Since late last year, the U.S. labour market has been experiencing a strange set of circumstances: rolling annual job growth has slowed to levels consistent with the immediate aftermath of a recession, yet the unemployment rate has remained relatively stable for almost 2 years, hovering around 4.3%.

In the last 12 months of data, the U.S. economy has created just 251,000 new jobs, but because of the fact that net migration is very low or, by some recent estimates, potentially negative, it doesn’t need to create anything like the normal level of job growth for unemployment to remain relatively stable.

If the current crisis in the Middle East turns into a full-blown global recession, then the U.S. is better placed than average for its labour market to endure it, on paper.

On the other hand, Australia is the polar opposite.

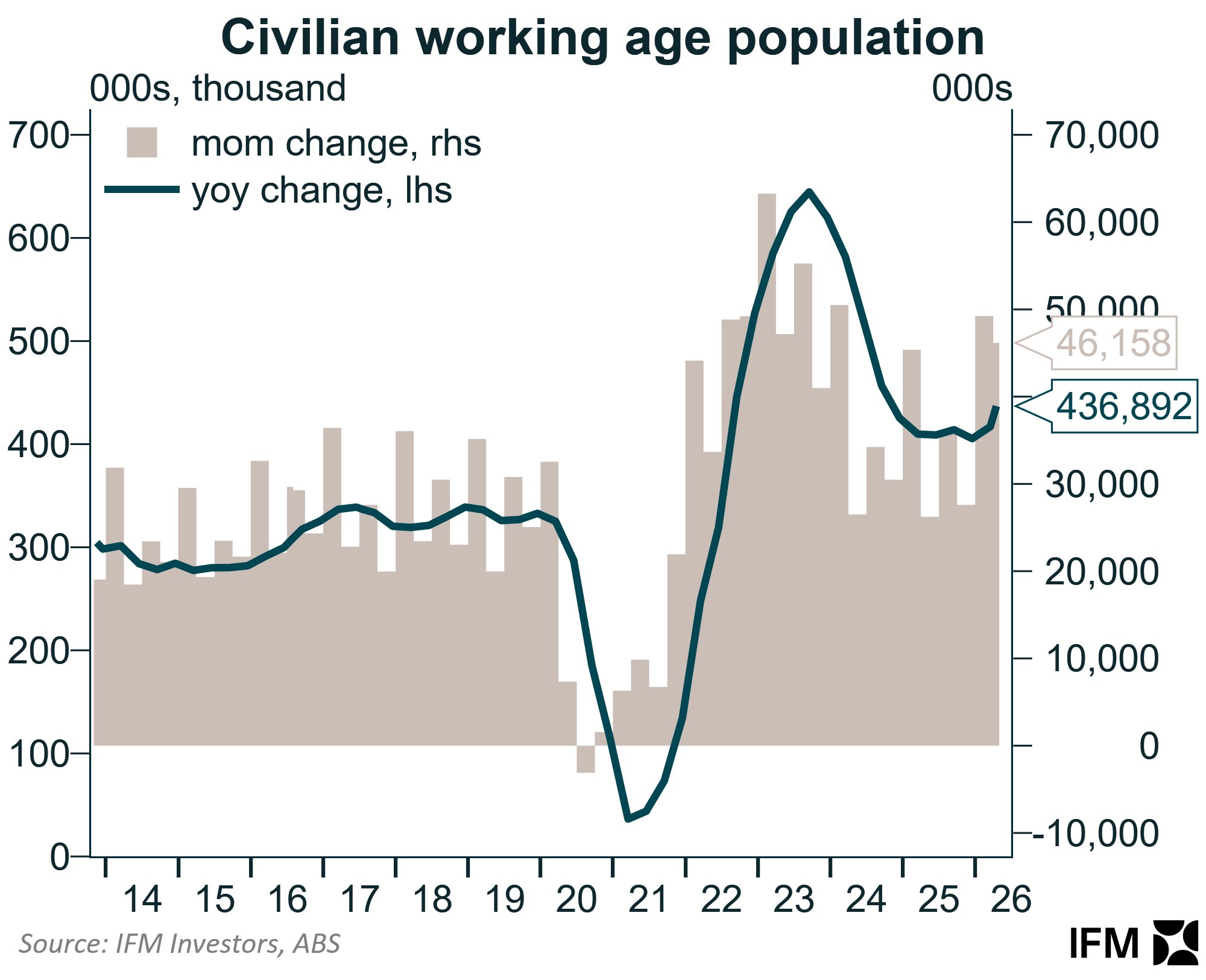

Australia’s working-age population is currently growing at a rate of 436,900 per year, the fastest rate of growth since October 2024.

Chart: Alex Joiner (IFM Investors)

Yet despite running an extremely high rate of working-age population growth, the economy created just 128,900 new jobs in the last 12 months of data.

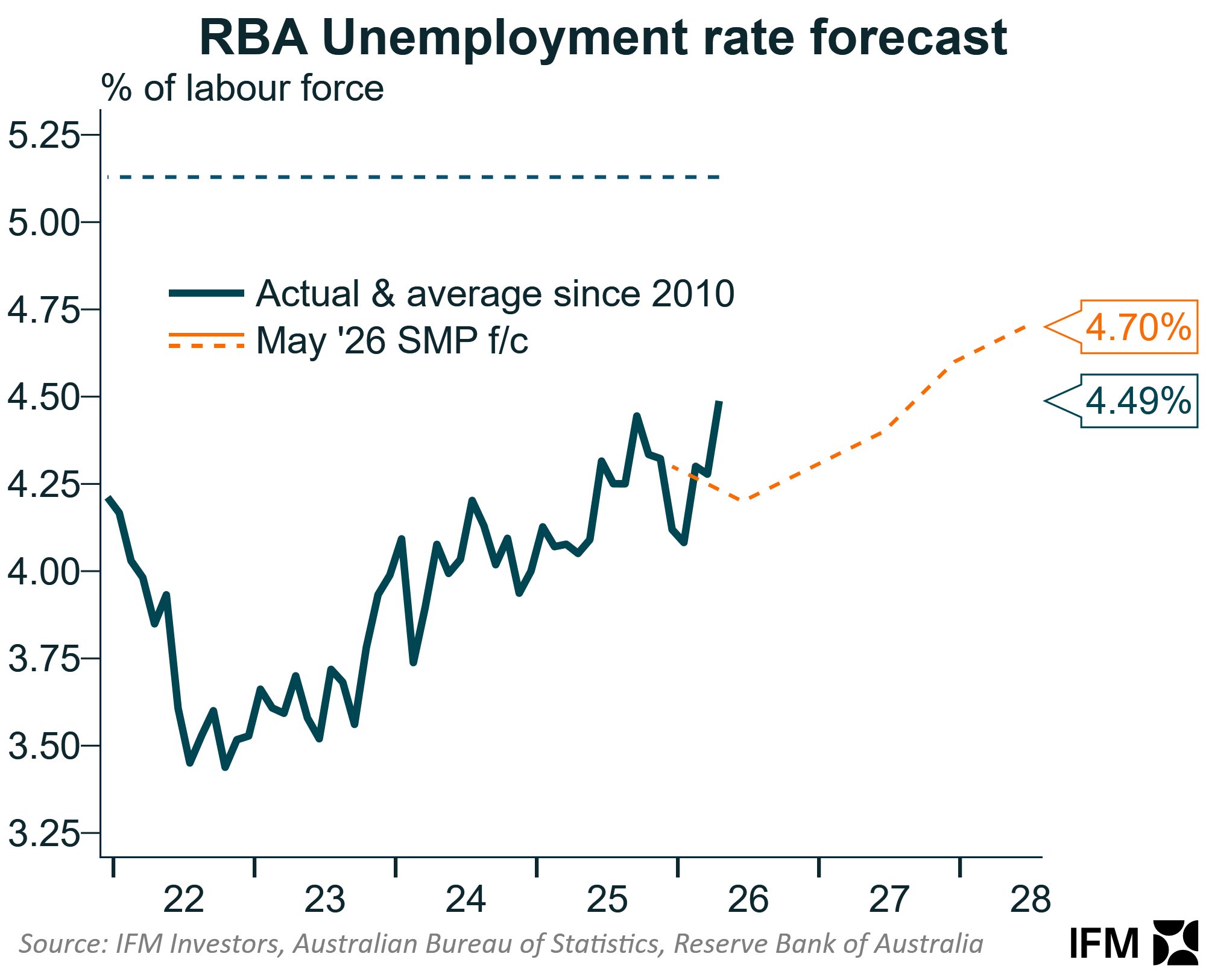

When you look at the nation’s unemployment rate, it shows.

Since this time last year, Australia’s unemployment rate has risen from 4.1% to 4.5%.

Chart: Alex Joiner (IFM Investors)

The rise in the unemployment rate has also been softened by the fall in the labour force participation rate dropping from 67.1% to 66.7%.

As the war in the Middle East continues, the weight of concerns expressed by economists and the Reserve Bank over inflationary pressures and the deteriorating path of the economy continues to grow.

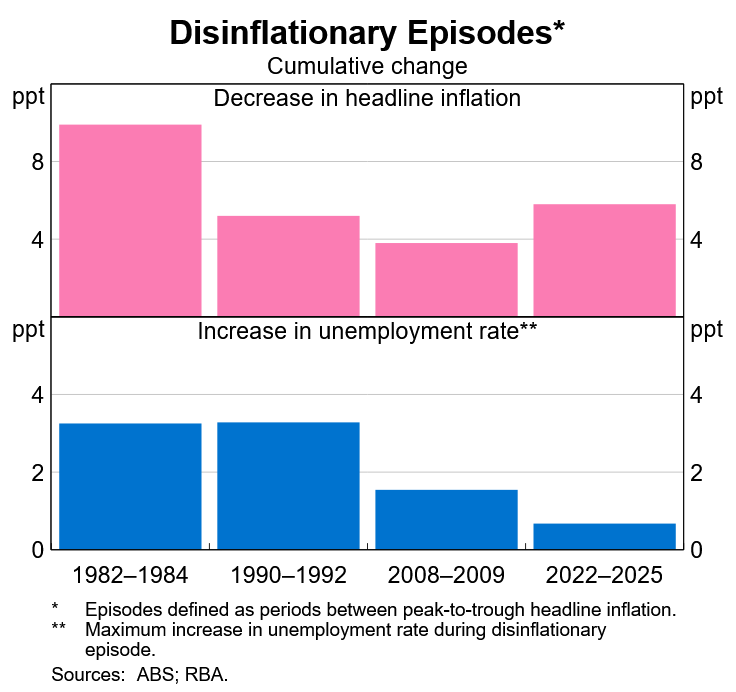

In a recent speech to the Bloomberg Forum for Investment Managers, RBA Assistant Governor Sarah Hunter shared the Reserve Bank’s concerns that a much more serious economic downturn and labour market deterioration could be required to tame inflation.

“Moreover, if (inflation) expectations rise persistently, it becomes harder for the central bank to bring inflation back to target, as it must both bring expectations back down and restore the balance between supply and demand”.

“Doing so may require a more substantial slowing of economic activity, as we saw during the early 1990s recession (Graph 6). So it’s crucial for central banks to keep inflation expectations anchored around the inflation target.” Hunter said.

This is the chart that Hunter was referring to: the decrease in headline inflation during various inflationary episodes and the associated rise in the unemployment rate during those eras.

The news from the S&P Global Australian Services PMI is also painting an increasingly concerning picture for the labour market:

“For the first time in nearly a year-and-a-half, there was a reduction in private sector employment across Australia midway through the second quarter. Although only marginal, the rate of job shedding was the joint-fastest in over five-and- a-half years (matching that seen in August 2021). The service sector joined manufacturing in retrenchment mode.”

The Takeaway

Among Anglosphere nations, Australia now has a unique vulnerability, an economy still running extremely high migration even as unemployment rises and job growth slows.

With the April labour force data painting a picture of only the very earliest impacts of the war in the Middle East feeding through, it is a warning sign of how quickly things could deteriorate from here.

Assuming a stable labour force participation rate, the economy needs to create 24,300 jobs per month based on the current rolling annual rate of working-age population growth.

Ultimately, even a stalling in job growth could see unemployment swiftly rise towards 5%, and if job growth outright reverses, significantly higher than that again.