The Real Estate Institute of Australia (REIA) has attacked the proposed reduction in the capital gains tax (CGT) discount, arguing that:

- Reducing the CGT discount (from 50% to 25%) would push landlords to raise rents to compensate for lower after‑tax capital gains.

- The proposed reduction could potentially affect about 2.4 million renting households.

- In a tight rental market, landlords would likely pass on costs.

- Housing construction rates would also fall.

“If CGT incentives were removed, there is a high probability that property owners would seek to recover the lost capital gain incentives through increased rents, which would then be passed on to tenants in an already constrained rental market”, the REIA said in its submission to the inquiry.

“Any measure to reduce or eliminate the 50% CGT discount would see smaller volumes of new home building activity. This could mean having over 33,000 fewer new dwelling starts over five years, representing a contraction of the new supply of dwellings of up to 3.2%”.

“This would have severe impacts on housing affordability… A supply shortfall would further exacerbate rental inflation and push first home buyers out of the market”.

“Any policy changes that disincentivise investment could destabilise the market, leading to higher rents and reduced housing availability for renters”, the REIA submission warned.

The evidence does not support the REIA’s arguments:

The empirical evidence does not support the suggestion that a less generous CGT discount would harm new housing supply.

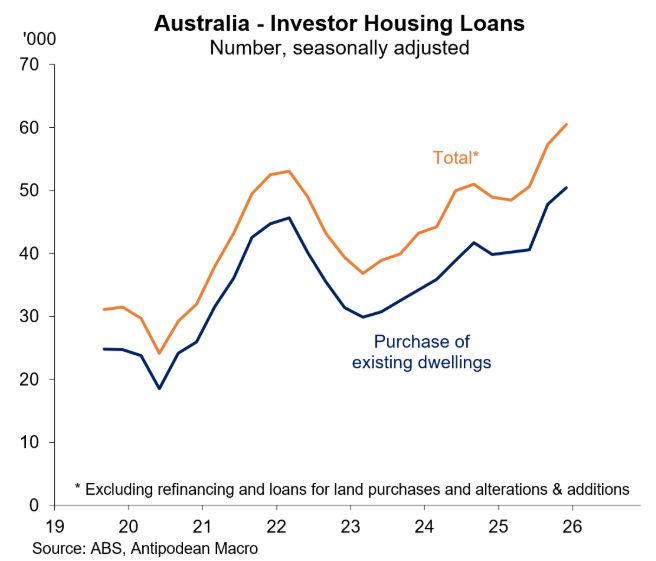

As illustrated below by Justin Fabo from Antipodean Macro, more than 80% of investor mortgage commitments are for established homes. Therefore, more than four out of five investors are not adding to housing supply:

Most investors, therefore, are simply turning homes for sale into homes for rent.

When an investor sells, the property does not vanish. Instead, it will either be purchased by another investor or by an owner-occupier (possibly a first-home buyer).

Therefore, if fewer investors participated in the market, or investors sold up following changes to the CGT discount, there would be fewer homes for rent, but also fewer people needing to rent because of more owner-occupiers.

The rental supply-demand balance would be largely unaffected.

Victoria proves the REIA wrong:

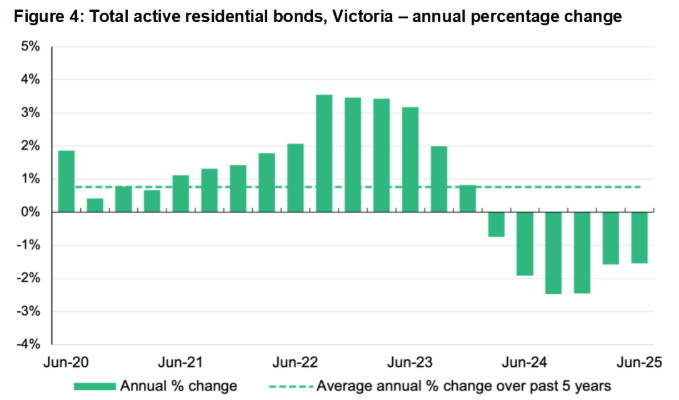

In 2024, the Victorian government significantly increased holding costs for investors—primarily through lower land‑tax thresholds, expanded vacant‑residential‑land taxes, and new short‑stay levies.

The changes mean more investors now pay land tax, and those who already pay are paying more, reducing net yields.

As a result, a significant number of investors abandoned the market, as evidenced by the decrease in rental bonds on issue:

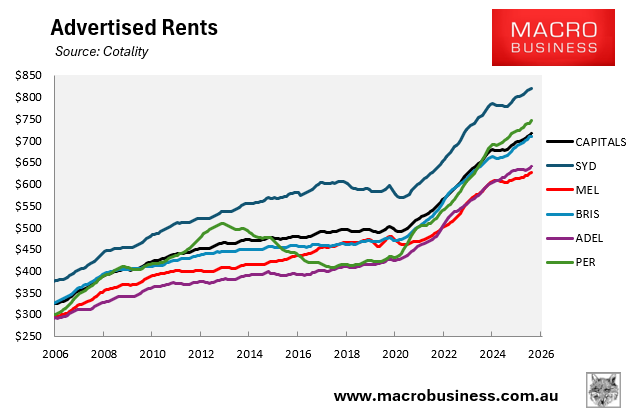

However, the exodus of investors has not driven up Melbourne rents or worsened affordability.

According to Cotality, Melbourne advertised rents grew by 36% in the five years to January 2026, significantly below the growth recorded across the other capital cities:

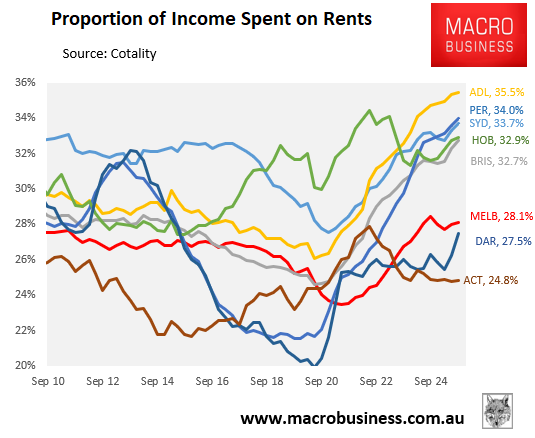

The amount of income required to rent the median home in Melbourne was 28.1% in Q3 2025, significantly below the other major capital cities and the national average of 33.4%:

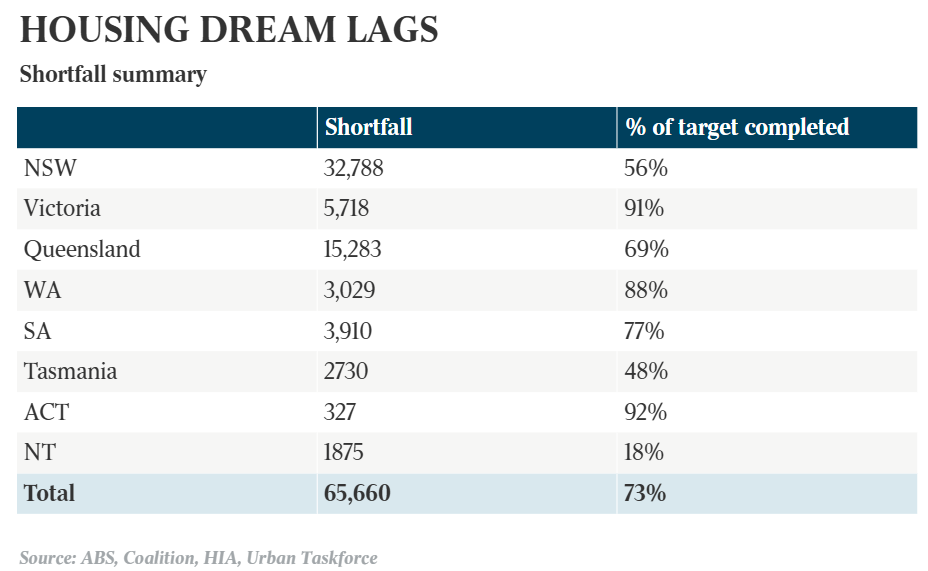

Victoria’s dwelling construction rate is also tracking well above the other states.

As illustrated below, Victoria is the only state to be tracking close to the National Housing Accord supply target:

The Takeaway:

The REIA’s scaremongering on the CGT discount doesn’t stand up to scrutiny.

The impact on housing supply and rental affordability would be minimal. In contrast, it would provide the federal government with additional revenue and make housing marginally more affordable for first-home buyers, thereby increasing the home-ownership rate.

Victoria’s experience also does not support concerns about an ‘investor strike’, given that it has the most affordable state rental market and has experienced stronger dwelling construction.