Aussies cut expenditure, complicating interest rate outlook

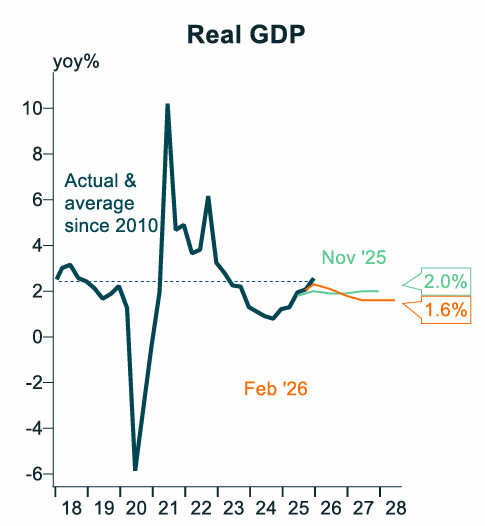

Wednesday’s December quarter national accounts release from the Australian Bureau of Statistics (ABS) came in hot, with GDP rising by 2.6% in 2025, above the RBA’s latest forecast in the February Statement of Monetary Policy (SoMP):

Chart by Alex Joiner (IFM Investors)

Viewed alongside the higher-than-target inflation and lower-than-forecast unemployment rate, the strong GDP print suggests that the RBA will be compelled to hike interest rates again, possibly at this month’s meeting.

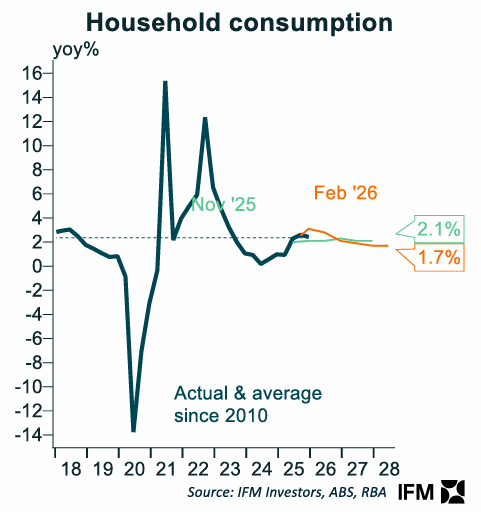

Chart by Alex Joiner (IFM Investors)

There is one significant ‘fly in the ointment’, however. Household consumption growth stalled in the December quarter, growing by only 0.3%, well below the RBA SoMP’s forecast of more than 1% growth over the quarter (RBA’s forecast presented below).

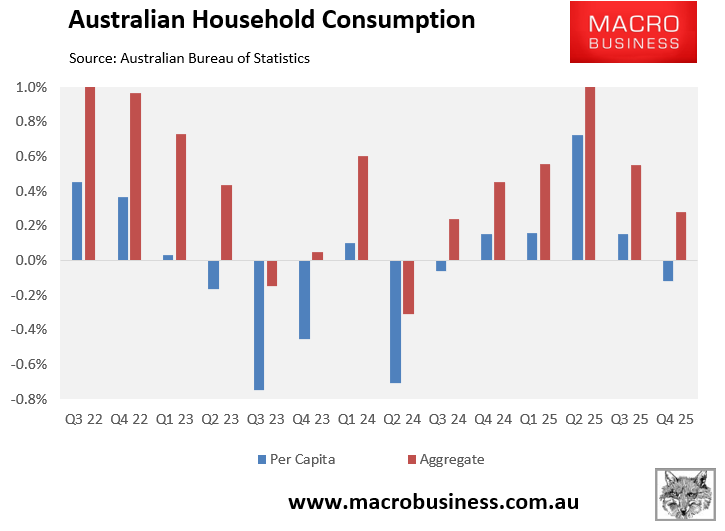

Chart by Alex Joiner (IFM Investors)

In fact, when adjusted for Australia’s 0.4% population growth over the quarter, real household consumption fell by 0.1% in per capita terms:

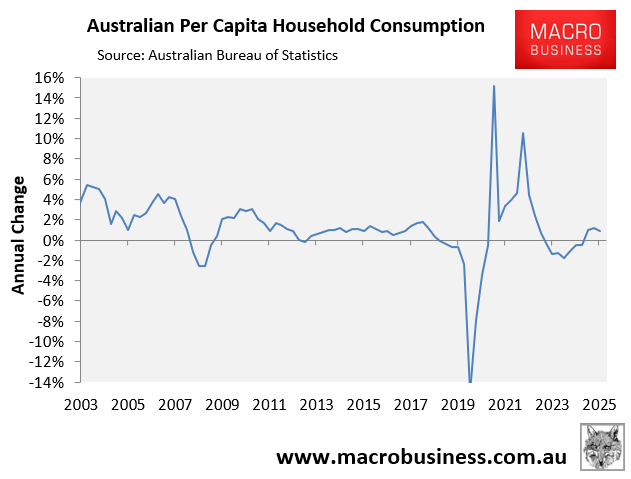

The annual growth in real per capita household consumption was also anaemic, tracking at only 0.9% annual growth in the December quarter of 2025, well below the RBA SoMP’s forecast of 1.6% growth:

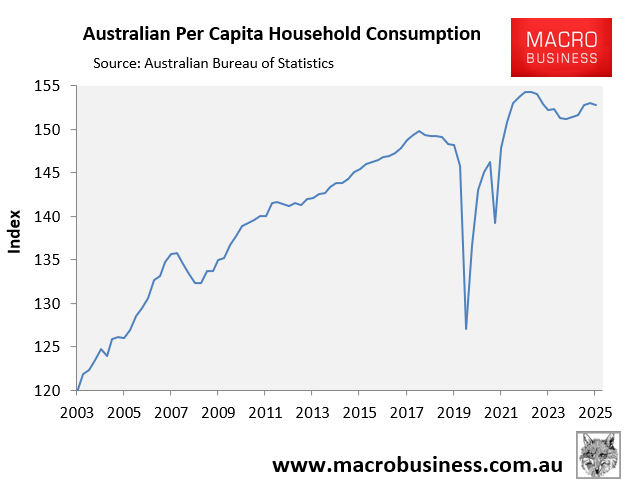

As illustrated below, real per capita household consumption remained 1.0% below its March 2023 peak:

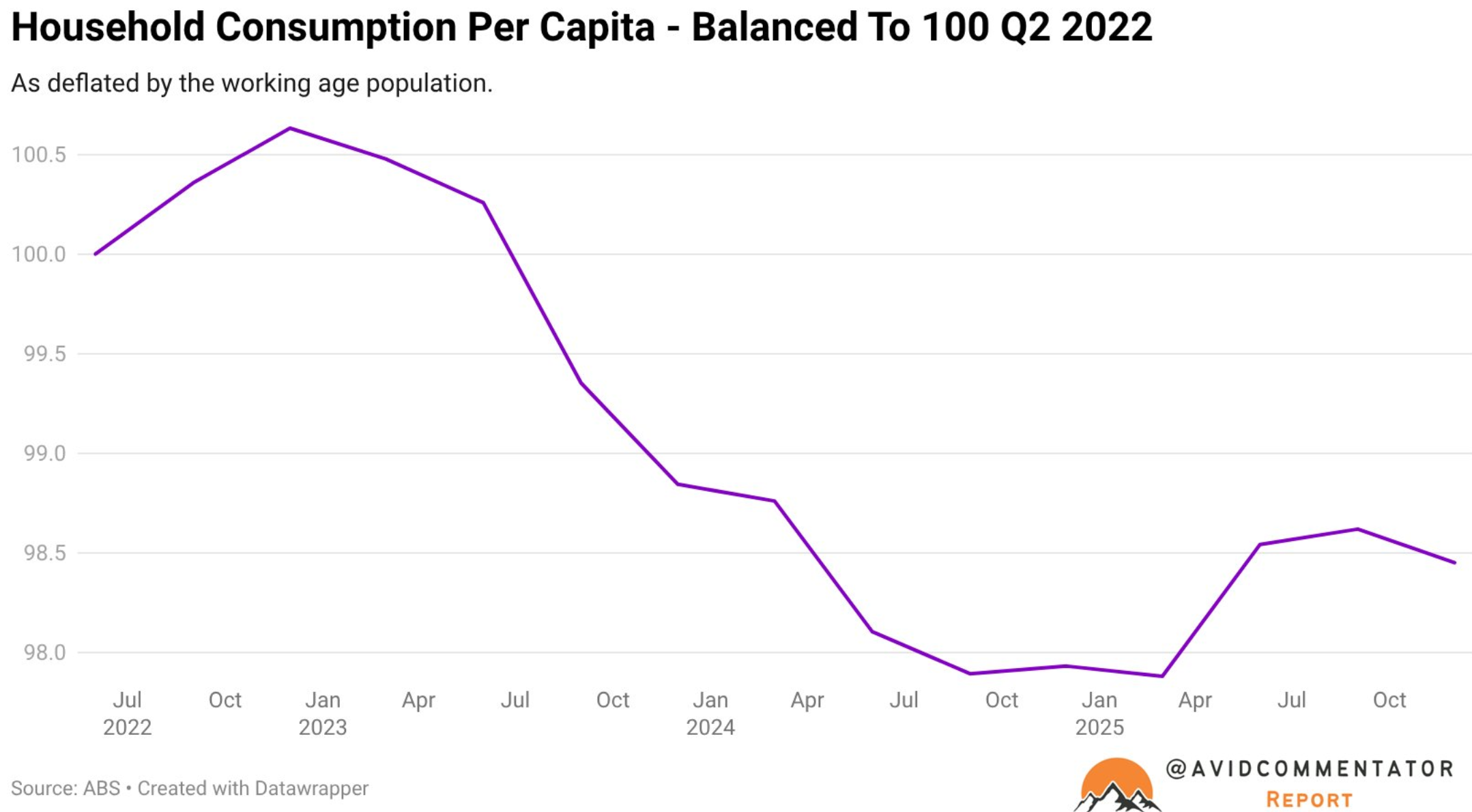

Tarric Brooker estimated that the decline in household spending is even sharper when tracked against the working-age population:

It could be that household spending has been impacted by changes in electricity spending due to rebates, which might have impacted growth rates over the year.

Even so, it is strange that we are talking about the RBA hiking interest rates when per capita household spending is so soft.