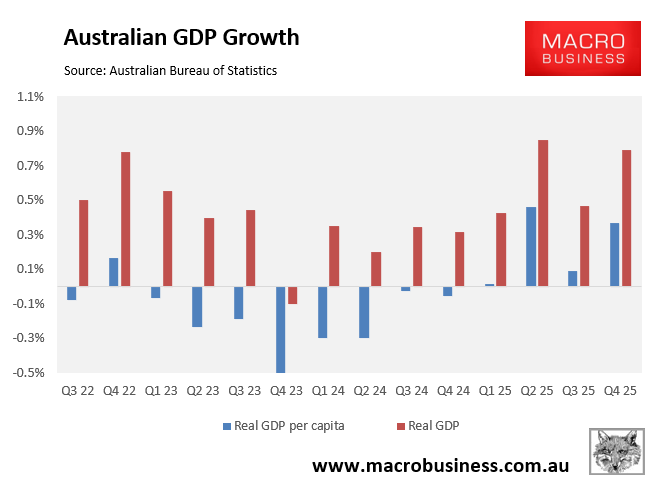

The Australian Bureau of Statistics (ABS) released national accounts data for the December quarter, which printed headline real GDP growth of 0.8% over the quarter and 2.6% year-on-year. The result beat expectations of 2.2% growth.

Thanks to backward revisions, per capita GDP has now grown for four consecutive quarters, rising by 0.9% in 2025, the highest through-the-year growth since the December quarter of 2022.

However, Australia’s real per capita GDP was still tracking 0.5% below its June quarter 2022 peak.

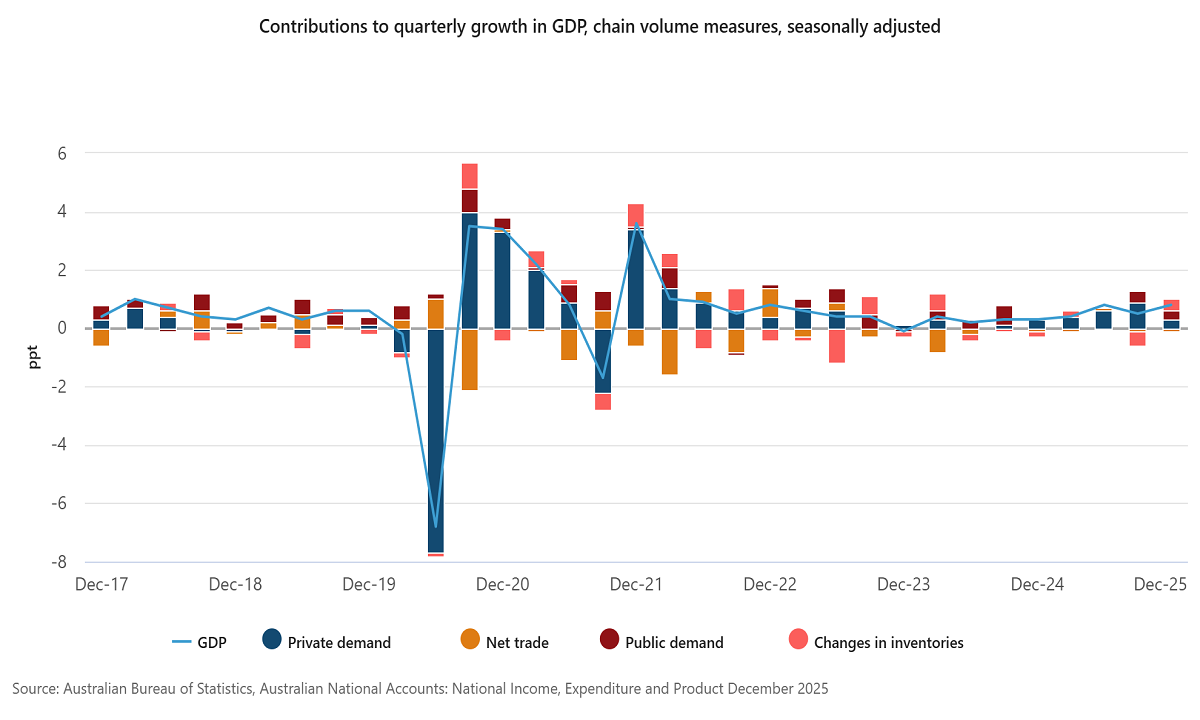

“There was broad-based economic growth in the quarter, with rises observed in a large majority of industries. Public and private demand each contributed 0.3 percentage points to GDP growth”, noted Grace Kim, ABS head of National Accounts.

The result is certain to bolster the view that Australia’s economy is operating above capacity, which is helping to fuel inflation.

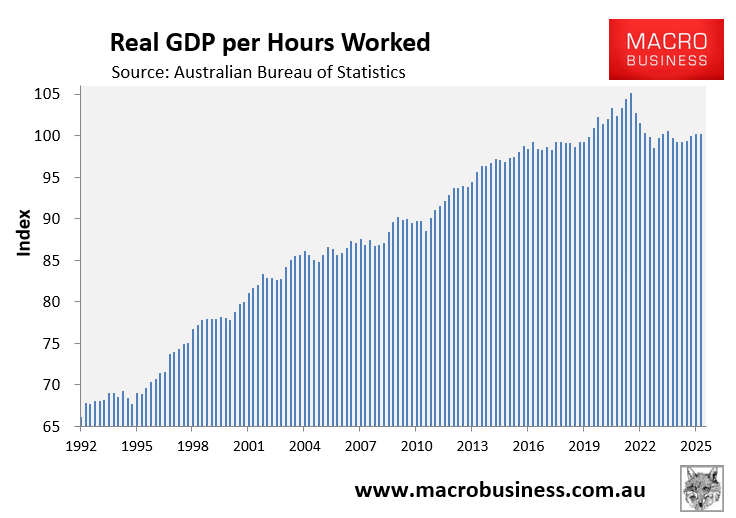

While labour productivity (GDP per hour worked) rose by 1.0% in 2025, it remains 4.7% below its March quarter 2022 peak:

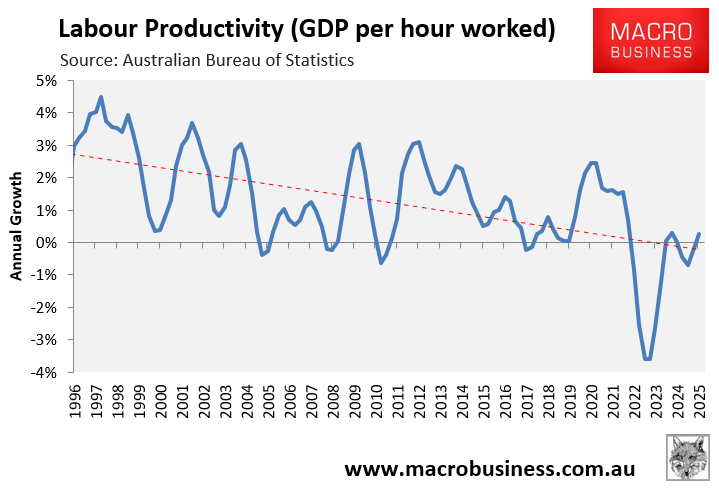

In fact, Australia’s labour productivity growth has trended down sharply over the past 30 years:

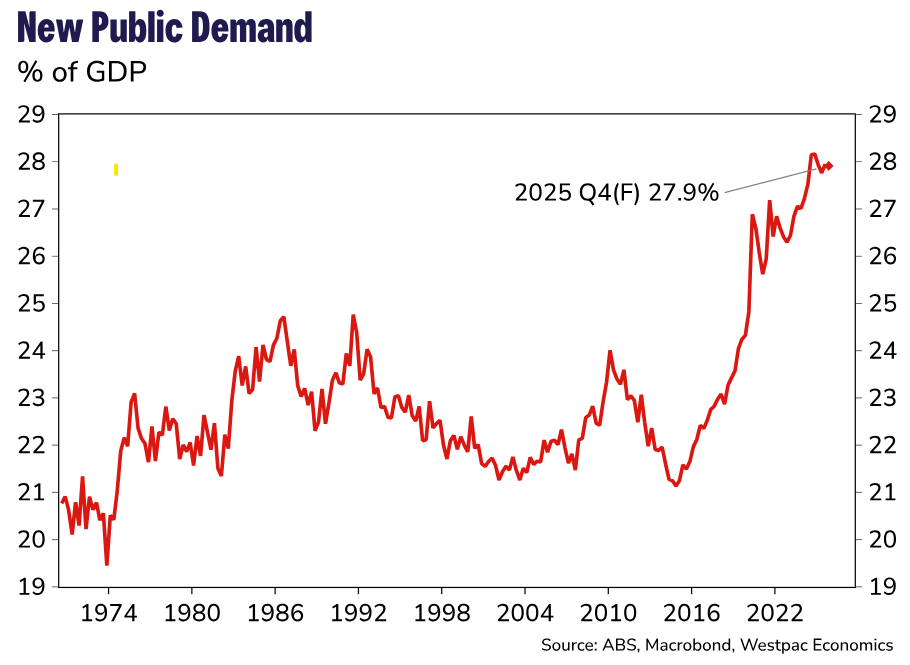

Australia’s federal and state governments are certainly not helping the inflation situation, given that public demand is tracking at a historically high share of GDP over the December quarter.

Put simply, Australia’s federal and state governments need to stop overstimulating the economy and placing upward pressure on inflation.

The situation is now even more critical, given the conflict in the Middle East, which threatens to send Australian petrol/diesel, gas, and electricity prices soaring, spiking energy inflation.

The Reserve Bank of Australia (RBA) is facing a nightmare scenario of embedded inflation driven by reckless government policy and cost-push energy inflation imported from abroad.

If it hikes too hard in a bid to stem inflation, the RBA risks pushing the economy into recession.