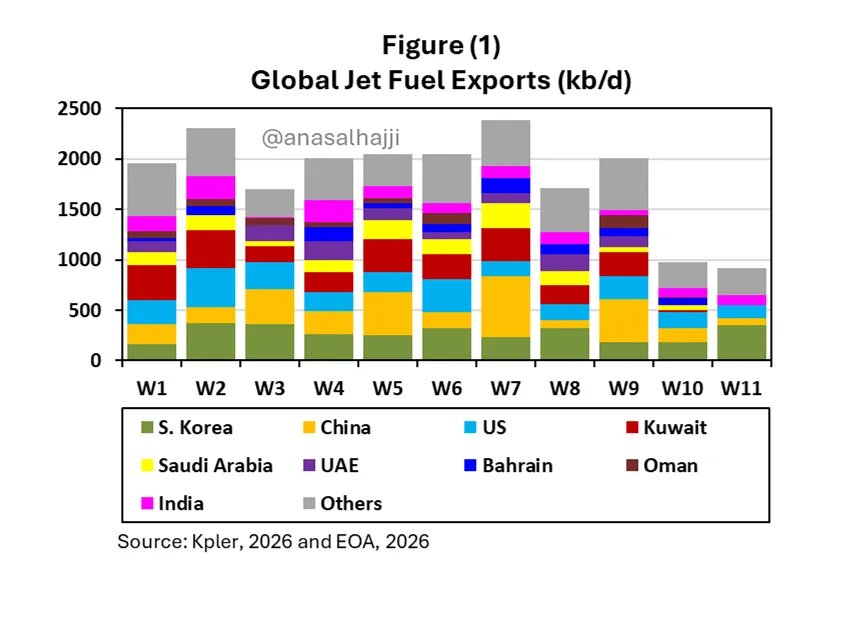

Shortly after the war in the Middle East began and traffic through the Strait of Hormuz was reduced to a relative trickle, the flow of global jet fuel exports was swiftly roughly halved, as flows from the Persian Gulf ceased and the impact of China’s near-ban on fuel exports began to bite.

Now that the conflict has been underway for nearly two months, the impact of plummeting exports is starting to show up dramatically in the total amount of jet fuel/kerosene on the water to be delivered to ports across the globe.

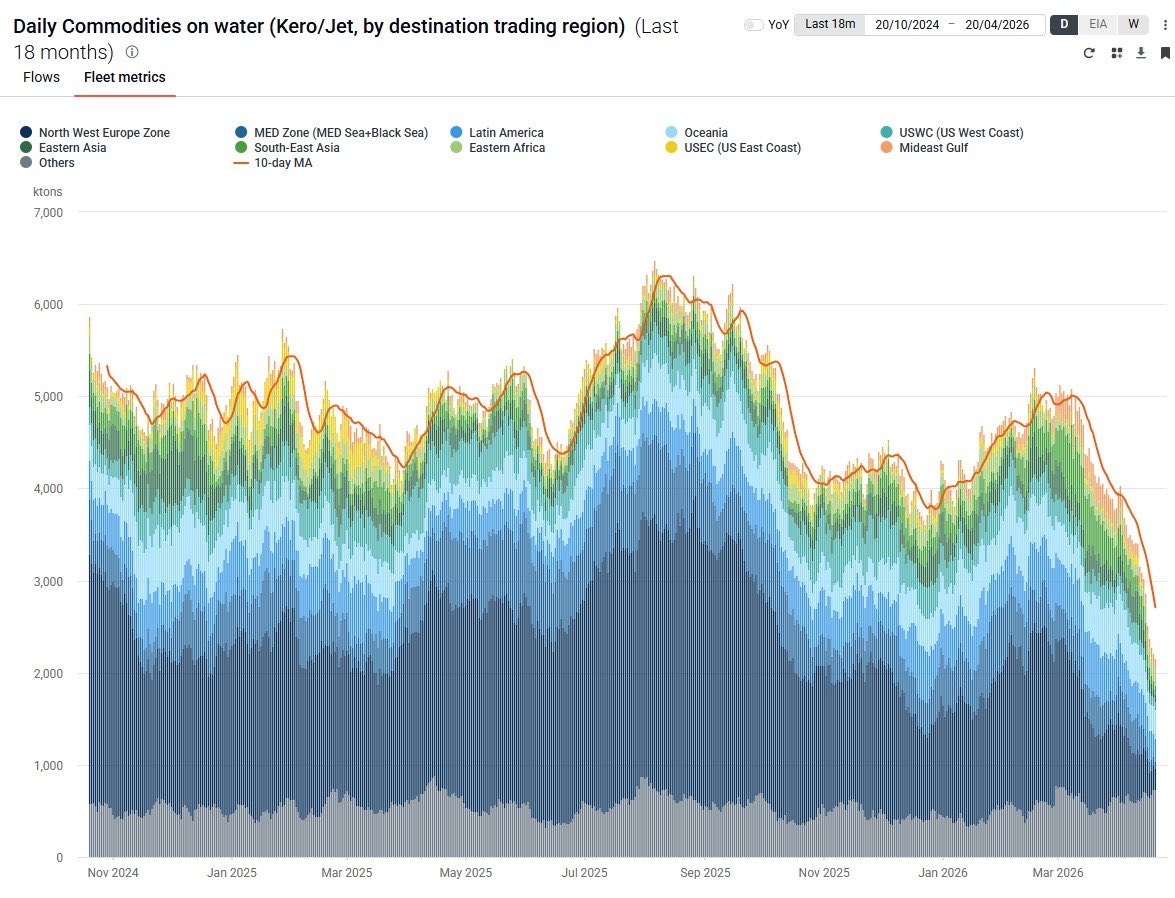

This time last year, there was an average of around 4,300 kilotons of jet fuel/kerosene heading for ports across the globe.

Today, there is roughly half that, with approximately 2,100 kilotons of these fuels on the water for delivery.

Amidst this challenging outlook, airlines in Asia in particular have been cutting flights and warning of further disruptions to come.

According to some estimates, the largest proportional impact has been felt by Air Asia (including its subsidiaries), with approximately 10% of its total flight capacity pulled due to supply issues and higher costs.

Meanwhile, International Energy Agency Executive Director Fatih Birol has warned that the impact of the crisis would gradually spread around the globe, noting that the interruption to flows of energy through the Strait of Hormuz is: “the largest energy crisis we have ever faced”.

In a recent interview with the Associated Press, he noted that Europe has “maybe six weeks or so (of) jet fuel left” and that “if we are not able to open the Strait of Hormuz … I can tell you soon we will hear the news that some of the flights from city A to city B might be canceled as a result of lack of jet fuel.”

A Complex Picture

The world’s jet fuel market is deeply challenging for nations who are importers.

Globally, somewhere between 70% and 75% of jet fuel is produced for domestic usage, leaving only 25% to 30% of fuel exportable to nations that need it.

While Asia was the hardest hit at first due to its reliance on flows through the Strait of Hormuz, the most exposed to a drop-off in global jet fuel exports are generally not in Asia.

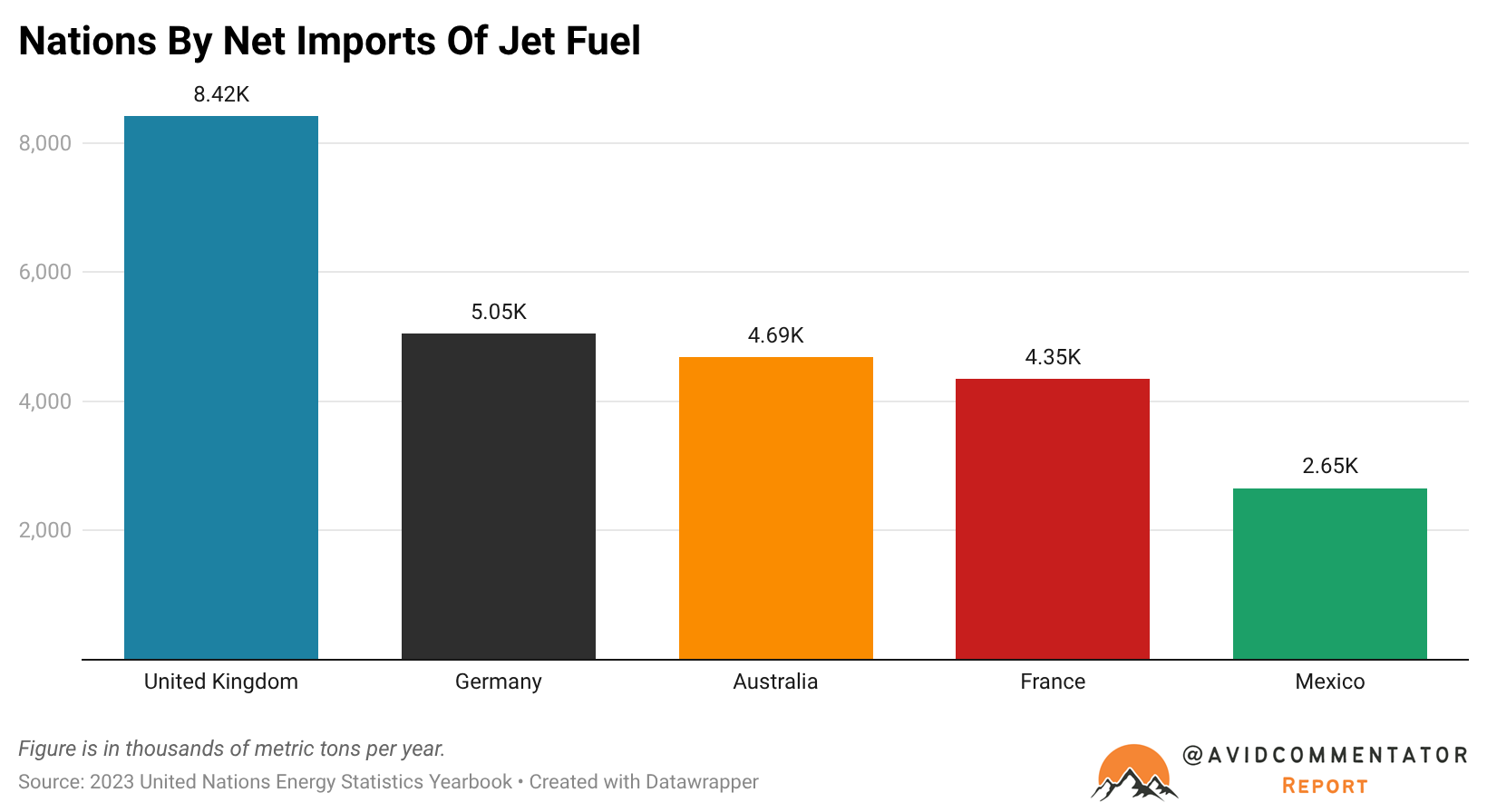

According to figures from the United Nations Energy Statistics Handbook for 2023, the five largest net importers of jet fuel are:

- United Kingdom

- Germany

- Australia

- France

- Mexico

It is these nations that, on a long-term timeline, will need to compete for a dramatically smaller slice of the aviation fuel pie, as it is set to shrink by more than half.

While nations like Australia have the financial firepower to outbid developing countries that are net importers of jet fuel, if the crisis persists in the long term, bidding wars against other wealthy large net importer nations such as Germany, France, Britain and Switzerland, amongst others, are going to be a very different story.

At that stage interruptions to flows of imports and significant reductions in flights become significantly more likely as the financial firepower of the developed world is unleashed against each other to secure cargoes to keep aerial transit and commerce running at normal levels.

As IEA Executive Director Birol noted, Europe is not yet at the crisis point, but in the coming weeks and months it will arrive there, and then the rush for jet fuel gets a whole lot more challenging.