As part of its recent first-quarter Energy Survey, the Dallas branch of the U.S. Federal Reserve produced a set of supplementary survey results compiled by asking various executives at oil and gas firms about their outlook regarding the future of the Strait of Hormuz and the war in the Middle East.

While several of the survey results were concerning outlooks, the chart prominently featured at the start of the supplementary report was the most impressive.

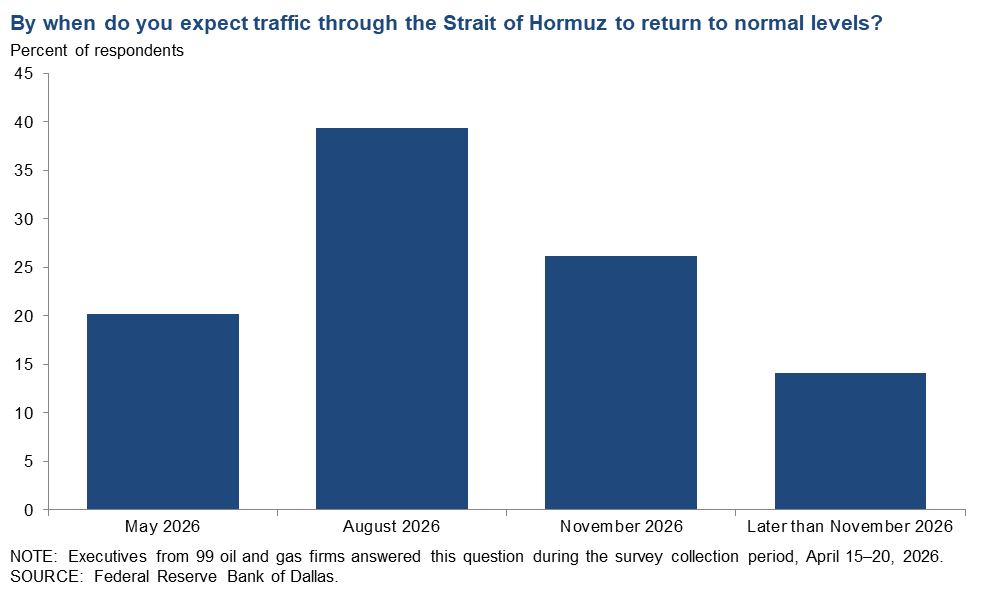

When asked, “By when do you expect traffic through the Strait of Hormuz to return to normal levels?”, 20% said by May, 39% by August, 26% by November, and 14% still later.

Put somewhat differently, 80% of surveyed executives believe that normal traffic through the Strait of Hormuz will not resume until June or later, with 40% believing it will be by November or later.

If the world enters June with traffic through the Strait of Hormuz still throttled to a relative trickle of pre-war levels, the chance of a global recession would have arguably risen past even odds.

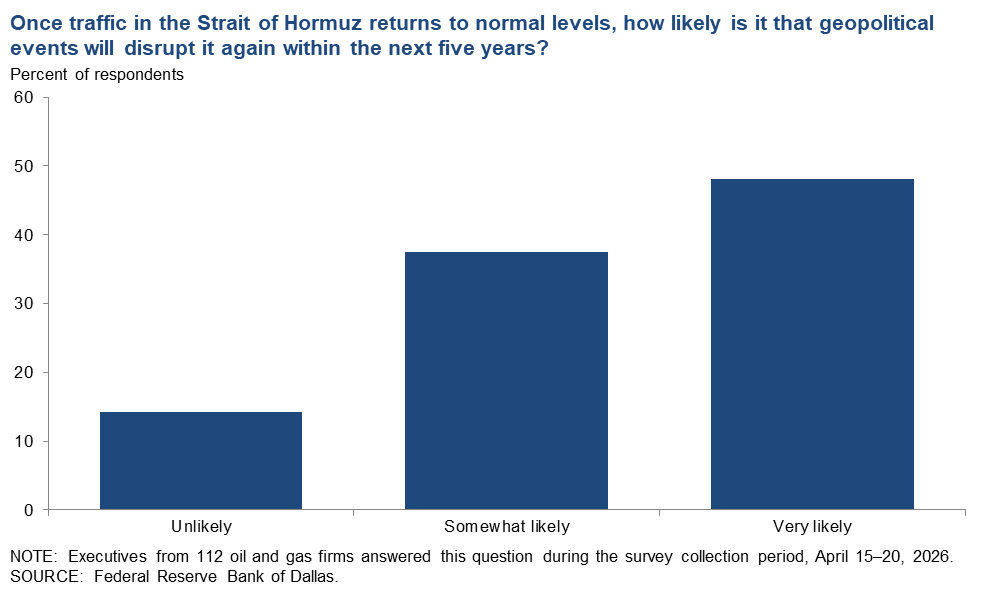

When asked about a further disruption to traffic flows through the Strait of Hormuz following normalisation, whenever that may come, they were not optimistic.

48% said that it was “very likely” that geopolitical events would disrupt traffic again in the next 5 years, 38% said it was “somewhat likely” and 14% said it was “unlikely”.

When quizzed on their view of the ability of the United States to expand its oil production to help make up the shortfall in oil supply, their forecasted production expansions came up much shorter than some of the optimistic narratives currently circulating on social media.

In terms of their outlook for 2026, 30% of surveyed executives said no change, 43% said up to 250,000 barrels per day and 17% said 250,000 to 500,000 barrels per day.

Only 10% said production that would expand by 500,000 barrels per day or more, with just 1% holding the view that production would be expanded by 1,000,000 barrels per day or more.

The Takeaway

While the battle of wills between Tehran and Washington increasingly appears like it may turn into a war of attrition, the unfortunate reality for much of the world, including Australia, is that we don’t have time for that.

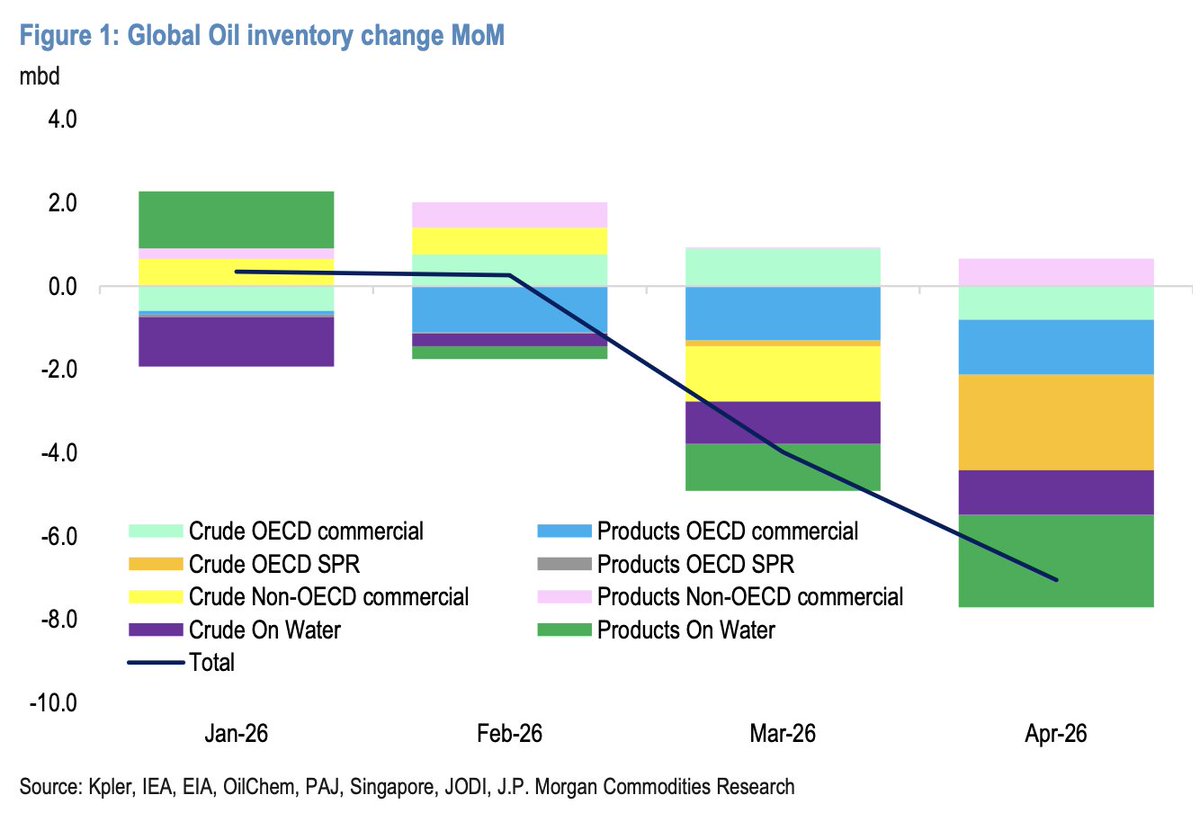

So far, most economies across the globe have been insulated by supply chain lags and have been burning through reserves, whether they be strategic reserves or refinery feedstock.

But as the chart below from JP Morgan reveals, that drawdown has swiftly accelerated in April and continues to deteriorate.

Source: JP Morgan via Ayesha Tariq on X

While some nations are much better placed than others to endure this challenging time, whether it be due to being net exporters of oil and gas, such as the United States, or due to having enormous reserves, such as Japan or China, for the nations that have neither, things are set to get a whole lot more challenging if the crisis persists as U.S. oil and gas executives believe it will.

So far demand destruction has largely been driven by a lack of supply, not by prices, with notable examples of this being a lack of liquefied petroleum gas (LPG) in India and a lack of naphtha and ethane hitting factories in Asia.

According to estimates from JP Morgan, so far the drawdown in stocks of gasoline and diesel has been kept to under 1 million barrels a day, as refiners burn through feedstock and strategic reserves. Although they note that their ability to capture the drawdown in fuel stocks is much less robust than with crude oil.

Ultimately, if the conflict continues in the long term, things are going to gradually get more and more challenging with each passing month.

So far it’s been easy mode, in relative terms.