DXY was pulverised.

Which held AUD up, though not against EUR.

CNY was hit.

Oil crashed as OPEC decided to pump.

The copper bubble goes “pop”. Base metals head for hard landing.

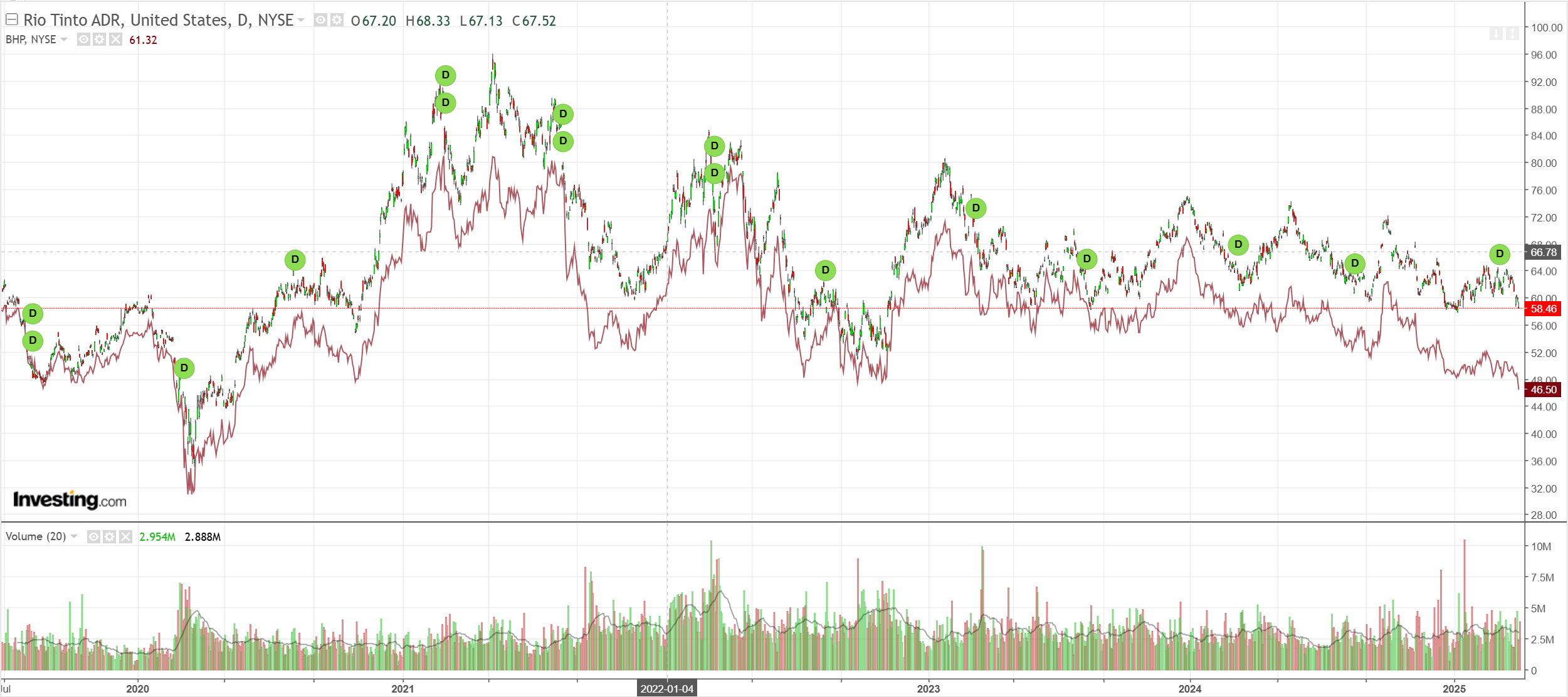

Big miners, big damage.

EM meh.

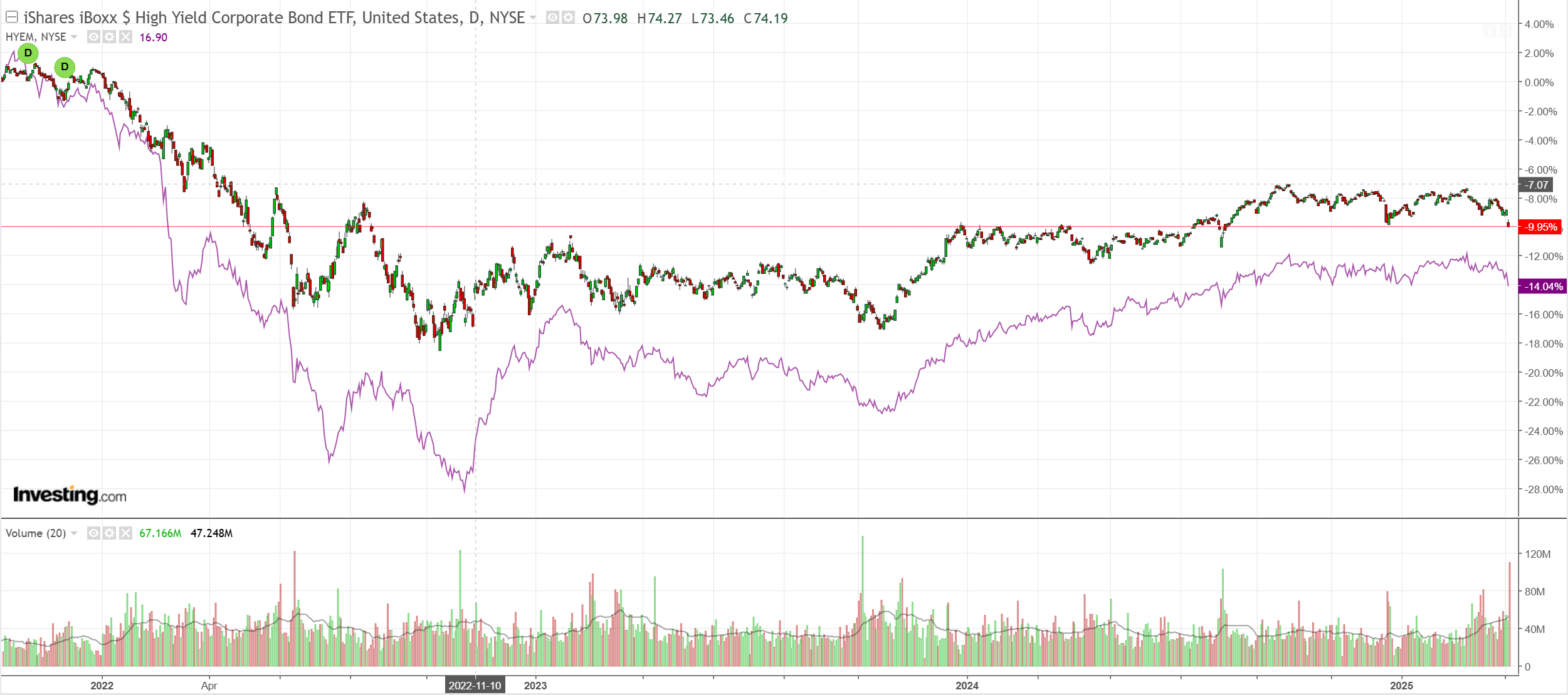

Junk breaking at last.

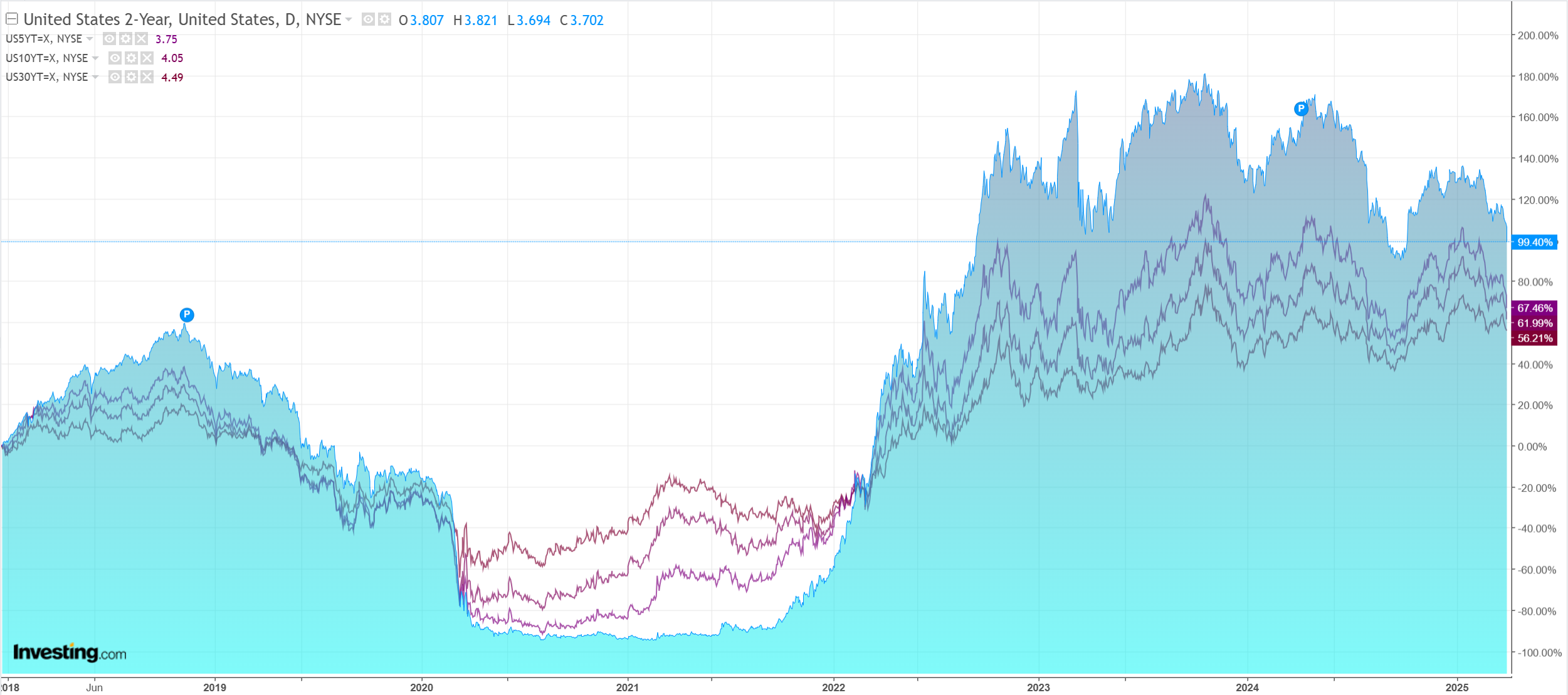

Yields are in free fall, but a long way to go to make a difference.

The S&P crashed 5% and Nasdaq 6%.

Can the AUD keep this up? Hard to think so. The market is banking on some kind of decoupling play as Chinese and European growth holds up while US collapses.

That never ends well.

Adding to market consternation is this.

Microsoft Corp. has pulled back on data center projects around the world, suggesting the company is taking a harder look at its plans to build the server farms powering artificial intelligence and the cloud.

The software company has recently halted talks for, or delayed development of, sites in Indonesia, the UK, Australia, Illinois, North Dakota and Wisconsin, according to people familiar with the situation.

Microsoft is widely seen as a leader in commercializing AI services, largely thanks to its close partnership with OpenAI. Investors closely track Microsoft’s spending plans to get a sense of long-term customer demand for cloud and AI services.

Microsoft dramatically outperformed other hyperscalers, so that’s a market signal for you. AI capex cuts ahead.

Economic data was OK but is not relevant right now. The growth shock is ahead, another reason to worry the AUD outperformance is temporary.

That said, there is this from Deutsche.

We have written about why the stability in USD/CNY, the problematic policy communication around the tariffs and the anticipation of more fiscal support measures from the rest of the world are all contributing to a weaker dollar.

But given the dramatic nature of the moves, we are becoming increasingly concerned that the dollar is at risk of a broader confidence crisis.

We have been warning about the importance of the correlation breakdown between US risk assets and the dollar for a while – European losses on US assets are now exceeding those seen during the 2022-2023 crisis.

…At the end of the day, the US has a large current account deficit, and the currency is reliant on capital inflows for stability.

A drop in the dollar, a drop in US equities and a rise in term premium in US treasuries would be the strongest market signal that a process of US disinvestment is accelerating.

A rise in term premia on US treasuries has not materialized yet, but it would be a very negative signal if it did.

That would essentially be a Liz Truss shock in the US.

Not a base case, but not crazy anymore, either.