According to media reports, the upcoming federal budget will change the capital gains tax (CGT) from its current 50% discount on nominal gains to the pre-1999 method of taxing 100% of real, inflation-adjusted gains.

The new CGT regime would apply to all assets, not just property.

Returning to the pre-1999 method of calculating CGT offers several benefits for tax efficiency, fairness, and budget sustainability.

Because only real profits were taxed, this system remained neutral during inflation cycles and avoided inflation-induced distortions.

It was also more equitable than the existing 50% discount approach, as it taxed real gains at full marginal rates and was less favourable to high-income households.

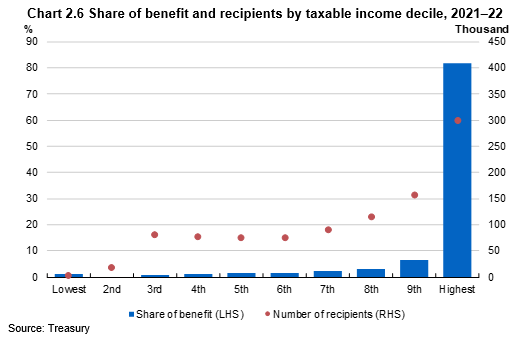

According to the Treasury, the top 10% of households capture more than 80% of CGT discount benefits under the current system:

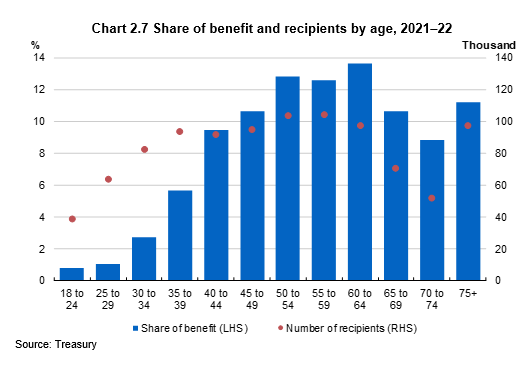

These recipients tend to be older. Hence, the existing CGT discount has a detrimental impact on intergenerational equity:

The pre-1999 system is also better for the federal budget since it is less vulnerable to asset bubbles and generates more consistent revenue. Taxing real profits will also generate more income during periods of low inflation.

Finally, the pre-1999 CGT system was significantly less distorting for housing because it did not provide a particular tax break for capital gains over wages, thus decreasing speculation.

Taxing real gains would also discourage short-term speculation and asset flipping by encouraging investors to hold assets for an extended period.

Don’t overcomplicate reform:

While there are clear benefits in moving back to the pre-1999 CGT system, the AFR’s Phil Coorey suggests that pre-existing assets could be subject to both CGT regimes.

“In this scenario, the existing 50% discount would apply to the capital gain on an asset acquired after 1999. Any subsequent capital gain made after the switch to the new tax regime comes into effect would be subject to the indexation-based deduction. This model would tax real gains adjusted for inflation over the life of the asset”, Phil Coorey wrote.

Such an approach could be a compliance nightmare, as it would require every asset, including about 2.5 million investment properties, to be valued at the changeover point between the two taxation regimes.

Housing Industry Association chief economist Tim Reardon said those who would benefit most would be the valuers.

My view is that existing investors should be grandfathered under the old rules.

Grandfathering existing investors would not lead to significant revenue losses versus non-grandfathering, because the longer existing investors take to sell, the more their nominal gains (taxed under the 50% CGT discount system) would be eroded by inflation.

The current 50% CGT discount benefits those who make their gains quickly and sell in a relatively short period of time versus those that hold assets for the long term, since there is less time for real gains to be eroded by inflation.