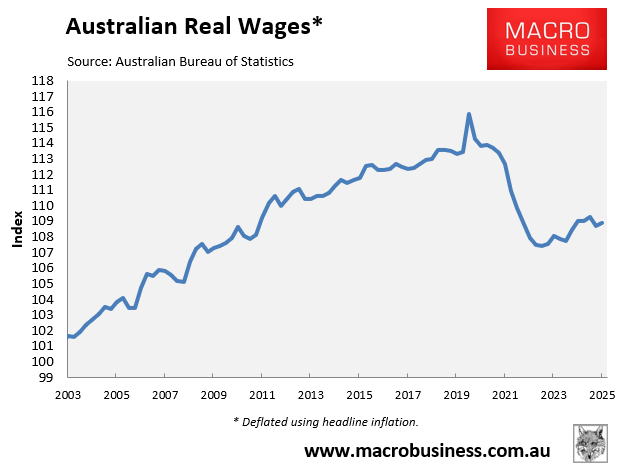

Last week, the Australian Bureau of Statistics (ABS) released wage data for the December quarter, which revealed that real inflation-adjusted wages fell by 0.3% in 2025, tracking at the same level as December 2011.

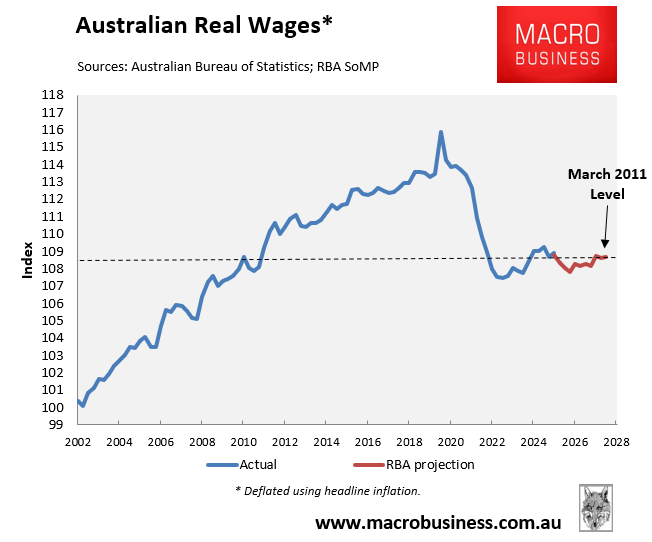

The Reserve Bank of Australia’s (RBA) latest Statement of Monetary Policy also projected that real wages won’t recover over its forecast horizon and will still be tracking at their late 2011 level in mid-2028.

Many readers are probably wondering why their material living standards aren’t improving following the pandemic inflation shock.

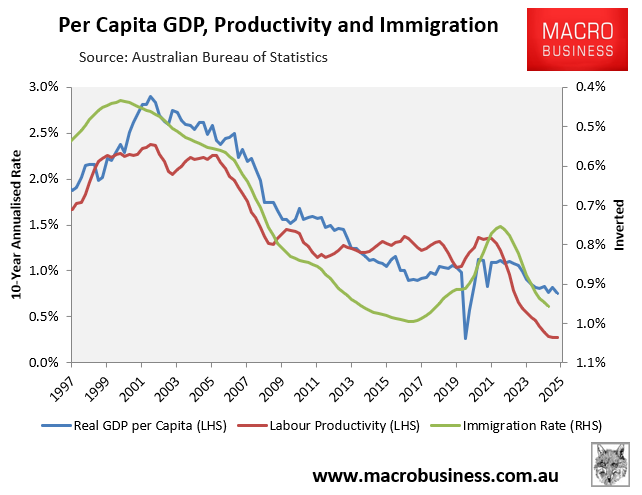

The main reason comes down to Australia’s poor productivity growth.

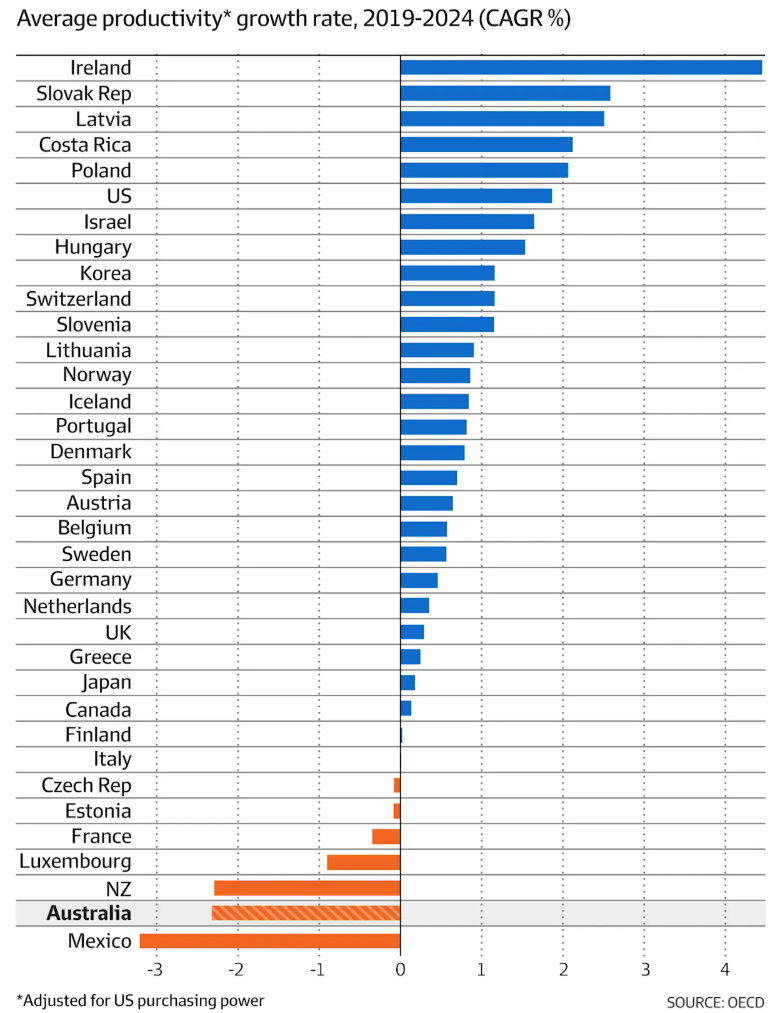

Australia’s productivity growth has fallen sharply over the past 20 years and since the pandemic has ranked amongst the poorest in the OECD.

Chart from The AFR

Without strong productivity growth, the economy’s speed limit has been lowered to a snail’s pace and cannot grow in per capita terms because it will continue to push up against capacity constraints.

With low productivity growth, every time demand rises, say due to excessive government spending (as we are experiencing currently), inflation will rise, resulting in higher interest rates (as overall demand outpaces supply).

Australia’s poor productivity growth has been driven by three primary factors.

First, due to high immigration, the nation’s population has grown significantly faster over the past 20 years than the growth in business, infrastructure, and housing investment.

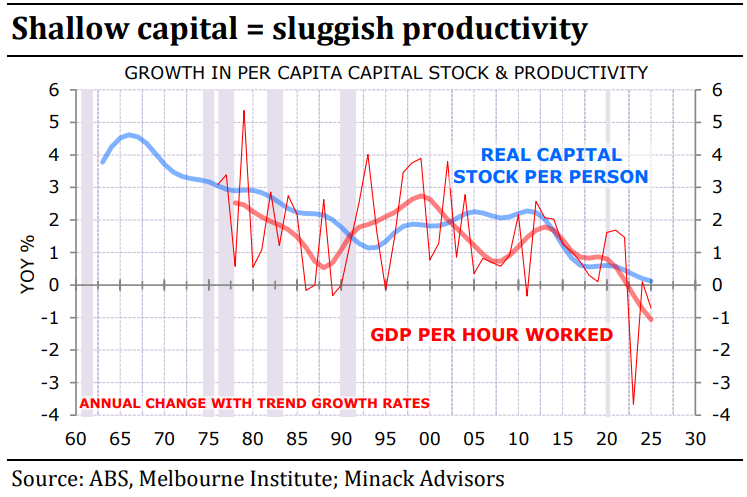

Chart from Gerard Minack (Minack Advisors)

As a result, Australia’s capital base—think infrastructure, tools and machinery, and technology—has been spread more thinly across more people. This has increased congestion in infrastructure, slowed output per worker, and helped to drive up inflation (e.g., via rents).

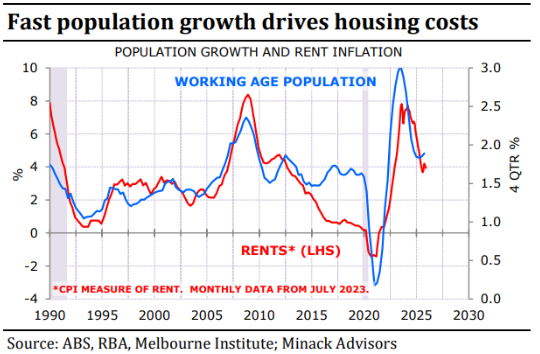

Chart from Gerard Minack (Minack Advisors)

Second, Australia has experienced a rapid expansion of non-market (government-funded) jobs, related mostly to the expansion of the NDIS.

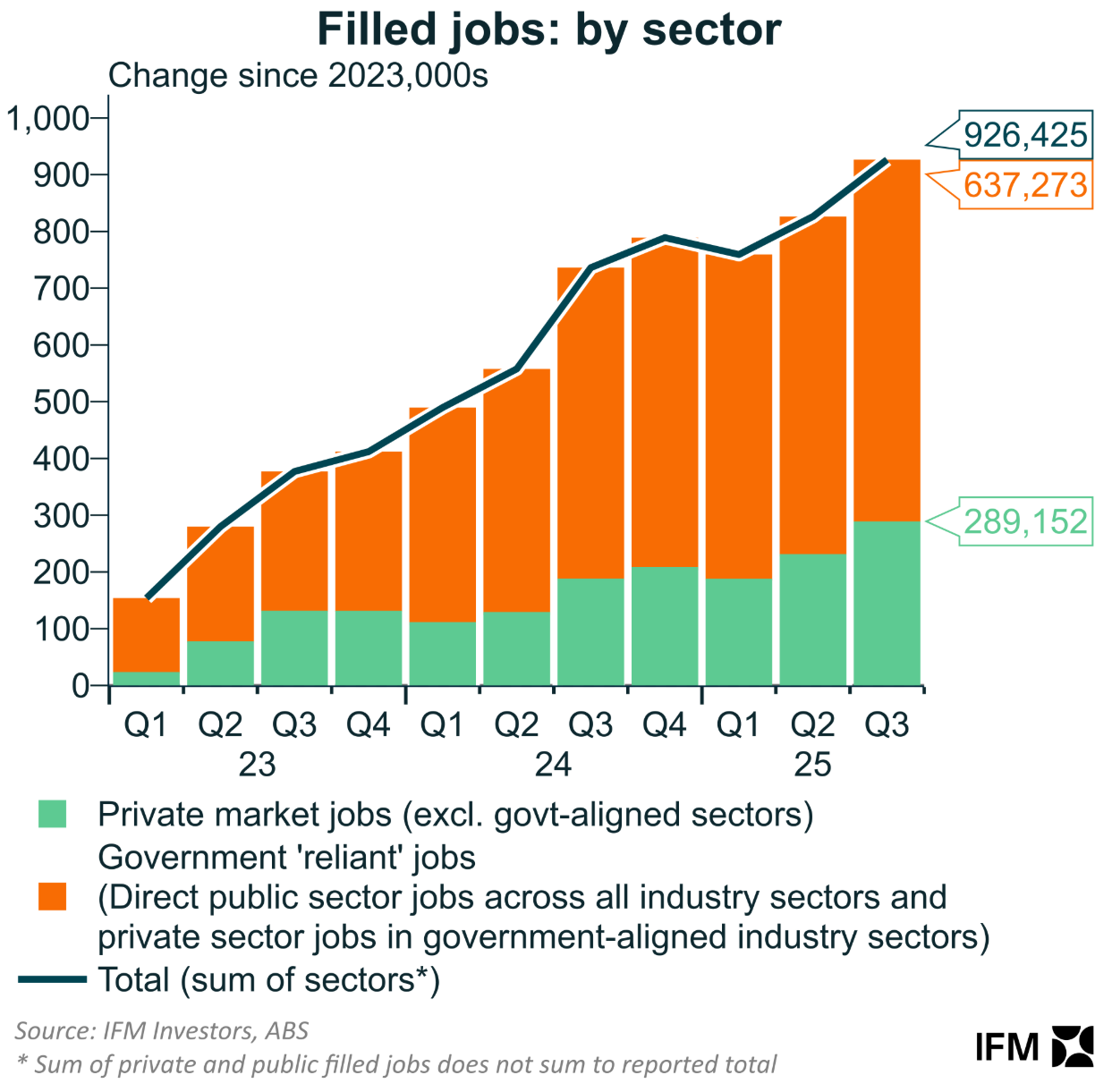

Chart from Alex Joiner (IFM Investors)

Most of Australia’s job growth since the pandemic has been in the non-market sector.

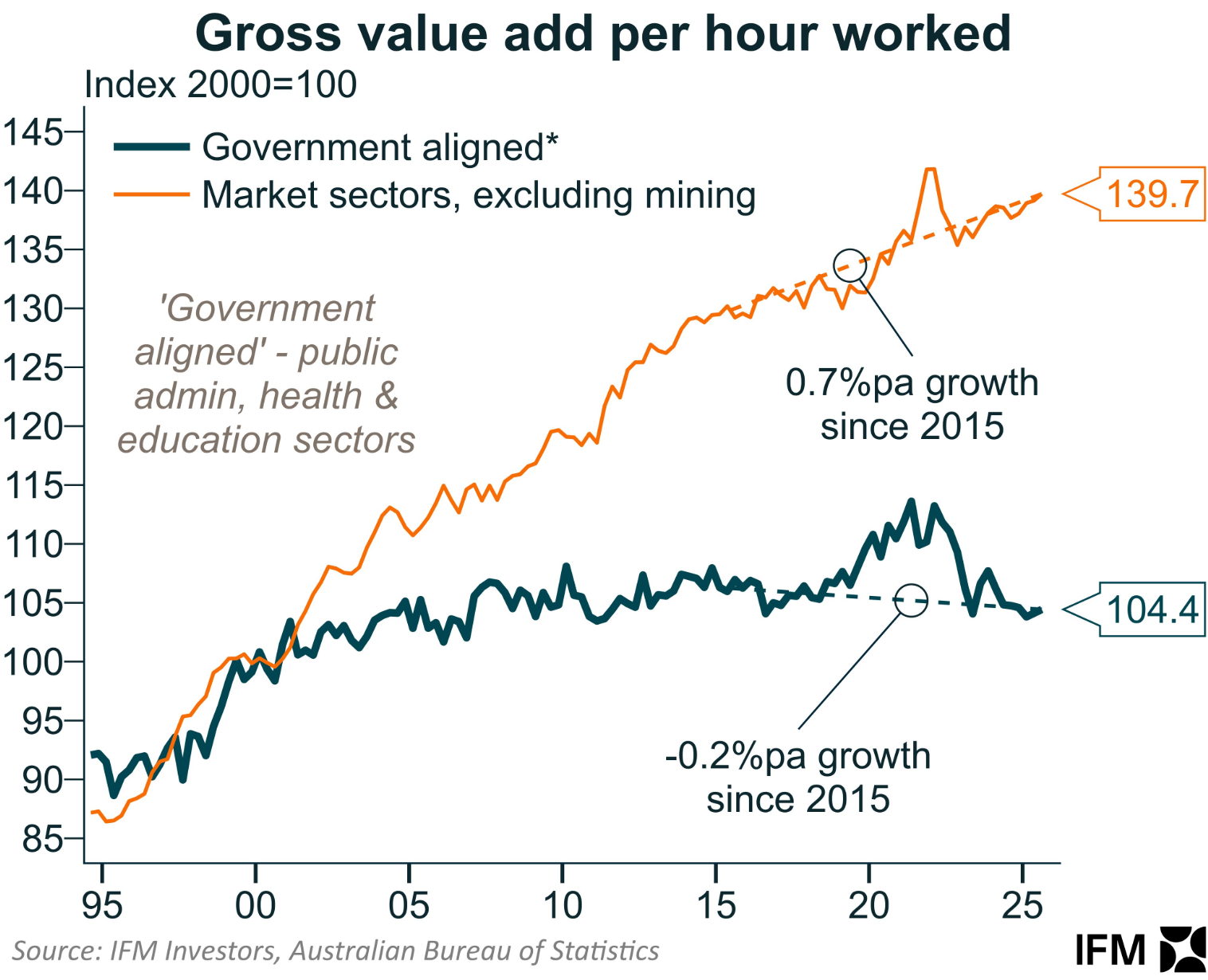

Productivity in the non-market economy has fallen sharply and is tracking at around the same level as 20 years ago, which has dragged down overall productivity.

Chart from Alex Joiner (IFM Investors)

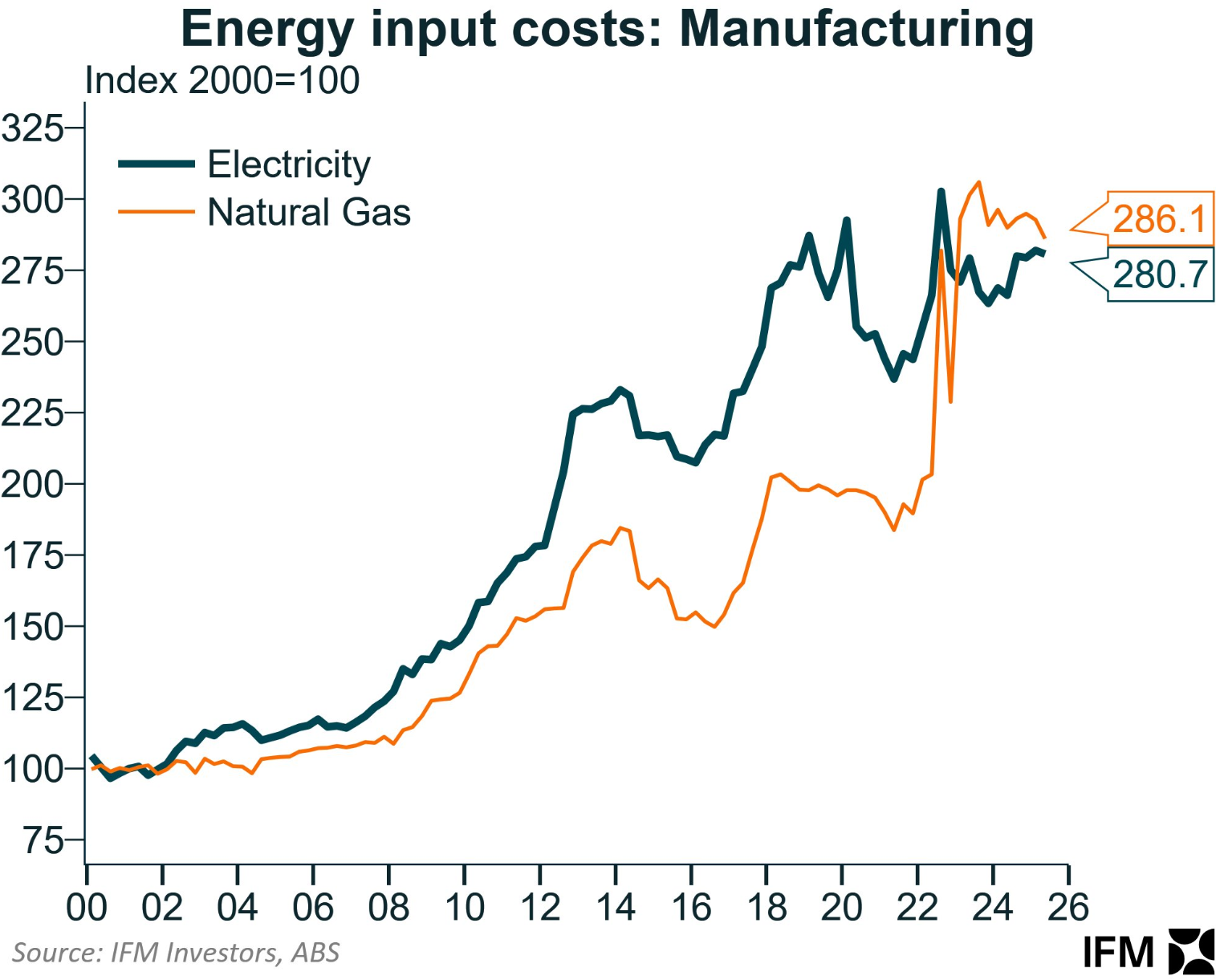

Third, soaring energy costs have eroded Australia’s productivity growth.

Energy turns labour and capital into useful work, and our GDP and living standards depend on it. Rising energy costs have added costs across Australia’s entire supply chain.

Chart from Alex Joiner (IFM Investors)

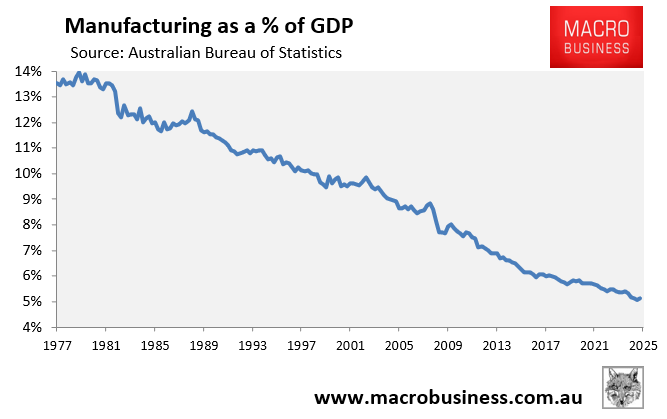

Rising energy costs have also shuttered many manufacturers and caused deindustrialisation.

Manufacturing has traditionally been a driver of Australia’s productivity growth, and its shrinkage has lowered overall productivity.

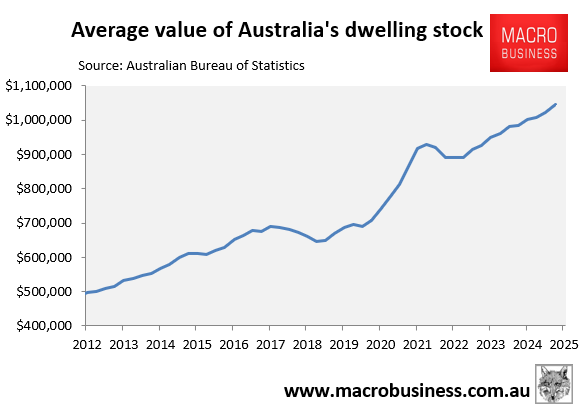

Fourth, Australia’s productivity has suffered from an increasing share of our economic output being channelled into non-productive housing, fuelled in part by generous tax concessions that incentivise investment in established homes rather than the real economy:

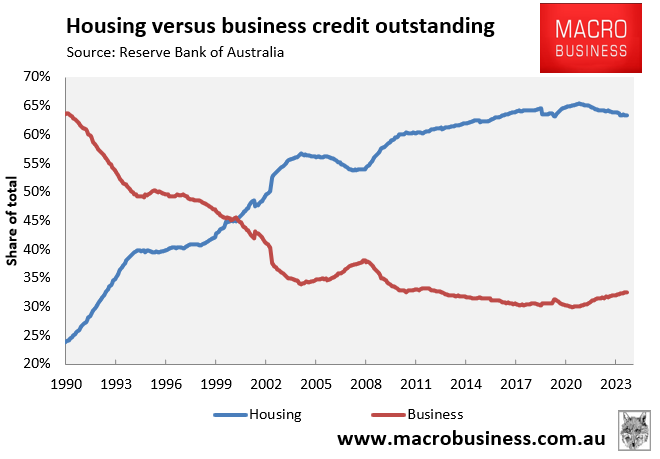

Australia’s banking system has also transformed into giant mortgage lenders, starving businesses of credit:

The Takeaway:

Australian real wages and living standards won’t improve unless the nation’s productivity growth improves.

The solution requires four main reforms from governments:

- Lower and better targeted immigration, to prevent capital dilution. We can’t keep growing demand faster than the economy’s absorptive capacity. We also need an immigration system that imports genuinely highly skilled people in areas of shortage, rather than more Uber drivers.

- Cutting back wasteful government spending and ensuring that when governments spend our money, they get the biggest ‘bang for the buck’.

- Delivering stable and affordable energy via genuine gas reservation and abandoning the push to an all-renewables energy future.

- Tax reforms to encourage productive investment over speculative housing investment.

I discussed these issues in my weekend Treasury of Common Sense at Radio 2GB/4BC.