Even the missteps of the American Madman can have a positive aspect.

China still relies less on foreign energy sources than most large nations, but it has vulnerabilities worth exposing from time to time.

This degree of dependence is far lower than that of major European industrial nations like Germany, Italy, and Spain, as well as neighbouring Asian economies like Japan, South Korea, and India.

China’s dominant domestic coal output, which continues to be the foundation of its energy system, is largely responsible for its relatively high level of energy self-sufficiency.

This is one reason why it has been hesitant to decarbonise such strategic industries as steel.

At the same time, reliance on imported fossil fuels is steadily decreasing due to rapid electrification and significant investment in renewable electricity, especially solar and wind.

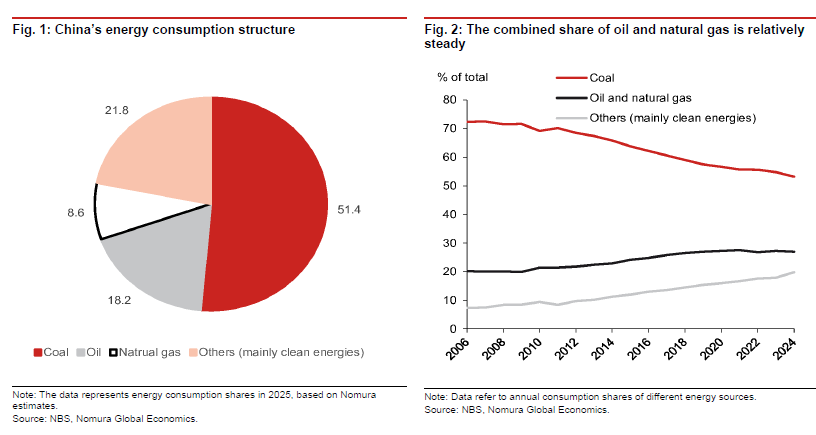

Coal still makes up a large portion of China’s energy mix; in 2024, it accounted for 53.2% of total consumption.

18.2% came from oil, 8.8% from natural gas, and 19.8% came from other energy sources like solar, wind, nuclear, and hydro.

According to preliminary data for 2025, coal’s proportion fell to 51.4%, with the growth of clean energy substantially offsetting this loss.

Still, China continues to be the world’s biggest importer of crude oil, and oil and natural gas together still make up around 27% of all energy consumption.

Because domestic oil output falls well short of consumption needs, import dependence is very high at roughly three-quarters.

Over one-third of China’s oil consumption and roughly 6–7% of its total energy demand might be impacted by disruptions in the Strait of Hormuz.

Although less, the reliance on natural gas is still big.

About 39% of consumption in 2025 came from imports, with 6.4% of gas demand associated with LNG shipments that crossed the Strait of Hormuz.

Source: Nomura

Of course, the Chinese vulnerability pales in comparison to Australia, which would run out of petrol in three weeks if there were any disruption to shipping.