The threat of rising interest rates, low yields, and the expected unwinding of property tax concessions has led to a sharp decline in investor demand for housing.

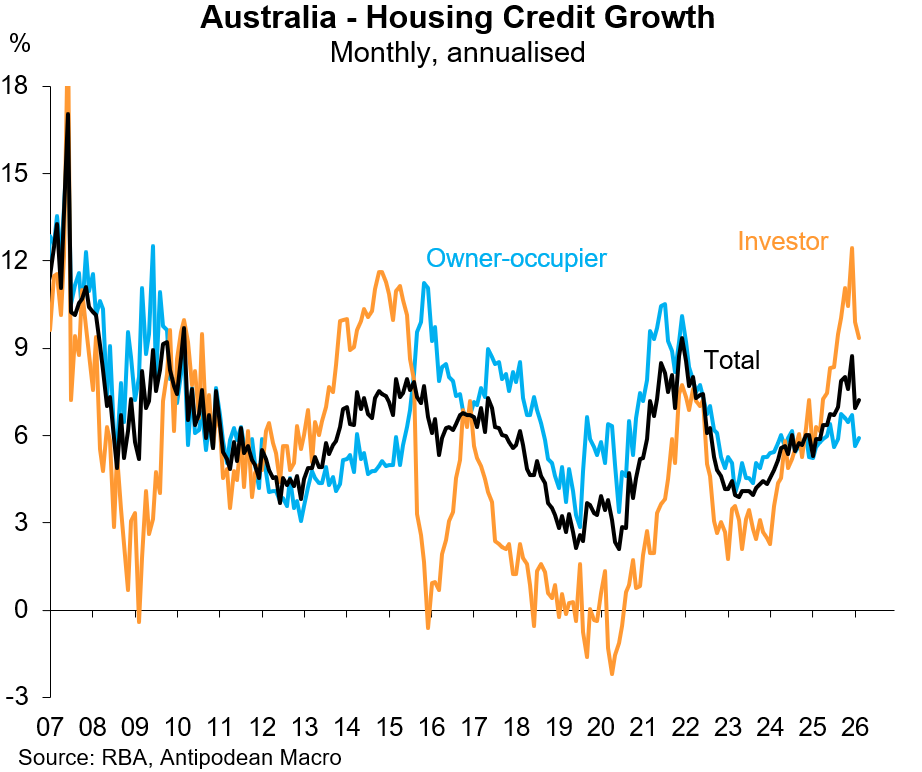

On Tuesday, the Reserve Bank of Australia (RBA) released credit aggregates data for February, showing that housing credit in Australia grew by 0.58% in February, down from the recent peak of 0.65%.

The decline in overall housing credit growth has been driven by investors, where growth fell to 0.75% in February, down from a recent peak of 0.98% in December 2025:

Chart by Justin Fabo from Antipodean Macro

This data captures the first 25 bp interest rate hike from the RBA, delivered on 3 February 2026.

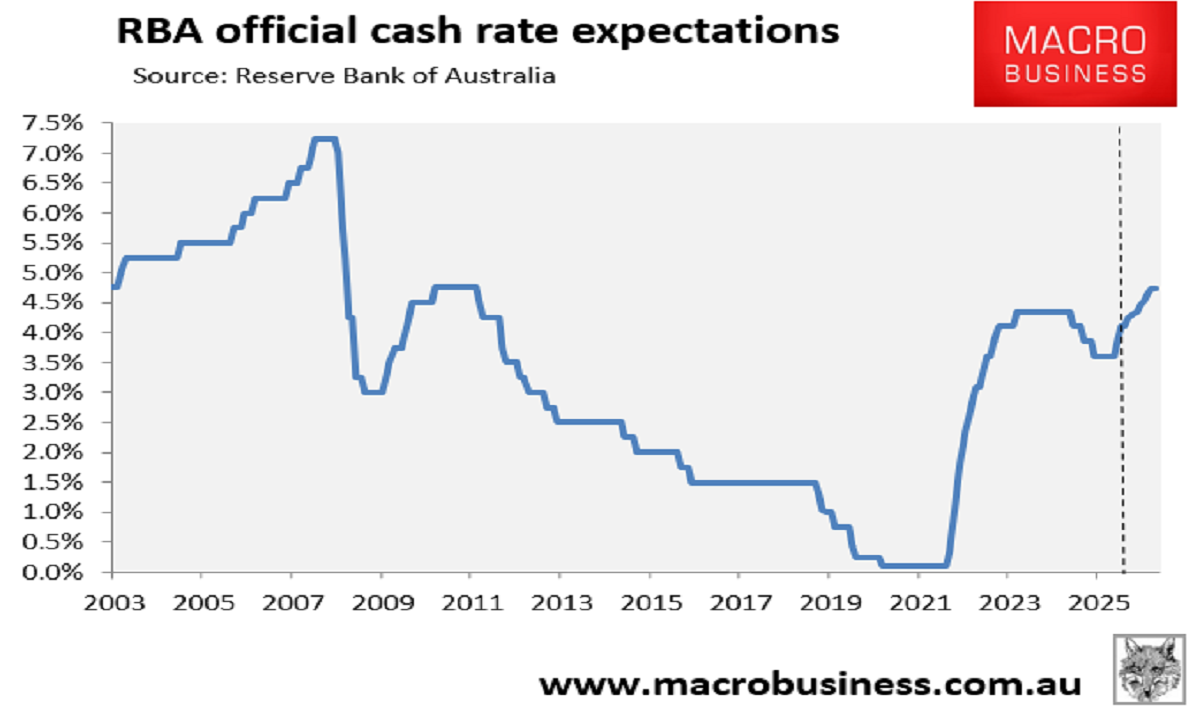

The RBA followed up with another hike in March, and the interest rate futures market expects a further three 25 bp rate hikes this calendar year, which would lift the official cash rate to an 18-year high of 4.85%:

The associated higher mortgage rates increase financing costs, reduce borrowing capacity, and place downward pressure on home prices, reducing overall housing demand.

Investor demand is also likely to be curtailed by expectations that the Albanese government’s May federal budget will deliver reforms to the Capital Gains Tax (CGT) discount and possibly negative gearing, reducing after-tax returns to investors.

While the exact make-up of these policy changes is uncertain, they are likely to have dented investor sentiment in the housing market.

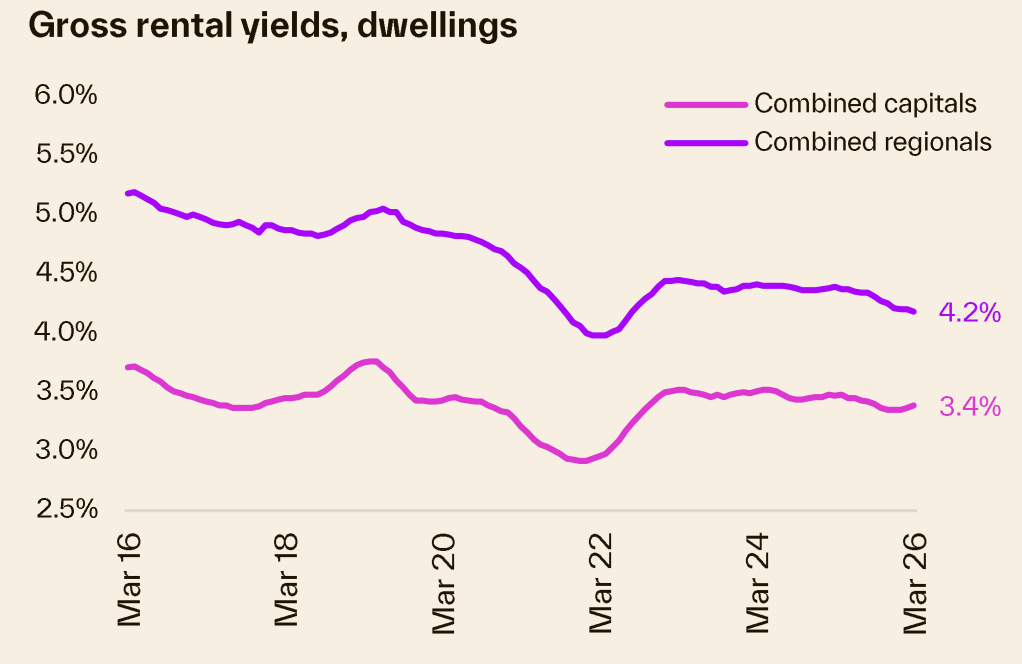

Finally, gross rental yields in the Australian property market have trended lower and are tracking at a low level of only 3.57% nationally in March, down from 3.69% a year earlier:

Source: Cotality

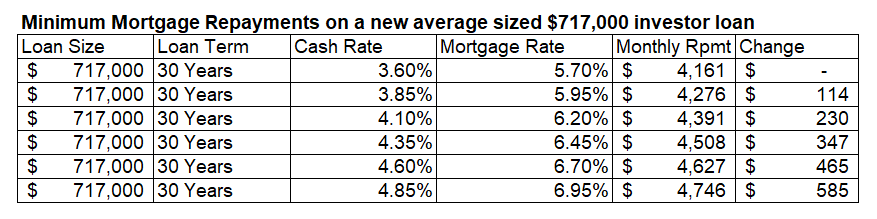

The gross rental yield of 3.57% in March is well below the current average investor mortgage rate of 6.20%, which will increase to 6.95% if the RBA delivers three more rate hikes this year:

The average prospective investor would, therefore, be heavily negatively geared at a time when the federal government is seeking to limit property tax concessions.

It is no wonder, then, that investor demand fell sharply in February, which was likely replicated in March and will soften in the period ahead.