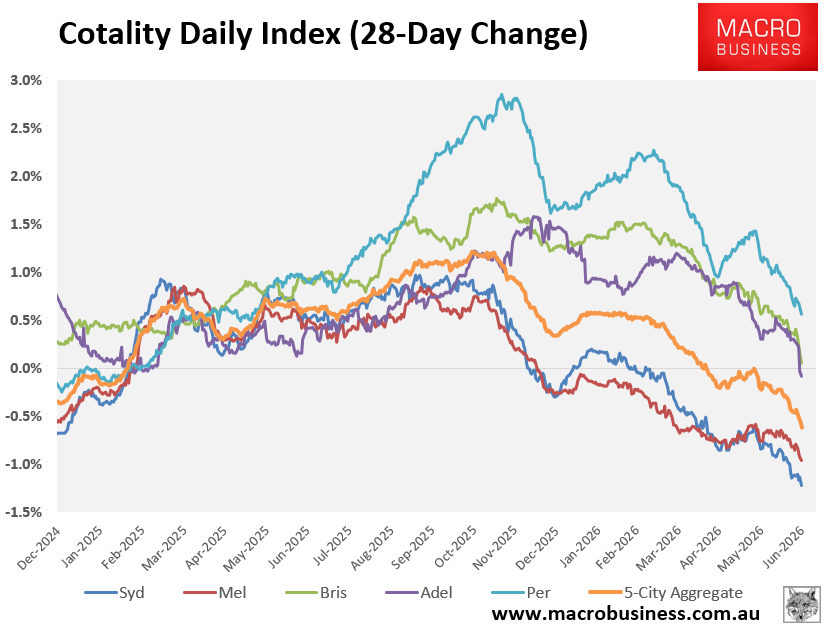

As the path for housing price growth continues to deteriorate, with more cities slowly joining Melbourne and Sydney in the falling housing prices club, concerns are building on the potential impact on the economy.

In the latest RBA Board Minutes they noted:

“Conditions in the established housing market had softened and housing credit growth looked set to slow in the period ahead. This reflected the pass-through of monetary policy tightening and, more recently, tax changes for housing investors announced in the Australian Government budget.”

“Members also noted the risks associated with a potentially material weakening in housing markets, including if this were to inhibit growth in consumption.”

This may be a significant issue in the future if the RBA’s previous conclusion about the impact of the housing market on the broader economy is correct.

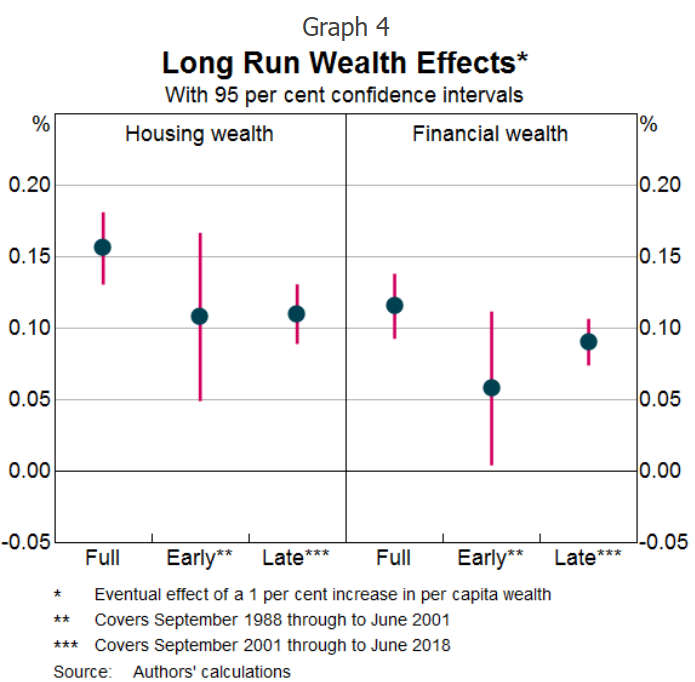

In a 2019 RBA paper entitled, ‘ Wealth and Consumption’, concluded that:

“a one per cent increase in the value of housing wealth will lead to a 0.16 per cent increase in the long-run level of consumption, while a one per cent increase in stock market wealth will raise consumption by 0.12 per cent”.

Now, amidst falling housing prices, that expected boost to consumption is not only being removed but reversed entirely.

While a “wealth effect” of higher asset prices is more or less an established policy setting for central banks across the developed world, Australia is somewhat unique in how rising asset prices feed into the economy.

Back in 2021, the Australian Financial Review reported that:

“Home-owners are using rising property values and increased equity to top up their mortgages, by nearly $93 billion in the last year, spending up on renovations, cars, and real-estate investments, or to prop up struggling small businesses.”

In short, rising housing prices motivate and facilitate Australians pulling billions of dollars every month out of their homes to do with what they will.

The Takeaway

It has been said that in Australia “housing is the economy” and there is evidence from metrics such as retail sales from during periods of housing price falls that supports this argument.

That being said, building an economy on a strategy reliant on ever higher housing prices was never going to be viable forever, in the same way that it wasn’t for the U.S. during its era of housing excess and home equity withdrawals.

As things stand today, it appears likely that housing price weakness will continue to spread and persist until a positive catalyst evolves.

Historically that has often come from the Reserve Bank or the federal government, but with underlying inflation uncomfortably high and the government already running several major policies that support the market, such as high migration, shared equity and the 5% deposit scheme, it may need to come from somewhere else.

Ultimately, the RBA is right to be concerned, but at the same time the adjustment that may occur is a much-needed one as the economy attempts to kick its addiction to high housing prices.