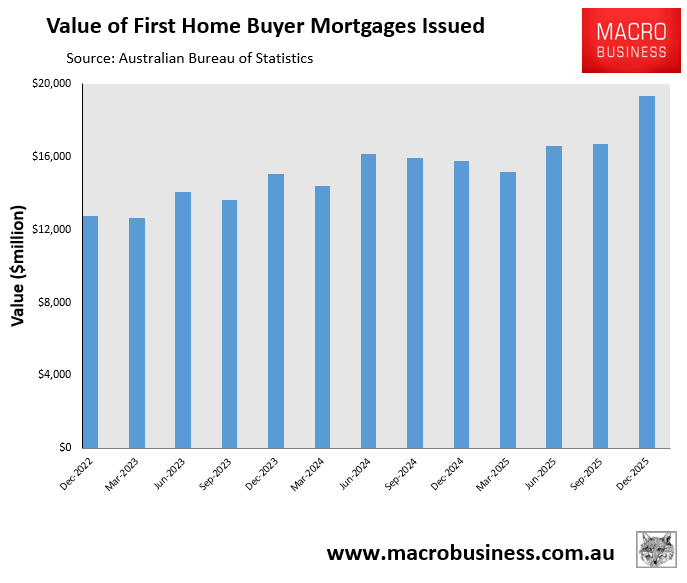

According to the most recent Australian Bureau of Statistics (ABS) housing finance data, $19.310 billion in mortgages were issued to first-time home buyers during the December quarter of 2025. This was a 16% gain over the previous quarter and the highest value since the first quarter of 2021:

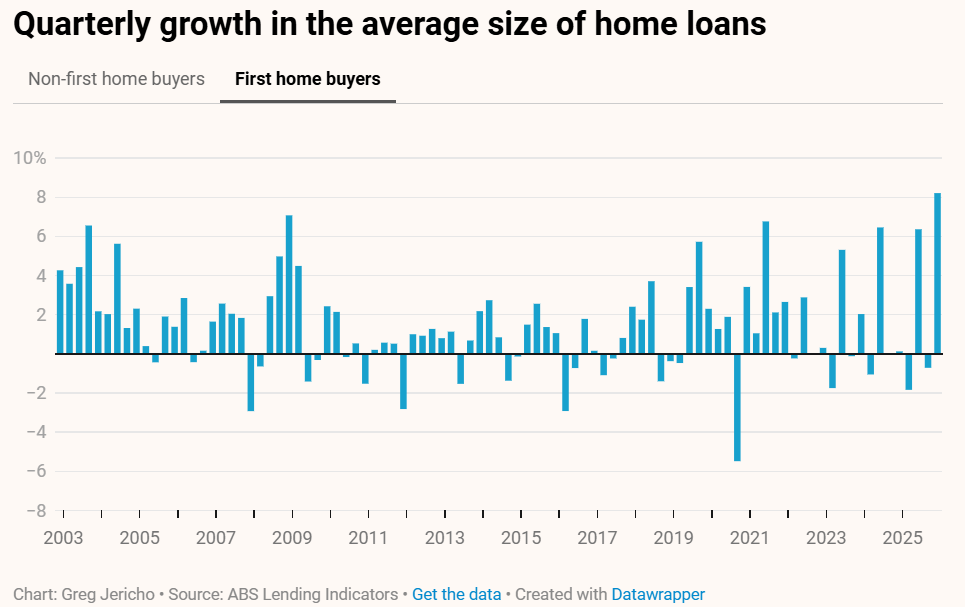

The average size of first home buyer mortgages also increased by a record 8.3% in the December quarter of 2025, to a new high of $607,500:

Chart by Greg Jericho at The Guardian

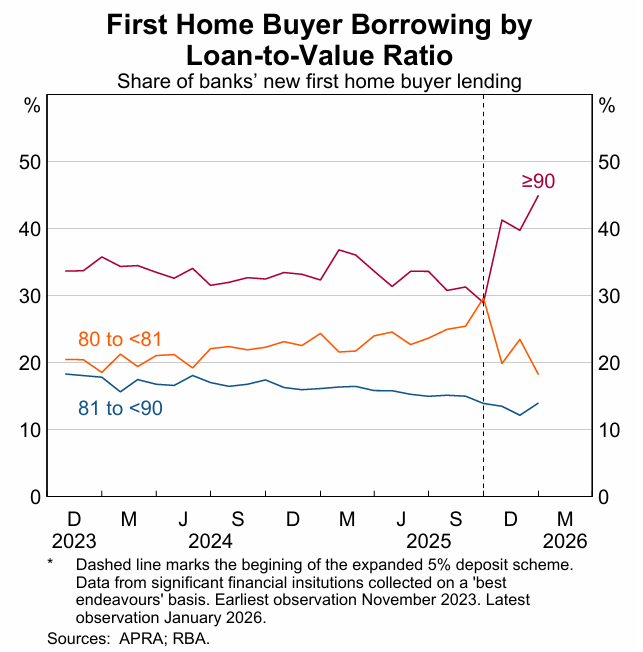

It was revealed that 22,921 guarantees were provided under the federal government’s 5% mortgage deposit scheme for first home buyers in the four months following its expansion on October 1, 2025.

This represented a 75% increase over the previous four-month period, June to September, when 13,105 guarantees were granted.

The Reserve Bank of Australia’s (RBA) latest Financial Stability Review also reported a sharp increase in high-loan-to-value-ratio (LVR) mortgage lending to first home buyers following the introduction of the expanded 5% deposit scheme.

Diana Mousina, AMP’s deputy chief economist, told the ABC that the data for the four months to January showed a “massive jump”.

“We know that incentives really matter in the housing market”, she said. “Whenever we get some sort of grants or discounts, we always see a big take-up of these things”.

The expanded 5% home deposit scheme was marketed by the federal government as an affordability measure. However, economists warned that these types of demand-side measures are always self-defeating from an affordability perspective, since they inevitably push home prices higher, thereby making housing less affordable.

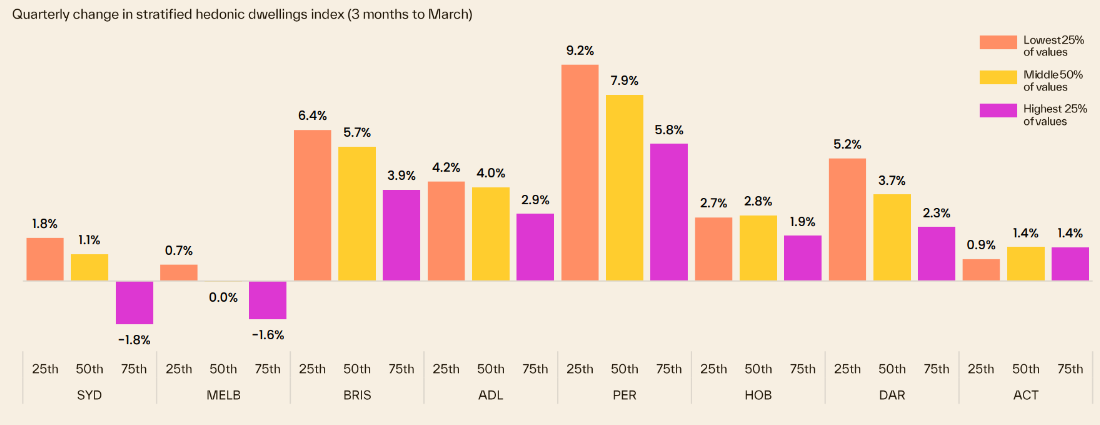

Cotality’s latest housing chart pack illustrates this point. As shown below, price growth for properties valued at the bottom 25% quartile, which fall well within the 5% deposit scheme’s price caps, grew the strongest in the three months to March 2026 across every major capital city market:

Source: Cotality

By contrast, the most expensive 25% of homes, which fall outside of the price caps, experienced the weakest price growth across every capital city market except the ACT.

Thus, the 5% deposit scheme simply drove up the price of entry-level homes, ultimately making them more expensive for first home buyers.

Future first home buyers will face the prospect of paying more for housing and holding larger mortgages than they otherwise would have without the 5% deposit scheme.