Risk markets bounced back overnight in the absence of further good but not bad enough news following the US jobs print on Friday that saw Wall Street sink nearly 2% across the board. European markets also came back to strength but on both sides of the Atlantic it doesn’t yet look convincing as the USD remains strong going into tomorrow night’s CPI print. The Australian dollar remains in a very weak position as it can’t get back above the 67 cent level.

10 year Treasury yields barely moved with a slight adjustment lower to the 3.7% level while oil prices also were relatively stable but still extremely weak as Brent crude remained below the $72USD per barrel level at a new monthly low. Gold fought back against expectations and was able to finish overnight above the $2500USD per ounce zone.

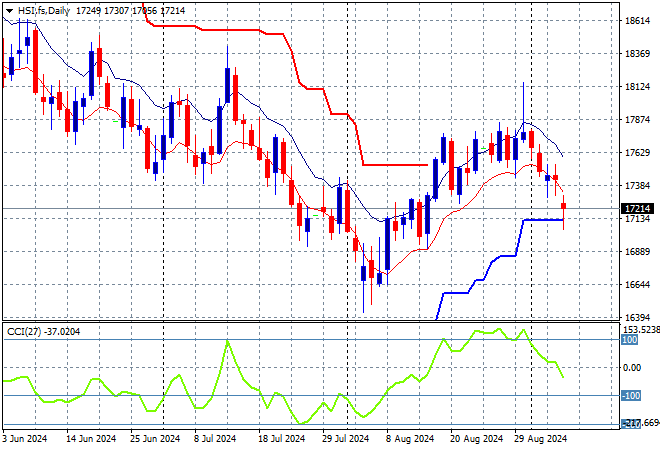

Looking at markets from yesterday’s session in Asia, where mainland Chinese share markets were again pulling back sharply with the Shanghai Composite down 1.3% while the Hang Seng Index was off nearly 1.4% to 17196 points.

The Hang Seng Index daily chart was starting to look more optimistic a few months back but price action has slid down from the 19000 point level and continues to deflate in a series of steps as the Chinese economy slows. A few false breakouts have all reversed course and another downside move is again looming here as price action just can’t clear short term resistance:

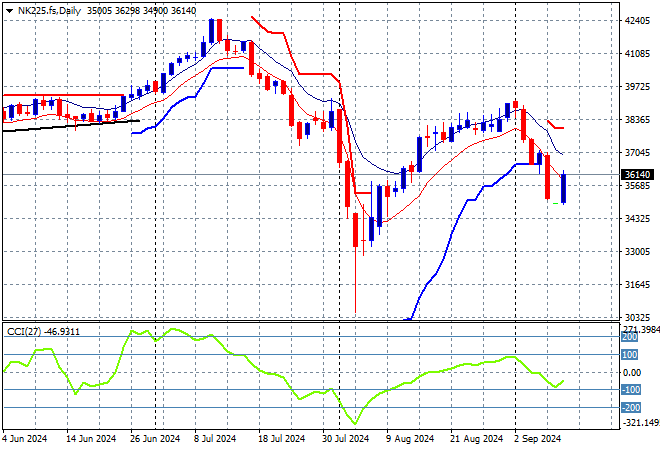

Japanese stock markets meanwhile are still falling as Yen appreciates with the Nikkei 225 closing nearly 0.5% lower to 36215 points.

Price action had been indicating a rounding top on the daily chart with daily momentum retracing away from overbought readings with the breakout last month above the 40000 point level almost in full remission. Yen volatility is coming back so a sustained return above the 38000 point level from May/June just doesn’t seem possible. Futures indicate a bounceback however this may not be enough to build positive momentum for the week:

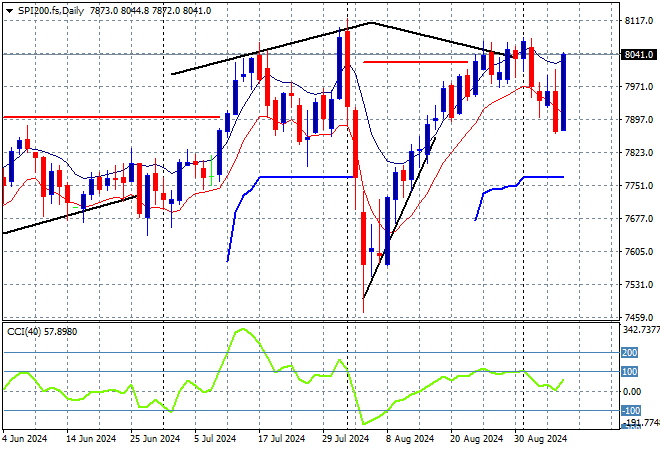

Australian stocks were down sharply at the open but the ASX200 only closed 0.4% lower to retreat slightly below the 8000 point level at 7981 points.

SPI futures however are up more than 1% due to the rebound on Wall Street overnight. Short term momentum and the daily chart pattern was potentially signalling a top here and this combination could still eventuate, as support at or just below the 8000 point level remains key to filling this gap:

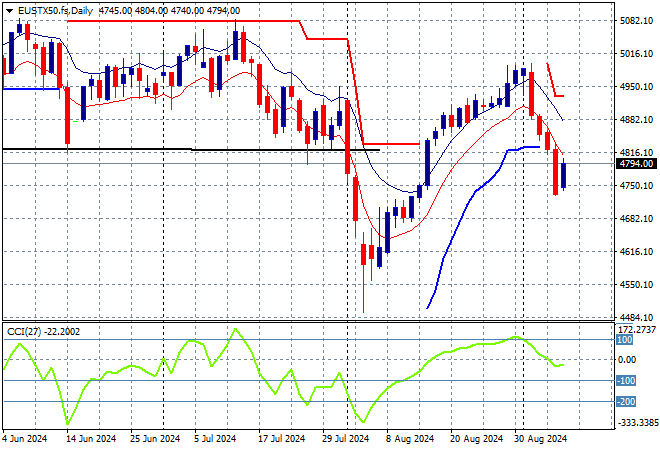

European markets got out of their negative mood with some solid gains across the continent as the Eurostoxx 50 Index closed 0.8% higher to 4778 points.

The daily chart shows price action off trend after breaching the early December 4600 point highs with daily momentum retracing well into an oversold phase. This was looking to turn into a larger breakout with support at the 4900 point level quite firm with resistance just unable to breach the 5000 point barrier. Price had previously cleared the 4700 local resistance level as it seeks to return to the previous highs but momentum has gone into full reverse turning this pullback into a selloff:

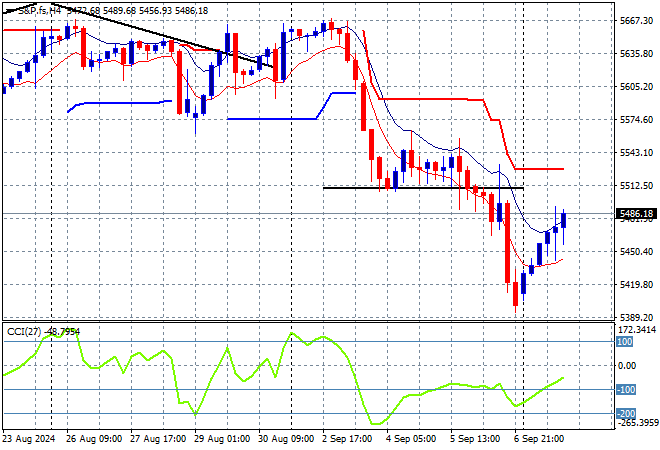

Wall Street rebounded, taking back about half the losses from Friday night with the NASDAQ and S&P500 both up exactly 1.1% each, the latter closing at 5471 points.

The four hourly chart illustrates how the inability to clear the 5600 point level in mid August and even match the July highs is setting up for a significant retracement that could end up at the 5100 point level as the Fed punchbowl is taken away. In the short term, momentum was not extremely oversold so it could bounceback further here to the 5500 point level before tomorrow’s CPI print:

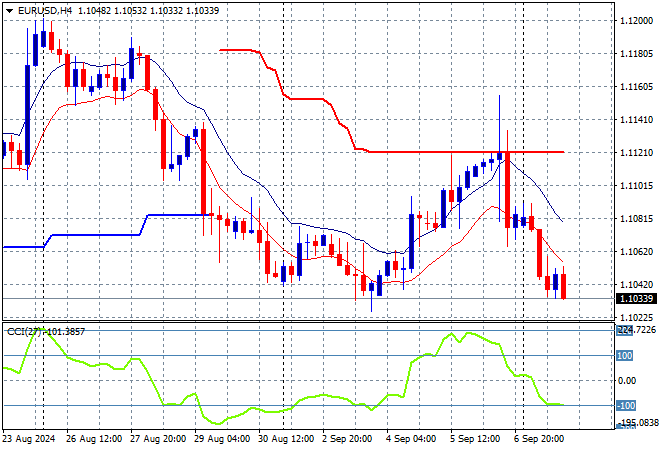

Currency markets have officially absorbed the soft NFP print and are now positioning for Wednesday’s US CPI print instead with King Dollar firming against all the majors and confirming the late interpretation from Friday night. Euro is back to the previous week lows while other currencies lost ground as well.

The union currency had been structurally supportive despite the start of week extended dip that reversed on built in expectations of this soft jobs print, with those expectations dashed and then some on the night! Watch now for a potential follow through below the 1.10 handle as momentum remains quite oversold in the short term:

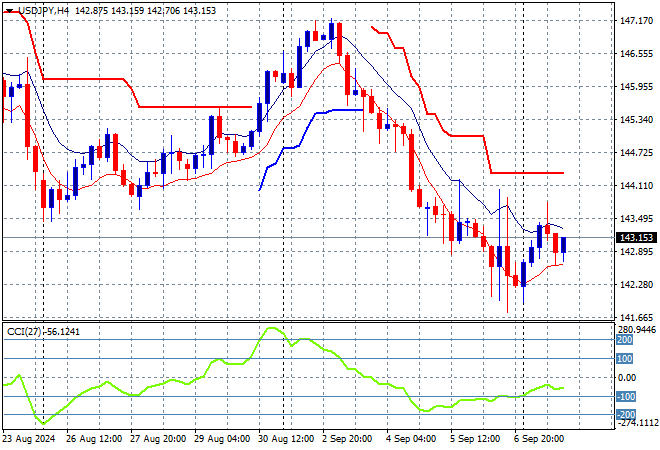

The USDJPY was able to stabilise somewhat following its on Friday night with some intrasession volatility and a return to just above the 143 level as Yen weakened ever so slightly.

The overall volatility leading up to the recent rout spoke volumes as it pushed aside the 158 level as longer term resistance in the weeks leading up to the BOJ rate hike. Momentum was suggesting a possible bottom was brewing as the BOJ wants to get this under control with this breakout building, but this retracement is coming faster than expected:

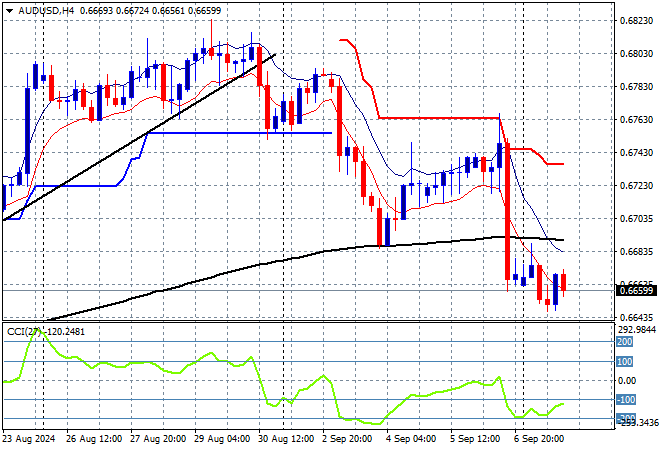

The Australian dollar fell out of bed after Friday’s NFP print, making a new monthly low in the process but was unable to climb out of its very weak position to remain below the 67 handle.

During June the Pacific Peso hadn’t been able to take advantage of any USD weakness with momentum barely in the positive zone but that has changed in recent weeks with price action finally getting out of the mid 66 cent level that acted as a point of control. This positivity has disappeared with a full retracement of the last two weeks of weak price action, staying well below the 67 cent level with the potential to fall further:

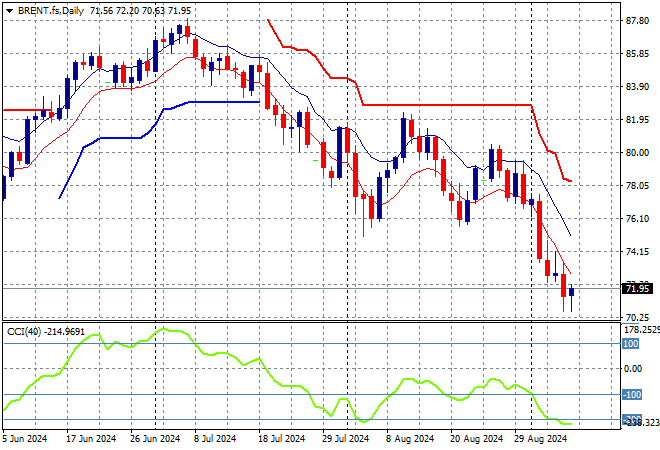

Oil markets remain in sell mode and in a very weak position on all time scales with Brent crude staying below the $72USD per barrel level after the weekend gap.

After breaking out above the $83 level last month, price action had stalled above the $90 level awaiting new breakouts as daily momentum waned and then retraced back to neutral settings. Daily ATR support had been broken with short term momentum still in negative territory, setting up for this sharp retracement – watch out below:

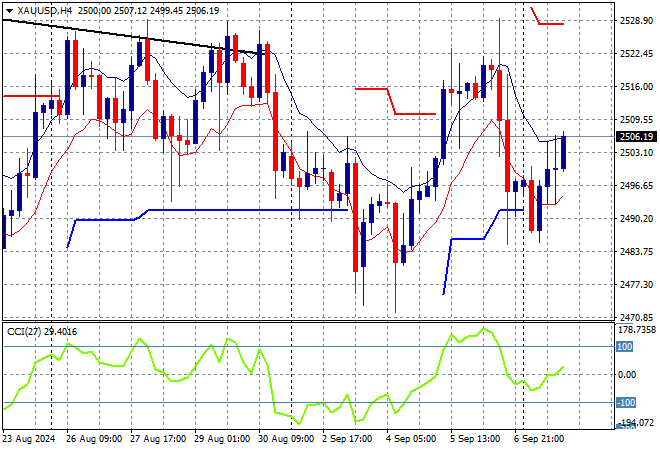

Gold was finally able to get back above the $2500USD per ounce level after the weekend gap with an unsteady session first in Asia before rebounding with other risk assets overnight.

The longer term support at the $2300 level remains firm while short term resistance at the $2470 level was the target to get through last week and is likely to be the anchor point for this week’s price action as momentum remains neutral at best:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out/wrong on your position, so cry uncle and get out!