Since the Albanese government returned to power last year, Treasurer Jim Chalmers and other senior government members have focused on productivity.

Perhaps the most notable example of this was the Albanese government’s ‘Productivity Summit’ or ‘Productivity Roundtable’ in August last year.

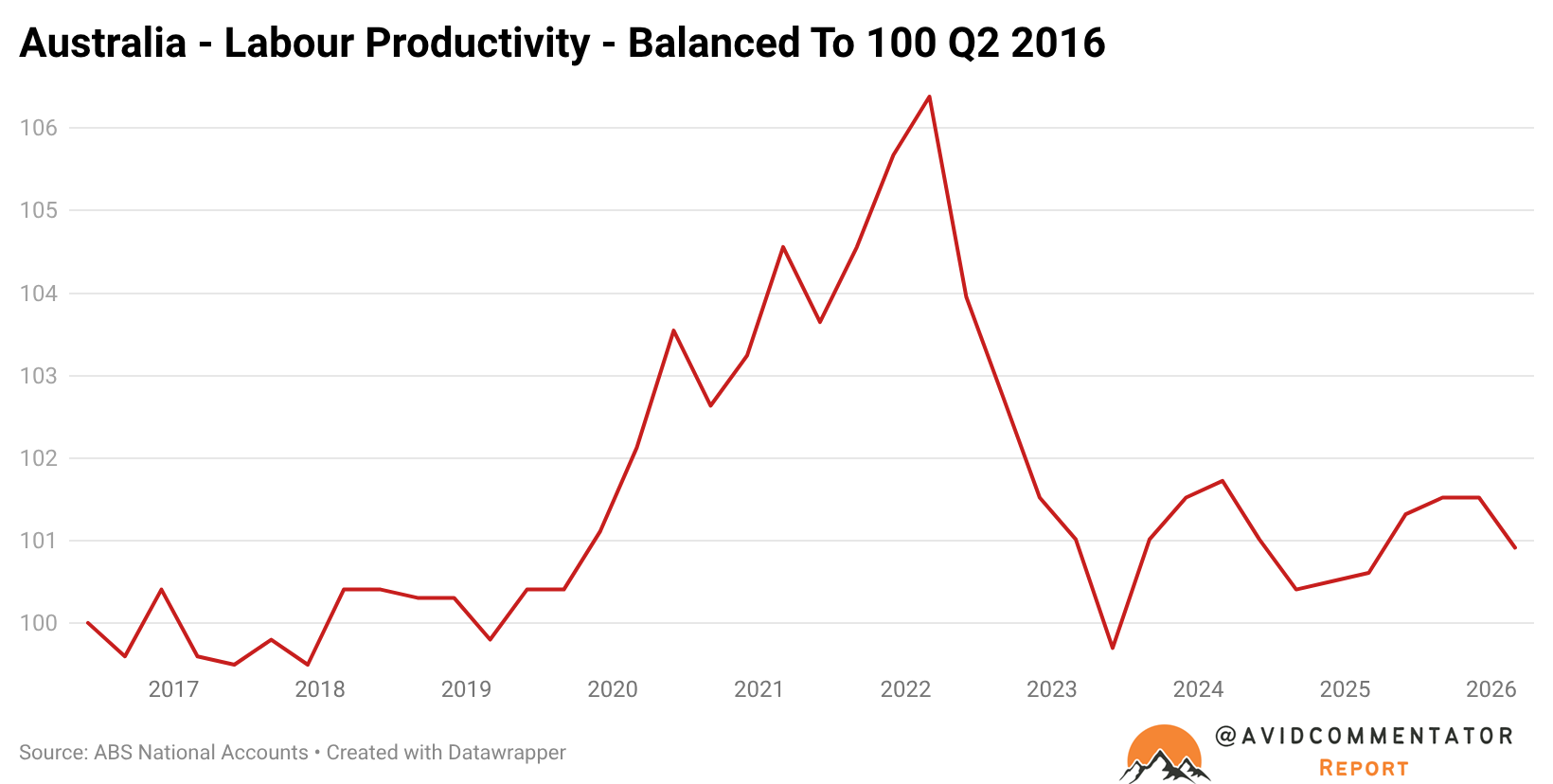

Since then, the weak productivity growth that has defined much of the last 15 years has continued, with labour productivity falling by 0.6% in the latest national accounts figures through to the end of the March quarter.

At the recent Morgan Stanley summit, Treasurer Jim Chalmers made the claim that the governments proposed changes to negative gearing and the capital gains tax discount would be “good for productivity”.

Chalmers made the case that making investment in existing homes less attractive would boost investment into more productive sectors.

“This speaks to the challenge we must confront in our economy: a tax system that funnels investment into established housing at the expense of other important parts of our economy”, Chalmers said

At face value this is a very worthy goal, it’s certainly true that the economy has lacked robust business investment for a long time and that existing housing is sucking in capital away from more productive uses.

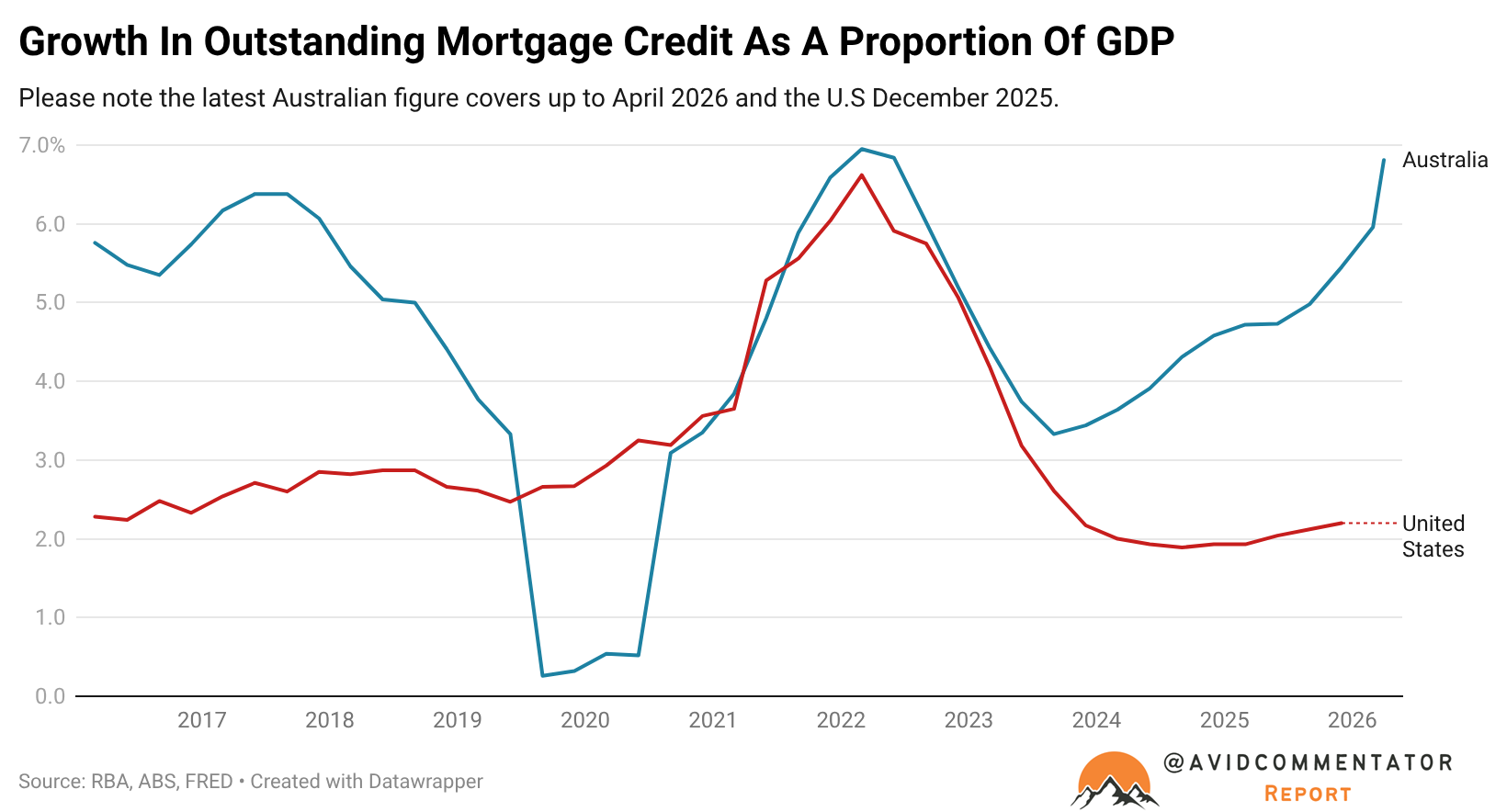

Looking at net mortgage issuance as a proportion of GDP over the last decade in the United States and Australia, it’s clear how reliant the Aussie economy is on housing.

If the governments changes to negative gearing and the capital gains tax discount were solely focused on existing residential property, then Chalmers’ argument that they would benefit productivity would be on fairly solid ground.

More capital would be devoted to shares, new home builds, businesses and other assets.

But because the changes target shares, businesses and other assets, the argument becomes much more challenging to make.

The Treasury estimates that despite the benefit of negative gearing being retained on new builds, 35,000 fewer homes will be built over the next decade compared with no changes being made.

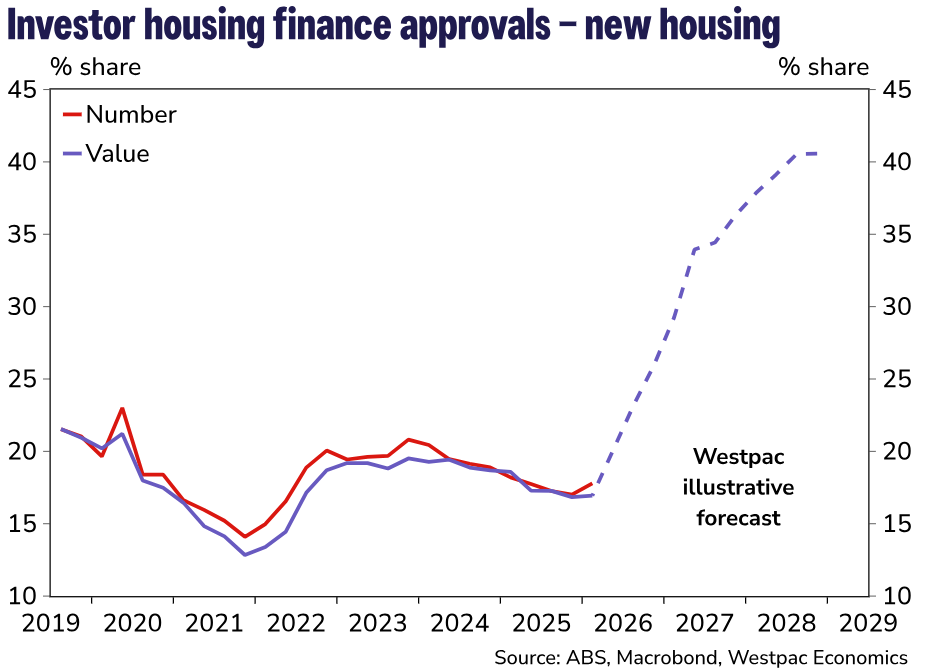

While others, such as Westpac, have made a case that investor-driven home construction will surge, even as broader investor activity falls dramatically, that is not the view of Treasury.

On balance we are left with a set of circumstances where investment into productivity-enhancing assets is less attractive than what it was prior to the federal budget, both in terms

While the Albanese government continues to insist that its changes will enhance productivity and improve the quality of economic growth, it is increasingly isolated, as concerns over the future of business and personal investment continue to mount.

Ultimately, it appears unlikely that productivity growth will accelerate from here, as long-standing structural issues and government policy choices combine to create an environment unfavourable for a return to robust levels of business investment as a proportion of GDP.