OK, so where Korea goes, goes AI. TME with more.

Memory Cracks

The technical deterioration across the AI memory complex is becoming difficult to dismiss as stock-specific. From SK Hynix and SanDisk to Micron, Kioxia and Samsung, momentum is fading at the same time, with several leaders breaking key trendlines and short-term support. Whether this is simply a healthy reset or the beginning of a broader unwind, the synchronized nature of the weakness deserves attention.

SNDK

SNDK has fallen roughly 22% from the all-time high reached just a few sessions ago. The stock is now breaking below both the steep uptrend and the 21-day moving average. The next major support comes in around the much lower 50-day moving average near $1,600.

Momentum has deteriorated rapidly, with RSI now at its most oversold level since late March.

Source: LSEG Workspace

KIOXIA

Momentum snapped overnight. The stock decisively broke below both the steep trendline and the 21-day moving average. The 50-day moving average remains well below current prices, while RSI has reached deeply oversold levels in just a matter of sessions.

Source: LSEG Workspace

MU

MU has broken below the steep trendline and the 21-day moving average. RSI has become heavily oversold almost overnight, although the next major technical reference, the 50-day moving average, still sits considerably lower.

MU never reached the euphoric extremes seen in SNDK or Kioxia, making today’s breakdown notable despite the stock entering it from a far less stretched starting point.

Source: LSEG Workspace

SK Hynix

Momentum has deteriorated rapidly for the poster child of the Asian AI mania. The stock has broken below both the steep trendline and the 21-day moving average, while RSI has become deeply oversold. The next meaningful technical support is the much lower 50-day moving average.

Source: LSEG Workspace

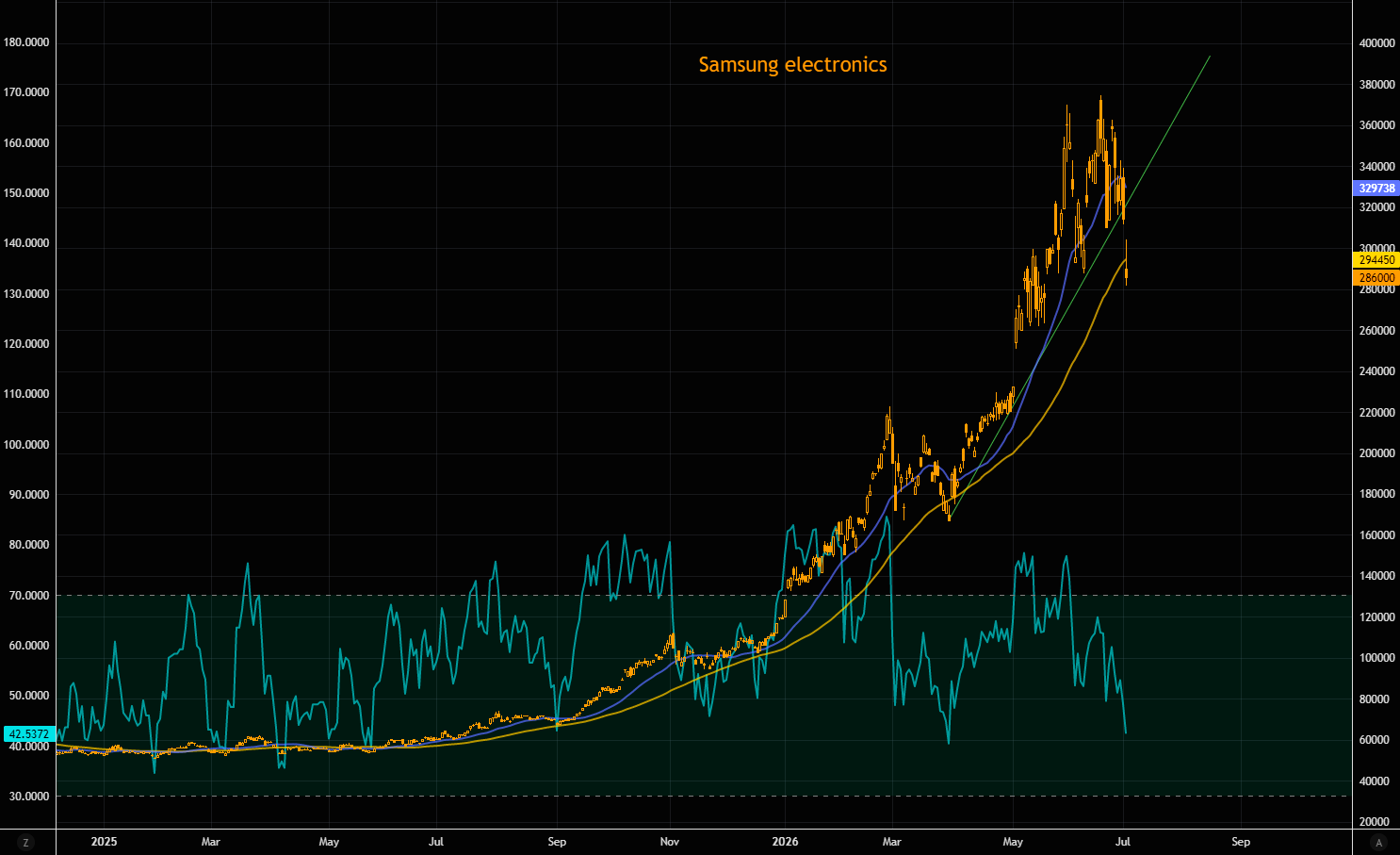

Samsung

The stock broke below the 21-day moving average yesterday and followed through today by taking out both the short-term trendline and the 50-day moving average. Unlike many AI peers, it never went truly parabolic, but momentum has clearly deteriorated. RSI is now at its most oversold level in months.

When even the laggards begin to crack, it’s becoming increasingly difficult to argue that the weakness is stock-specific.

Source: LSEG Workspace

Memory

For some perspective: the above mentioned names and performance YTD (in %).

Source: LSEG Workspace

China’s memory moment

Apple is reportedly considering Chinese memory suppliers for products sold domestically. The immediate benefit is obvious: lower costs and greater supply flexibility. The bigger story is what it signals. If Apple embraces Chinese memory suppliers, it does more than lower costs; it validates domestic competitors and could gradually reshape competitive dynamics in the world’s largest electronics market.

All bubbles are feedback loops, and this one is no different.

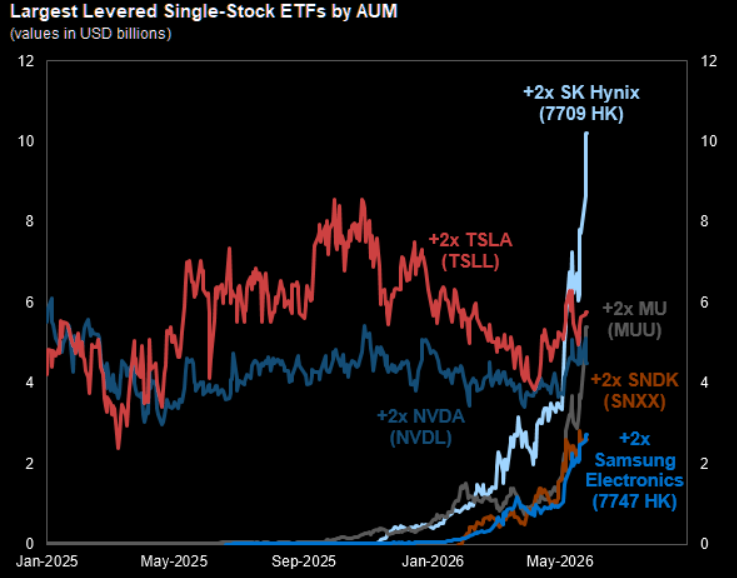

King of leverage

Goldman highlighted one of the clearest signs of AI euphoria last month: the 2x leveraged SK Hynix ETF had grown into the world’s largest single-stock leveraged ETF by a considerable margin. When one of the market’s most crowded trades is also one of its most leveraged, volatility has a habit of feeding on itself.

Source: GS

Learning leverage lessons

The biggest casualties aren’t necessarily SK Hynix shareholders, they’re the retail investors who chased the move through 2x leveraged ETFs. Despite the stock remaining well above its June lows, the combination of leverage and extreme volatility has inflicted devastating losses.

Investors who bought near the peak now require a gain north of 70% just to get back to flat. That’s the cruel arithmetic of leverage, and a painful reminder that parabolic trades rarely end gently.

Source: LSEG Workspace

The slippage trap

The slippage comes from daily rebalancing. Leveraged ETFs target a multiple of daily returns, not long-term returns. As a result, volatile back-and-forth price action gradually erodes performance through compounding effects, meaning a leveraged ETF can remain well below its highs even when the underlying index has fully recovered. Few understand this.

Source: TME

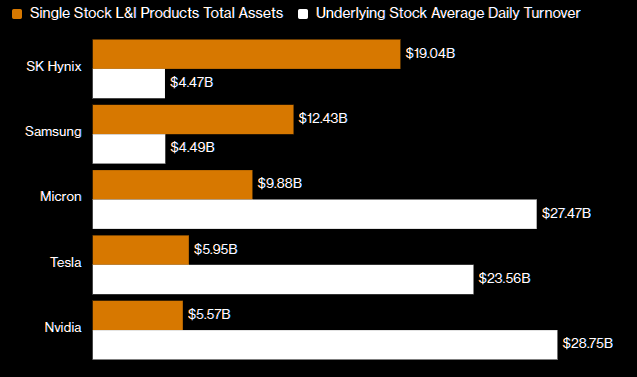

Leverage over the underlying

Korea’s tech stars stand out for outsized leveraged ETFs relative to daily trading volume, increasing the potential for ETF flows to amplify moves in the underlying stocks.

Source: Bloomberg

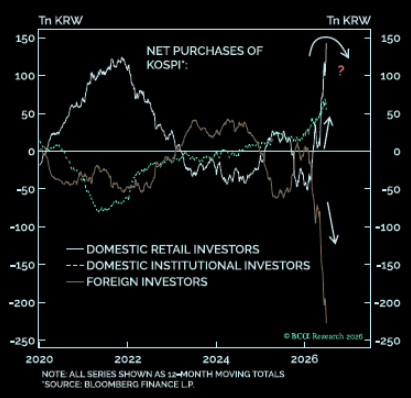

The buyer of last resort

Every bubble eventually reaches the point where retail has to keep buying because everyone else already has. BCA’s Budaghyan argues Korea may be approaching that stage. Foreign capital has been leaving even as the Kospi pushed to new highs, making the market increasingly reliant on the optimism of domestic retail investors.

Source: BCA/Authers

Theta bites

The KOSPI has spent months in an extreme spot-up, vol-up regime, but those conditions rarely last forever. With the KOSPI VIX flirting with 100 just days ago, upside exposure became extraordinarily expensive. Once the market stops going straight up, theta takes over. Premiums collapse, late call buyers head for the exits and the resulting unwind risks feeding directly back into the underlying market through dealer hedging and broader de-risking.

Source: LSEG Workspace

The combination of leverage, expensive options and retail dominance helped fuel one of Asia’s most spectacular AI rallies. If those forces now begin reinforcing each other in reverse, the unwind could prove just as powerful as the advance.

Touche. There’s suddenly a lot going wrong with Meta pulling the pin on capex, Korea coming apart, Palantir at war with partners over business models and overcharging and the Warsh test underway in the backgrond. Bubbles don’t die of old age.

That said, if DXY reverses, expect another leg up.