Author Mark Twain once famously said, “History doesn’t repeat itself, but it often rhymes”.

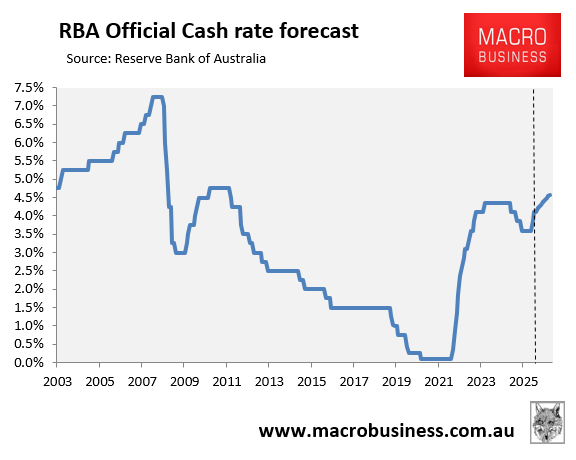

We are witnessing such an event following the RBA’s back-to-back interest rate hikes, which have taken the official cash rate to 4.10%.

The interest rate futures market has also priced two additional rate hikes for 2026, which would take the official cash rate to 4.60% by year’s end:

You will see from the above chart that the RBA hiked aggressively in the lead-up to the 2008 Global Financial Crisis (GFC).

The subprime mortgage crisis hit the US in the second half of 2007. Despite this, the RBA hiked the official cash rate by 1.0% (from 6.25% to 7.25%) over seven months, only to then rapidly slash rates by 4.0% when the full-blown GFC hit in September 2008, following the collapse of Lehman Brothers.

I feel that the RBA is setting itself up to repeat the same mistake.

The global energy shock, while inflationary, appears increasingly likely to drive the world into recession.

The war in the Middle East is not going as planned for the US, and it appears that the Strait of Hormuz, which supplies about 20% of the world’s tradeable oil and gas, will be effectively closed to cargo traffic indefinitely.

This means that global energy prices – oil and gas, in particular – will continue to rise, driving global inflation and crimping growth via demand destruction.

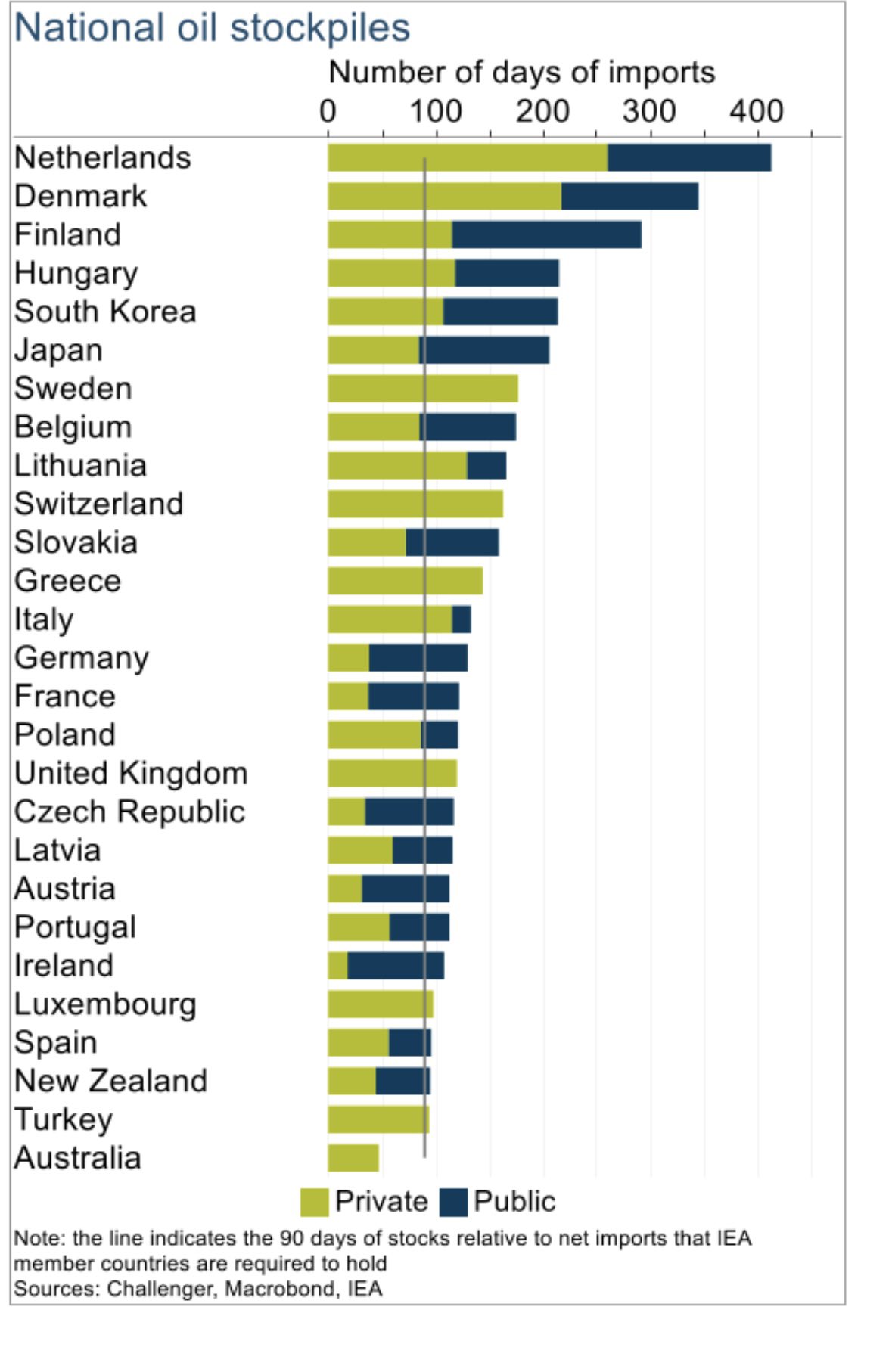

Australia’s low storage and high dependence on liquid fuels make its economy particularly vulnerable, especially given its heavy dependence on diesel across mining, freight, agriculture, essential services, and backup power generation.

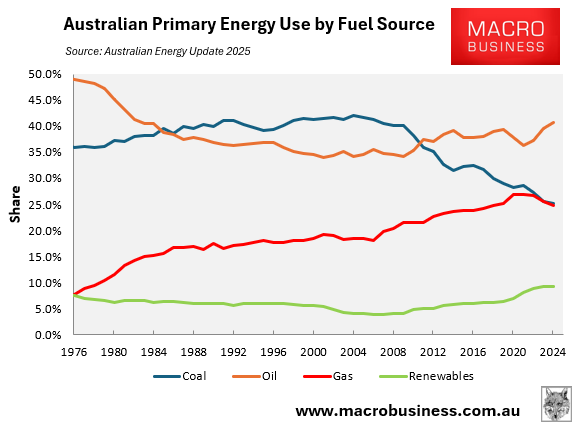

As illustrated below, oil accounted for the largest share (41%) of Australia’s primary energy use in 2024:

Given the lack of a reservation scheme across Eastern Australia, domestic gas prices are also likely to surge, placing upward pressure on electricity generation and fertiliser prices.

The upshot is that Australia faces a severe economic slowdown as the global energy shock rips across markets and economies.

I would not be surprised at all if the RBA responds similarly to the GFC and slashes rates to ward off recession.

Again, “History doesn’t repeat itself, but it often rhymes”.