When the Reserve Bank met last Tuesday to hand down its latest monetary policy decision, a 0.25% rise to 4.35%, it also came with a new set of forecasts from the RBA’s latest Statement on Monetary Policy (SOMP).

While it held downgrades to the forecast rate of economic growth and higher inflation forecasts than the previous iteration, overall it wasn’t nearly as bad as some of the commentary from other central banks, such as the Bank of England, would suggest the outlook may be.

Source: Bank Of England

Meanwhile, back at Martin Place in Sydney, the RBA’s baseline outlook is relatively optimistic, all things considered.

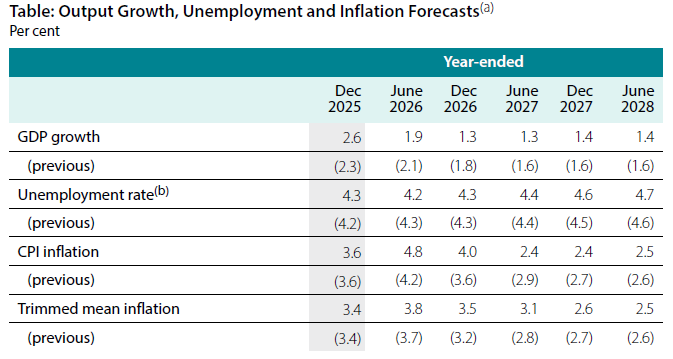

The largest revision to annual GDP growth was a downward move of 0.5%, expected in the year to December 2026.

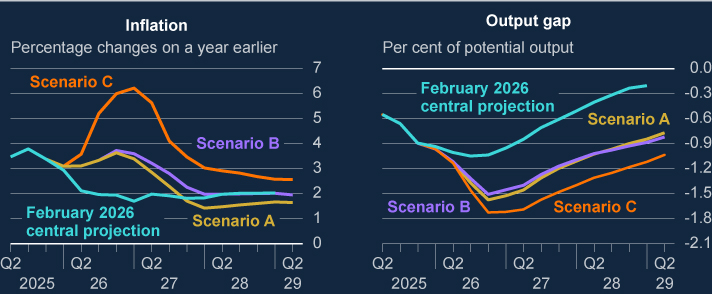

In terms of headline inflation, the largest increase was 0.6% in the year to June 2026, falling to an increase of 0.4% in December 2026 and then lower than expected inflation come mid-2027.

The expected level of the RBA’s preferred inflation metric, the trimmed mean, was also revised higher, but only by 0.3%.

Overall, a pretty tame set of conditions considering the crisis currently knocking at the door of the global economy.

But arguably the real key to the future path of monetary policy hinted at in the forecasts is the expected unemployment rate.

Unemployment is now tipped to be lower in the June quarter of this year compared with previous estimates and remain the same as prior forecasts until June 2027.

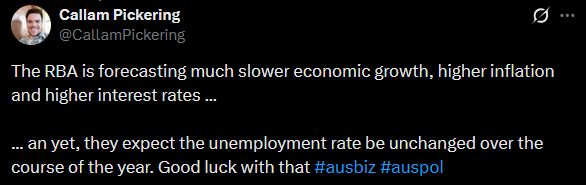

As one might imagine this is a bit of a strange set of circumstances, a significant uptick in inflation expected, along with a downgrade in growth, only for unemployment to remain the same.

This led Callam Pickering, a Senior Economist at Indeed to conclude on social media platform X:

Given that there is quite literally zero expected deterioration to the pathway for the labour market stemming from the ongoing crisis in the Middle East until at least the second half of 2027 and then only by the most marginal degree, it’s not going to take much to blow past the RBA’s forecasts and for unemployment to rise uncomfortably above their expectations.

It’s not hard to imagine a scenario in which unemployment rises to 5% or more due to the impact of a protracted crisis in the Middle East and the hangover from the closure of the Strait of Hormuz to most maritime trade.

If that were to come to pass, the RBA would be compelled by the labour market element of their mandate to cut interest rates.

From that perspective, this forecast leaves the RBA primed to cut rates if the labour market begins to deteriorate dramatically faster than anticipated.

On the other hand, if inflation ends up going far higher than anticipated, as the Bank of England’s downside scenario suggests, then it will also be compelled to keep monetary policy tight in order to tame inflation.

While Governor Bullock has so far shown a bias toward the strong labour market element of the RBA’s mandate, she could soon be in a highly challenging position of having to choose between taming inflation and preventing a potential episode of stagflation, and significantly higher unemployment on the path ahead.