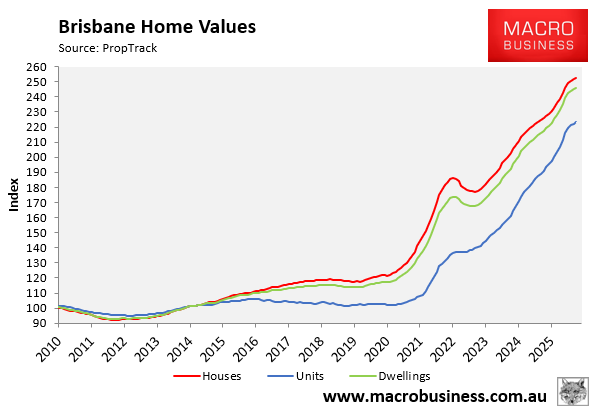

Brisbane’s housing market has experienced one of its largest-ever price booms over the past five years.

According to PropTrack, Brisbane dwelling values soared by 95.7% in the five years to January 2026:

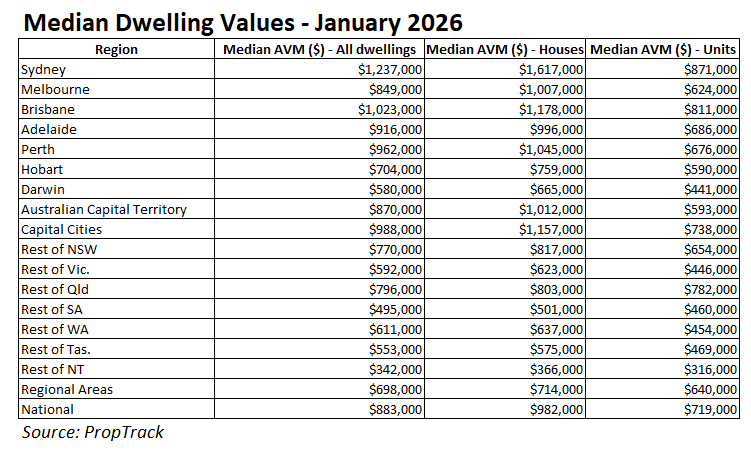

As a result, Brisbane has become the second most expensive housing market in the nation based on median values, behind Sydney:

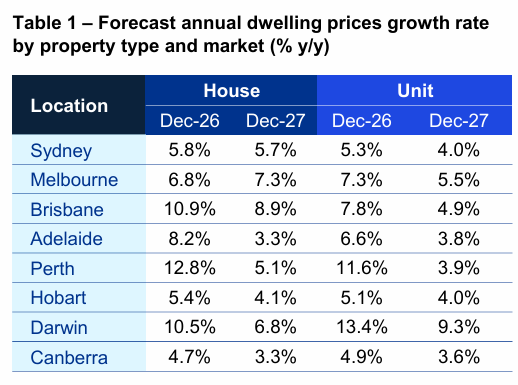

KPMG’s latest house price forecasts tip that Brisbane house prices will continue to record strong growth over 2026 and 2027:

Source: KPMG

According to KPMG, Brisbane house prices will rise by 10.9% in 2026 and by 8.9% in 2027. Using PropTrack’s figures, Brisbane’s median house price would increase to just over $1.4 million by the end of 2027 under these growth assumptions.

KPMG forecasts that Brisbane unit prices will rise by 7.8% in 2026 and by 4.9% in 2027, which would take the median Brisbane unit to more than $900,000 by the end of 2027.

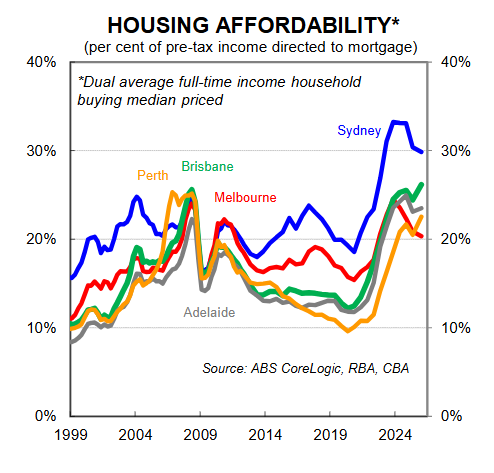

As illustrated below by CBA, mortgage repayment affordability in Brisbane is already tracking at its worst level in history, surpassing the GFC low:

With financial markets pricing in two 25 bps rate hikes this year, alongside strong projected house price growth, Brisbane mortgage affordability is set to worsen materially.

At some point, we will have to ask ourselves whether Brisbane housing is a bubble.

While historically low stock levels support current price growth, fundamentals will eventually reassert themselves.

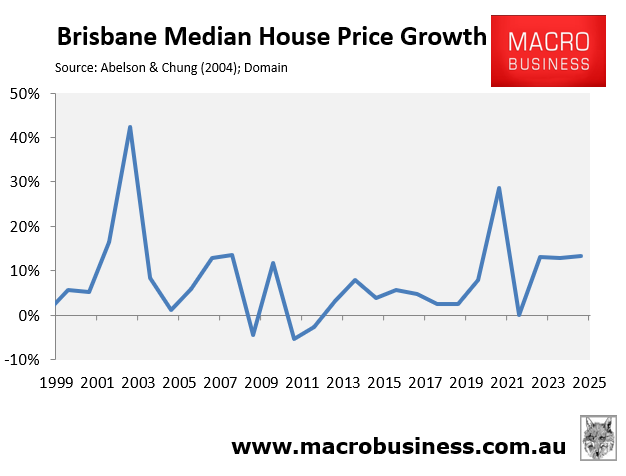

It is worth remembering that after the 2000s house price boom, Brisbane values posted barely any growth for nearly a decade:

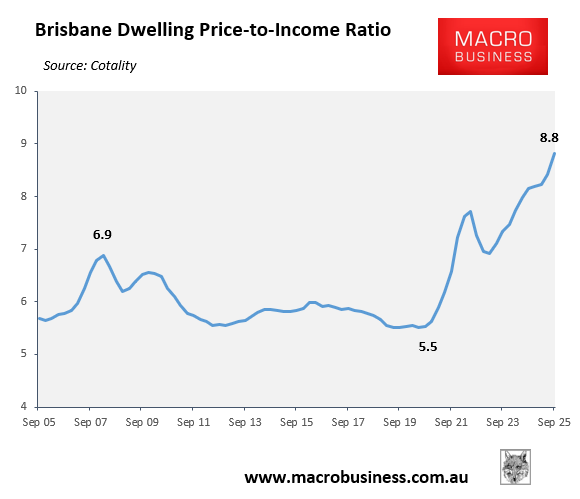

As a result, housing affordability in Brisbane improved both in mortgage serviceability terms (chart above) and relative to incomes (below).

A repeat of that event would be the benign scenario. The more destructive scenario would be a New Zealand- or Canadian-style price correction, in which values fall by around 15%.

Taking out a mega-mortgage and leveraging into Brisbane’s frothy market is undoubtedly a perilous proposition.