In the months prior to the recent federal budget, data suggested that mortgage demand was beginning to trend downward.

Against a backdrop of deeply depressed consumer confidence and falling per capita real consumer spending, it was arguably an entirely expected set of circumstances.

When assessing mortgage demand through the lens of the Reserve Bank’s credit aggregates data, it’s clear that at least up until the end of May demand for mortgage credit from property investors appeared to remain robust.

On the other hand, growth rates for outstanding owner-occupier mortgage debt stagnated in recent months.

Following the announcement that negative gearing would be grandfathered out for existing homes and the 50% capital gains tax discount would be removed for newly purchased assets, the outlook began to change significantly.

According to recent figures from Macquarie Bank analyst Victor German provided to the Australian, demand for new investor loans has declined by up to 50%, with overall new lending flows for household mortgages down by 20% to 30% in year on year terms.

German concludes that owner-occupiers have also been impacted, but the drop in their demand for new loans is significantly smaller, at 10% to 20% year on year.

“This compares with Westpac’s application volumes tracking down 20 per cent year on year and NAB application values down about 15 per cent quarter on quarter.” German stated.

Shifting the focus to the housing market, the time a home remains on the market has begun to surge across much of the country, with Brisbane and Perth in particular showing dramatic increases.

In terms of prices, growth has moderated dramatically across most of the nation, particularly in smaller capitals that were seeing robust price growth not long ago.

In Sydney and Melbourne, the existing downtrend in price growth seen throughout much of this year has intensified.

There is further downside risk, with the market still heavily supported by long-lived but ultimately temporary factors.

For example, in per-capita terms (working-age population), the number of properties on the market for sale is roughly half of what it was in 2019.

If we were to see this very belatedly begin to normalize over the coming months and years, the likelihood of greater downside for the market grows significantly.

The Takeaway

As prices continue to fall across an increasingly large proportion of the country, it’s worth reflecting on how much the market has been supported by these temporary factors.

Eventually, listing volumes were going to make a push back towards pre-pandemic norms, and the impact of this highly unsung factor supporting higher housing prices would draw to a close.

The number of first-home buyers the government could potentially coax into the market is also finite.

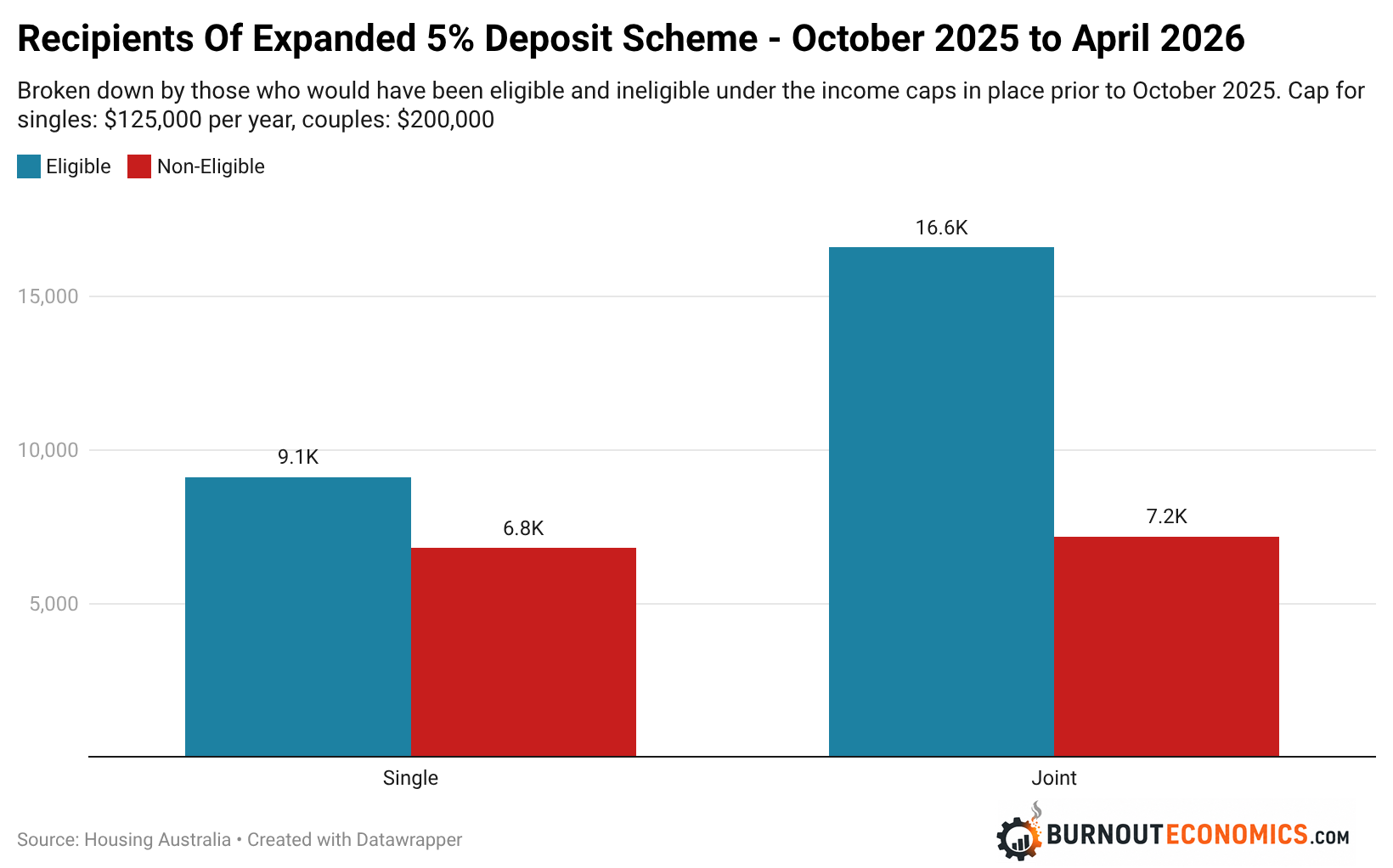

With the expansion of the Albanese government’s 5% deposit scheme driving only a 3% increase in first home buyer activity on a 6 month rolling basis, according to an analysis by The Guardian.

As the chart below from my Burnout Economics.com article on the impact of the scheme illustrates, first home buyer numbers are being heavily supported by a cohort who simply wouldn’t have qualified less than a year ago, due to having too high of an income.

When looking at some of the commentary on social media regarding the future of the housing market, much of it now rests on the continued high levels of migration.

The theory is that the Albanese government will keep the rate of immigration far too high, and that this approach will ensure the rental crisis continues, thereby supporting demand from property investors and, by extension, home prices.

While that view is built on a deeply troubling outlook for Australia’s future, the expectation from analysis in both the public and private sectors is that this is indeed the base case.

The risk for housing prices going forward is that this does not to come pass, that for whatever reason the Albanese government is forced to follow its Anglosphere peers in cutting migration back to more sustainable levels.

If that were to come to pass, a much greater downside for the housing market would become significantly more likely.